By John Helmer, Moscow

Russia’s government-owned fleet operator Sovcomflot, run by Sergei Frank [1], has announced that international commodity trader Glencore will take over, market and operate five of its newest oil tankers as they come out of the shipyard and put to sea.

The history of Glencore in Russia since 1991 is a simple one – only financially desperate enterprises agree to Glencore’s terms, when there is no cash to trade with, and no alternative for marketing [2]. For example, in 2008 and 2009 Glencore had baled out Oleg Deripaska’s Rusal when it was on the brink of insolvency at negative $17 billion. When Russneft’s time came in 2010, the Kremlin preferred to make its deal to save the company with the original owner, Mikhail Gutseriyev, rather than leave Russneft in Glencore’s and Deripaska’s hands. More recently, after the lifting of the grain export embargo last July, the state-owned United Grain Company has intimated that it plans to attack Glencore’s dominant market share of the Russian grain export market [3].

With these precedents, Sovcomflot announced its first deal with Glencore in November 2010. This appeared to acknowledge that Sovcomflot was having trouble taking delivery of new oil tankers and servicing the loans required to build them without money advanced from Glencore’s pocket.

The press release from Sovomflot was coy on the details. “On 16 November 2010, SCF Group took delivery of the first product tanker, SCF Alpine under a joint project between SCF Group and Glencore International AG. The project, which will be undertaken by a joint venture of Sovcomflot and Glencore, provides for the acquisition and commercial management of five coated Panamax product tankers (LR1 type). Technical management of all the vessels will be performed by Unicom (St.Petersburg) – a subsidiary of OAO Sovcomflot. The delivery of the four other product tankers is expected to be within the year 2011. Evgeny Ambrosov, Senior Executive Vice-President of OAO Sovcomflot, noted: “Sovcomflot’s entry into the LR1 product tanker segment, as well as the enlargement of the company’s fleet with modern new vessels, is in line with SCF Group’s development strategy for 2010-2015… Participation in the joint project with Glencore enables a broader access by SCF Group to the cargo base of one of the world’s largest traders and lays down the foundations of the company’s further development in the LR1 product tanker segment.” LR stands for long-range oil tanker, and LR1 for vessels with cargo-carrying capacity of between 50,000 deadweight tonnes and 80,000 dwt.

| Read for its market meaning, Ambrosov’s remark was the concession that Sovcomflot couldn’t generate enough cash for the SCF Alpine (right image) charter, or the four additional vessels still on the builder’s slips, without a takeover by Glencore. |  |

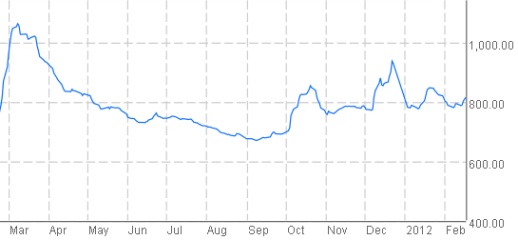

In the year since that first announcement, Sovcomflot’s bills for the additional LR1 fleet have been falling due, but the tanker charter rate today is no better than it was:

BALTIC EXCHANGE DIRTY TANKER INDEX, 2011-2012

A new announcement by Sovcomflot on February 13 reveals that it has had to extend the terms of the early deal to cover four new tankers. “On 10 February 2012, Sovcomflot (SCF Group) agreed a further joint project with Glencore International AG to own, operate and manage four coated LR1 type product tankers (74,000 tonnes DWT). The vessels “SCF Plymouth”, “SCF Pacifica” and “SCF Pearl” built in 2011 at Hyundai Mipo Dockyard Co (South Korea) will immediately be managed by the joint venture. The fourth vessel, “SCF Prudencia” will be delivered from the same shipyard at the end of February 2012. The design of all vessels incorporates all the latest requirements in terms of environmental protection, energy efficiency, crew accommodation and safety. The technical management of all the vessels will be performed by SCF Unicom Singapore – a part of SCF Group. The commercial management of the vessels will be performed by the joint chartering teams.”

“Evgeny Ambrosov, Senior Executive Vice-President of OAO Sovcomflot, noted: ‘This is the next stage of our joint ownership project with Glencore for product tankers, which started in 2010 when Sovcomflot and Glencore formed a joint venture and entered the LR1 product tanker segment with five newbuildings. The project is in line with SCF Group’s Strategy for 2011-2017, and strengthens the position of Sovcomflot in the developing markets of oil products transportation, primarily in South-East Asia and Russia.’”

