By John Helmer, Moscow

According to United Company Rusal, the Russian state aluminium monopoly, it is one of the most transparent multinational corporations in the world – that’s to say, in the emerging markets of the world, and across sixteen countries. A report [1] of Berlin-based Transparency International (TI), issued on October 16, has ranked Rusal sixth on several measures, with a perfect 100% score on what TI calls “organizational transparency”. The other perfect scorers were Emirates Airlines (UAE), Johnson Electric (Hong Kong), Petronas (Brazil), and Shanghai Electric Group.

As for what organizational transparency means to TI and how it scored Rusal and the others, TI says it asked these eight questions as part of a larger questionnaire:

| ORGANISATIONAL TRANSPARENCY 14. Does the company disclose the full list of its fully consolidated material subsidiaries? 15. Does the company disclose percentages owned in its fully consolidated material subsidiaries? 16.Does the company disclose countries of incorporation of its fully consolidated material subsidiaries? 17.Does the company disclose countries of operations of its fully consolidated material subsidiaries? 18.Does the company disclose the full list of its non-fully consolidated material holdings? 19.Does the company disclose percentages owned in its non-fully consolidated material holdings? 20.Does the company disclose countries of incorporation of its non-fully consolidated material holdings? 21.Does the company disclose countries of operations of its non-fully consolidated material holdings? |

The answers appear to have been compiled by TI from a quick read of company reports, articles and memoranda of association, and notices filed with local stock market regulators. Before they ticked the yes/no boxes, the TI surveyors were in no position to assess what exactly the reported disclosures meant, whether they were comprehensive, or if they were true. Missing from this survey are the debt and security questions — in the case of Rusal, Russia’s most indebted company, how much is disclosed of debts to the Russian state banks, and of what security is held over Rusal group and subsidiary company shares, over production and trading assets, and in favour of what beneficial debt holders?

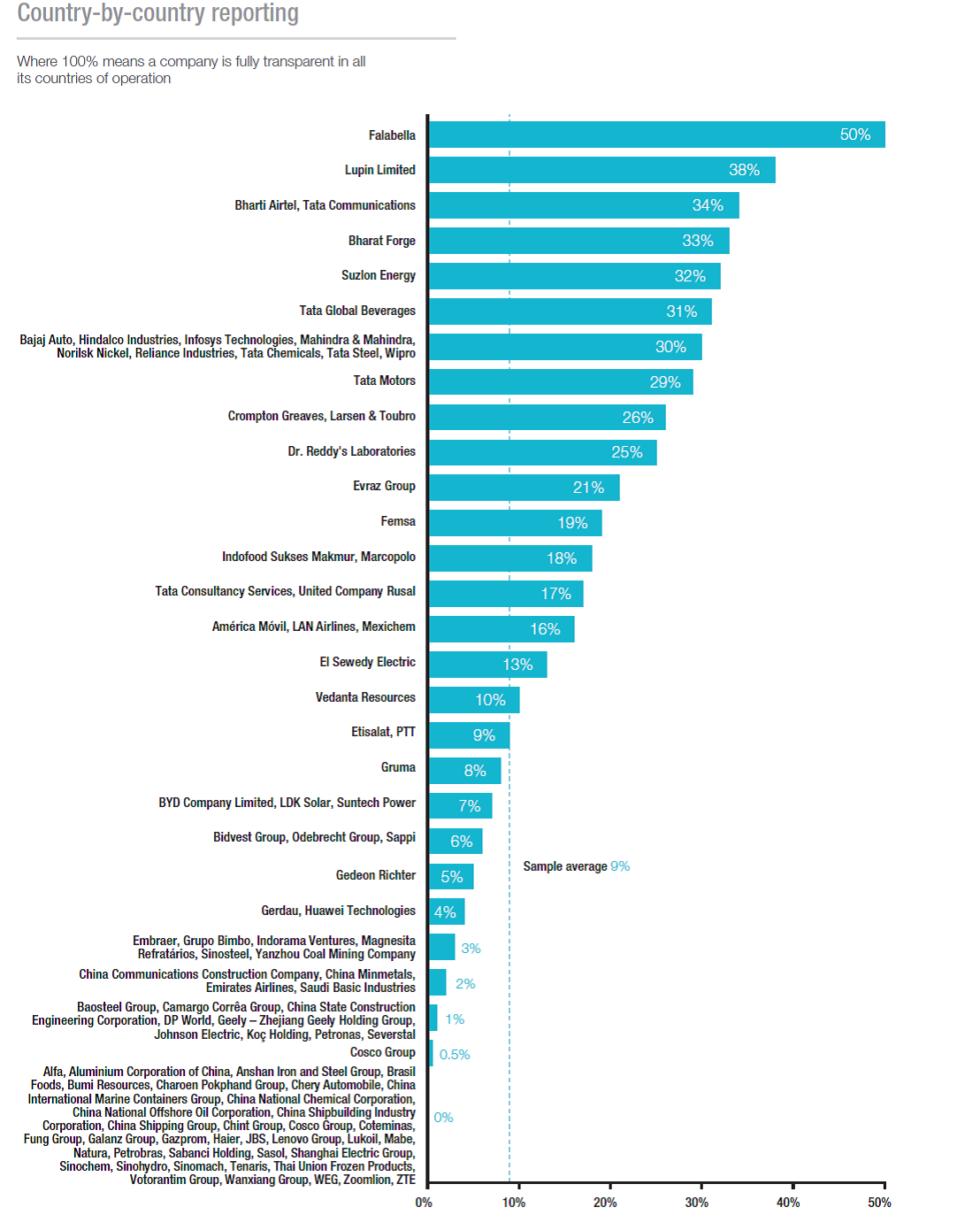

There also is a big qualification in the TI report. Rusal’s transparency varies significantly between the countries in which it operates. On TI’s country by country table of transparency, Rusal ranks 27th, trailing well behind its Russian peers, Norilsk Nickel and Evraz.

Click to enlarge

[2]

[2]

Source: Transparency International

What this means is that in one country a company like Rusal may get a perfect score on what it discloses, at least on TI’s questionnaire. But in another country – for example, where Rusal registers the ownership of its shares, or records its operating revenues and pays its taxes – the record of transparency is far more impenetrable. Quite impossible for TI to score and evaluate. That’s exactly what offshore haven registrations are for, as everybody knows. But in the latest TI report there is not a single mention of offshore incorporation as a scheme for corporate concealment.

The offshore question is obviously the case for Rusal, because it generates most of its operating revenues in Russia, but it is officially incorporated on the island of Jersey; that’s where Rusal files reports of its ownership changes, subsidiary structure, and beneficial rights and liabilities. Regarding the transparency of the Jersey records TI doesn’t know whether Rusal’s disclosures are transparent or not. Nor can TI say what the Jersey disclosures reveal about the ownership structure of the Rusal group, and who benefits from its trading operations. How Rusal conceals its offshore trading operations can be read here [3]; the role of the Latvian banks in ensuring non-transparency for these cashflows is documented here [4].

This black hole is of particular significance because of the December 6 deadline which is coming up. That’s the day from which a special class of shareholders will have the right to redeem their shares with Rusal, and demand payment of up to $1 billion in accumulated Rusal obligations. Here’s the official identification of the “redeemable” shareholders in RTI, the wholly owned Rusal subsidiary, in the Jersey record [5].

Here in Rusal’s December 2009 prospectus [6] for the Hong Kong Stock Exchange is the potential liability owed by Rusal to the redeemable shareholders. The language is quoted in full to invite close interpretation – no prize for attempting this at speed.

“RTI Limited (“RTI”), a direct subsidiary of the Company, will need to be recapitalised by 12 February 2010. The recapitalisation involves the Company giving an undertaking to pay, on a date after 6 December 2013, an amount greater or equal to the present retained losses of RTI in return for the allotment of redeemable shares in RTI. Upon allotment (provided RTI is willing to allot the Shares on the basis of the undertaking which it should do if satisfied as to its current and future solvency), the additional paid in capital from the allotment will be coedited to the share capital account of RTI and will therefore offset against the retained losses of RTI. As at 30 November 2009, RTI had retained negative equity of approximately US$1 billion. Under the recapitalisation procedure, the Company will not have to make any payment to RTI in respect of its undertaking to pay (as referred to above) until December 2013 at the earliest. In the event that RTI trades solvently through December 2013, then the receipt of monies from the Company to RTI and the payment of redemption monies by RTI to the Company are likely to cancel each other out. In light of this, no sums have been set aside in this respect. Under Jersey law, there is no requirement for recapitalisation and negative net assets do not prevent a company from continuing to trade or from paying dividends.” (See Prospectus, page 236.)