In the olive oil market of the Roman empire, noone thought the donkeys which carried the amphorae to port, or the slaves which rowed them over the Mediterranean to Rome, were strengthening their positions in the profit chain. Again, Amborosov is making Glencore’s market reach look like it benefits Sovcomflot’s, when the reverse is true.

The reason that Sovcomflot would not be making its deal now unless fleet charter rates were so parlous is that there is a company record that Sovcomflot told Glencore no deal a decade ago, before Frank took over management of the shipping company.

SCF’s former CEO Dmitry Skarga told Fairplay he negotiated with Glencore on the terms of their fleet marketing offer in 2000 and 2001. Then, he said, the fleet deal was rejected by the Sovcomflot board because the board judged that “Glencore would take all the profit and leave Sovcomflot with all the costs.” According to Skarga, “the new arrangement is a sign of how desperate the management is in the current market.”

In the latest deal announcement, Richard Prince, deputy head of ST Shipping, the Glencore subsidiary for fleet operations registered in the Singapore tax haven , said his company is introducing to Sovcomflot “our experience of commercially operating tankers and our cargo base”. That “experience” is based on a fleet of 203 vessels, according to company reports as of December 31, 2010. These include 176 vessels on time charter for third-party owners, joint ventures, or for Glencore’s direct interest. But just 41 vessels in the Glencore fleet are reported by the company to involve Glencore’s equity interest, suggesting that only one in four of Glencore’s fleet partners allow the Swiss-based conglomerate to take a dividend-based stake in their tanker business. Sovcomflot thus appears to be in the minority of Glencore’s partners.

A close look at the Glencore prospectus for the initial public offering (IPO) of its shares in Hong Kong and London in May 2011 reveals that ST Shipping’s “experience” in 2009 and 2010 was loss-making. “Assuming [sic] Glencore holds a long position in freight at any given time”, reveals page 17 of the Glencore prospectus risk section, “a decrease in freight rates could have a material adverse effect on the performance of Glencore’s Energy Products business segment…The recent economic downturn led to a significant reduction in freight rates and had an adverse effect on the performance of the freight desk, which experienced significant losses in 2009 and 2010. While freight spot rates have recovered to some extent in the current year, there has yet to be a sustained improvement. There can be no assurance that freight losses will not experienced in the future…”

So what assurance can Frank and the Sovcomflot board have accepted from Glencore that it can turn the Sovcomflot fleet operations into anything but the loss-making ST Shipping has been achieving since it put the SCF Alpine to sea? Is the customary Glencore commission of 18% a transfer through the Singapore tax optimization zone into a profit it is willing to share? With Sovcomflot the state company? With someone else?

And if loss-making experience is the gun to Sovcomflot’s head right now, how far will it extend into other areas of Sovcomflot’s operations which management cannot make profitable in the current oil shipping market? Is there, for example, the intention of Frank and Ivan Glasenberg, Glencore’s chief executive, to extend Glencore’s “experience” into the lucrative marine oil-search segment of the market occupied by state-owned Russian company, Sevmorneftegeofizika (SMNG)?

| SMNG operates a fleet of sophisticated vessels equipped to search the seabed for traces of oil and gas. To the right, the Vyacheslav Tikhonov (above), and the Akademik Lazarev (below). |   |

Late last week, a press report appeared in Interfax and in other Russian media claiming that “Prime Minister Vladimir Putin has endorsed the transfer of 100% of shares in OJSC Sevmorneftegeofizika (SMNG), Russia’s largest marine geophysics company, to the charter capital of Sovcomflot”. Although both companies were reported to have agreed to the capital transfer and takeover by Sovcomflot, there was no announcement on either company website. No trace of a government resolution, decree or order can be found. Putin’s spokesman, Dmitry Peskov, failed to reply to the question of when, where or how Putin had done what the news leaks claim.

When SMNG was asked to confirm the agreement to the Sovcomflot takeover, and to estimate what SMNG estimates its enterprise value to be at present, the chief executive, Konstanin Dolgunov, and his deputy, Boris Sapozhnikov, did not respond. In Murmansk, where SMNG is headquartered, the regional branch of the state property agency responsible for supervising SMNG was asked to confirm that it is implementing the prime ministerial order. Along with the parent ministry, the Ministry of Economic Development in Moscow, they were asked to clarify the legality of the de facto privatization of SMNG without a public auction or competitive process. No reply.

In short, noone directly affected by the proposed takeover is willing to acknowledge that the government decision to implement it has actually been made. According to one investment bank source in Moscow on Friday: “I’m aware of the news. I’ve just seen it in the papers. But it’s not the final word.”