As for what can happen if the redeemable shareholders have a money claim against Rusal after December 6, the prospectus says: “The redeemable limited shares of the Company shall be capable of being redeemed from any source, but only if they are fully paid up. (iii) The redeemable limited shares are not capable of being redeemed unless all the directors of the Company who authorise the redemption make a statement as to the solvency of the Company at the time of redemption which is forward looking for a twelve month period following the redemption.” (page VII-19).

Rusal’s current market capitalization is just $4.4 billion, so on December 6 the redeemable stake in Rusal’s RTI may be worth almost one-quarter of the entire group’s value. On the current operating report [7] for the September quarter, however, Rusal says its sales revenues amounted to $2.4 billion; its cost of sales, $2.1 billion; its earnings, $130 million; its net loss for the period, $172 million; its available working capital, $1.8 billion; its accumulated loan obligations, $11.5 billion; and its cash on hand, just $463 million.

In Rusal’s latest accounting [7] for the provisions it must make for future liabilities, the total amount reported as of September 30 is $687 million; most of that is for site restoration, followed by pension liabilities, tax owing, and legal claims (page 30). There is no mention of, so no provision for, a claim by the redeemable shareholders.

A quick solvency check of these accounts suggests the Rusal board would have insuperable difficulty meeting a $1 billion redemption on condition it can “make a statement as to the solvency of the Company at the time of redemption which is forward looking for a twelve month period following the redemption.” In short, if the RTI redeemables are presented to Rusal for payment of $1 billion, that would put Rusal in bankruptcy.

So who are the owners of the 1,600 redeemable shares; and how much can, or will they claim against Rusal next month? At last attempt to analyse the meaning of the Jersey-listed “redeemables”, it was reported [8] that “RTI seems to have multi-billion claims on Rusal’s sales revenues but does no business of its own directly. So what is it there for? The answer appears to be that it is a repository of shares Rusal is holding in a form of trust for (also by) individuals who think they own a stake in Rusal revenues, and who have been counting on Deripaska to keep the value of that stake in trust, and keep it secret.”

According to Alexander Voloshin, formerly chief of staff of President Boris Yeltsin and Rusal’s nominee to be chairman of the Norilsk Nickel board, a substantial bloc of Rusal shares was owned by the Yeltsin family. Voloshin says these were sold some time ago. Another source claims it was Yeltsin himself who controlled the shares initially, and that at his death they passed to his wife and daughters. Yeltsin died on April 23, 2007. What happened next, according to a source close to Rusal, was “a rearrangement”. Either then, or by about 2010 according to Voloshin’s version, all the Yeltsin shares had been sold. Who bought them is a secret Rusal is keeping.

According to one accounting analysis, “the key issue is that the redeemable shares have been issued by RTI (Rusal’s tolling/marketing vehicle), not UC Rusal. So it is Rusal itself which is owed $1 billion by its 100% subsidiary! This was imposed by Rusal’s international banks, some of which had loans guaranteed by RTI and wanted to prevent it going into liquidation.”

The international bank agreement on rescheduling Rusal’s debts was signed on December 7, 2009. It isn’t certain whether the redeemable shares were created before or after that date. The available Jersey records suggest [9] the redeemables were paid up and recorded in the company register by July of 2007.

According to the accounting source, it is a misreading of the Jersey records and the Rusal prospectus to interpret this class of shares as anything other than an accounting device by Rusal creditors to protect their security in Rusal and its trading proceeds.

The consensus of sources closer to Rusal is different. They say the redeemable shares were created by Oleg Deripaska, the chief executive and through his EN+ holding the control shareholder of both Rusal and RTI. But there are two interpretations of what this class of shareholding is meant to do for Deripaska’s benefit.

One interpretation is that the arrangement is a poison pill, creating a liability of $1 billion for Rusal to pay in the event Deripaska triggers the RTI redeemable shareholder demand. In theory, the only reason Deripaska would do that is if his control of Rusal comes under attack from other Rusal shareholders, or from the state shareholders working through the state banks.