SMNG was first established as a state enterprise in 1979. In 2003 it was reorganized as a joint stock company in which the state holds 100% of the shares. In addition to its Murmansk operational base, SMNG also operates from Gelendzhik, on the Black Sea. This is how [4] the company describes itself. No financial reports have been released on the company’s website, and so for the time being, it is impossible to tell what its revenues look like, its costs, and its bottom-line. Estimating its capital value if incorporated within Sovcomflot is also impossible.

Maritime industry analysts in Moscow, who follow Sovcomflot and other listed Russian fleet companies like Fesco and Prisco believe there is no precedent for adding value to a shipping company by combining it with an oilfield services company. “There is nothing like that I’ve seen,” said one Moscow transportation analyst. “Oilfield services make a different enterprise group. Compared to the tanker and fleet operator group they have different drivers. They are different businesses. [Adding SMNG to Sovcomflot] would not necessarily add value to Sovcomflot’s share sale.” The Fitch ratings agency has already reported [5] that Frank’s wager on adding new vessels to his fleet when charter rates were plummeting was a mistake. The reaction to the SMNG announcement suggests he is making another one.

Frank appears to have convinced the Sovcomflot board, and some, but not all government ministers, that the merger will add capital value to his IPO by simple arithmetic — his valuation of Sovcomflot plus his valuation of SMNG’s capital. Sovcomflot has been issuing asset valuations of around $6 billion since 2008, and these have continued to rise as Sovcomflot’s financial performance has been faltering. The last asset value figure published was $6.7 billion as of September 30, 2011.

The press leaks appear to have been orchestrated by Frank to amplify on a letter he wrote Putin recommending the takeover of SMNG a month ago. One of the press reports cites Frank’s letter as saying that adding SMNG to Sovcomflot this year would enable the establishment on “the base of Sevmorneftegeofizika of a world-class Russian marine seismic company with a specialization in working in Arctic conditions.” Frank even told Putin that Sovcomflot would invest $300 million in SMNG “by placing orders for the construction of new vessels at Russian shipyards without the involvement of the budget.” According to the reported Frank letter, this newbuilding programme would be arranged with state-owned United Shipbuilding Corporation.

The contents of the letter to Putin leaked to date do not mention how Sovcomflot can afford new investment in fresh vessel construction when it cannot afford to service the loans on the so-called Glencore fleet.

This press report [6] claims Frank assured the prime minister that the federal Ministry of Transport is backing the combination, along with SMNG itself, but the Ministry of Energy is opposed. Again according to this press report, Putin scribbled the word “agree” on the letter, and ordered staff work to prepare “projects of necessary enforcement documents” for the proposal. The interpretation of Putin’s cryptic is so far Frank’s.

| The one publicly listed company comparable in function, business and specialization to SMNG, whose shares trade in a regulated international market, is Polarcus of Norway. It operates a fleet of 8 specialized vessels (right image) to SMNG’s seven. |  |

Howver, Polarcus’s capital value has been shrinking dramatically since 2008, as the chart of its share price shows. At 4.37 Norwegian krone, Polarcus is today worth one-third of its value at the start of 2008:

Currrent market capitalization for Polarcus is NOK2.04 billion; that’s equivalent to US $350 million. Polarcus’s financial reports show that it has been loss-making every quarter since 2010. The list [7] of stock-listed comparable geophysical services companies worldwide is a long one; None is larger than Polarcus, and almost all are showing a downward trend in share price and capital value. If market valuation methods are to be applied to SMNG, Sovcomflot is acquiring an asset with a negative rate of return.

The consensus of Russian analysts is that the proposed takeover is a bad idea. According to Nord News, “although this [deal] will reduce the volatility of the shipping giant’s income, it will increase its expenditures in connection with the need for the development of the new company [SMNG] in the industry.” IFK Metropol reports that “diversification of the company’s business is not very suitable, since there is no synergistic effect.”

A London marine market analyst warns that acquiring SMNG would not diversify Sovcomflot’s sources of revenue, because the cashflow sustaining SMNG’s operations comes from the same oil and gas companies which produce the cargoes Sovcomflot’s tankers currently transport. “So either the main purpose [of the proposed deal] is to save Sevmorneftegeofizika by renewing its fleet at a cost SMNG can’t afford by itself. But then Sovcomflot can’t afford this either. Or else there are hidden values in SMNG, like its oil data archives, which will pass into private hands after Sovcomflot’s privatization.”

Frank has ordered Sovcomflot not to respond to this correspondent’s questions.