A second interpretation is from a Rusal insider. He believes, as do other sources close to the state banks, that the Rusal shareholding which Deripaska claims to hold through EN+ — 48.13%, according to the Rusal website [10] – has been substantially reduced by pledges Deripaska has given in exchange for the state funds keeping Rusal from insolvency since November 2008. The consequence, according to this theory, is that Deripaska acts more as the trustee of the Kremlin, less as a control shareholder in his own right. “The ultimate decision over the structure, control and recapitalization of Rusal aren’t Deripaska’s to make,” the source says. “So if there were to be a takeover decision, he might argue against it but could not prevent it. However, if he controls Rusal’s trading cashflow through RTI and the 1,600 redeemable RTI shares, he can secure his own pocket for up to a billion. It’s his exit ticket.”

Rusal’s future structure and Deripaska’s control have been in contention since mid-year after Mikhail Prokhorov’s Onexim holding, with 17.02% of Rusal’s shares, went public with a proposal to buy up a large part of Rusal’s foreign bank debt; convert this to equity; and thereby form a new majority shareholding alliance to replace Deripaska and EN+. In June Dmitry Razumov, the chief executive of Onexim, announced [11]: “we don’t want to be in a company [Rusal] whose only mission is to pay creditors, not shareholders….[The one thing that may help Rusal] to recover sooner rather than later is converting a part of its debt into equity.”

Another challenge is the litigation at the London Court of International Arbitration (LCIA) by Victor Vekselberg and Len Blavatnik to put a stop to Deripaska’s manipulation of Rusal’s shareholder charter and trading arrangements. Vekselberg and Blavatnik control 15.8% of Rusal shares. They commenced their London case in April of 2012. In the section on contingencies of the auditors’ notes for its 2012 financial report, Rusal noted [12] “the dispute relates to certain shareholder arrangements between the parties in respect of the Company. SUAL Partners alleges, inter alia, that certain contracts between the Company and Glencore International AG and a contract between the Company and a company indirectly controlled by En+ were, or will be, in breach of those shareholder arrangements. SUAL Partners seek injunctive relief preventing the Group from performing the contracts, annulment of the contracts, an account of profits from, and damages against the defendants. Management do not expect that the arbitration will have a material adverse effect on the Group’s financial position or its operation as a whole.”

The continuing lossmaking reported by Rusal this week has obliged Deripaska to lobby for Kremlin support of many kinds. One of his schemes is for the state budget to pay for a state stockpile of aluminium to hold off the market, until the market price recovers to a level where Rusal’s operations would become profitable. A similar scheme was implemented in 2009 [13] to keep Alrosa’s diamond mines in the Sakha republic working at full capacity but selling the diamonds to the Ministry of Finance’s Gokhran stock and keeping them from domestic or export sale until global diamond prices revived. The cost to the state budget at the time was more than $1 billion [14]. For the time being, such a scheme has not been agreed for aluminium.

Deripaska is also seeking permission to reorganize his Russian smelter operations, closing down the high-cost plants in the western regions, and delaying the start-up of new smelters in the east. Whether Rusal would become a purely Siberian metal producer, or return to its pre-2000 model as the producer of primary aluminium, semi-finished sheet, and downstream applications for construction, aerospace, and the auto industry, Rusal’s management isn’t saying publicly, yet. For the time being, the company’s November 12 report [15] claims the shutdown of its western plants is a temporary expedient, not a permanent restructuring of the company.

“To ensure business efficiency, RUSAL temporarily ceased aluminium production at the Volgograd, Volkhov and Urals aluminium smelters and at the first phase of the Novokuznetsk aluminium smelter as well as certain potrooms of the Bogoslovsk and Nadvoitsy aluminium smelters. Production volumes have been also reduced at other production facilities.” Aluminium industry specialists in London warn that once an aluminium smelter is fully shut down, it may be more costly to restart it than to build the same capacity elsewhere.

If the 1,600 redeemable shares are controlled, not by Deripaska but by the state, then the redemption deadline may be the start of a much bigger reorganization of Rusal than has been reported in public to date. According [16] to Rusal, its organizational structure is 100% transparent; its high score in Transparency International’s measurement “underscores the importance RUSAL places on corporate reporting and ownership structure transparency. RUSAL also scored 69 percent for its reporting on anti-corruption programmes.”

For Rusal’s minority shareholders these scores are beside the main point. Just what that is will become clearer after sunset on December 6 when, or if, Rusal and RTI’s redeemable shareholders disclose the money claims they wish to make on each other.