By John Helmer, Moscow

A spate of advertisements for an initial public offering (IPO) of shares, accompanying several rouble bond issues, makes the Lenta hypermarket chain of St. Petersburg appear to be diversifying its investor base with promises of strong growth and a wager on rising Russian consumer spending. In fact, Lenta’s largest shareholder, the US investment fund TPG, is quietly attempting to sell out of the company with the pitch that if a new stakeholder doesn’t hurry with his cash to the negotiating table, the price will be much higher later on.

The ploy, already recognized by investment banking sources in London and Moscow, is a new twist on Russian corporate attempts at placing shares on the London Stock Exchange (LSE). It has the advantages of concealing the company’s financials before they are expected to worsen; and of avoiding the accountability and governance rules demanded by the UK Listing Authority. There’s one catch, though – Lenta and TPG wouldn’t be playing this game unless they have something to hide, and no genuine buyer for their shares.

Lenta is a grocery retailer, which started in St. Petersburg in 1993, when the owner was Oleg Zherebtsov. Nowadays, the chain says it operates a total of 59 stores located in 34 cities, including 16 in St. Petersburg, 4 in Novosibirsk, 3 in Omsk, and 2 in four other cities. St. Petersburg is also the hub for inventory stocking and despatch to the stores all over the country – except for Moscow, where much bigger, better capitalized rivals – Magnit, X5, Dixy, and O’Key – dominate the retail market.

But according to Lenta, it has now decided to penetrate the Moscow market with eight stores so far in planning. Lenta’s website claims its annual sales revenues in 2012 came to Rb109.9 billion ($3.3 billion); if the figures are accurate, that represents an annual growth rate since 2008 of 23.3%.

Zherebtsov sold out in 2009 after a dispute which embroiled his US partner, the company’s chief executive and board chairman, along with executives at the Moscow office of US investment fund TPG. Zherebtsov had been trying to cash out for several years before, but negotiations with international retail chains like Carrefour had failed. Promises of an IPO on the London Stock Exchange were issued publicly, then aborted. A private placement was arranged instead with the European Bank for Reconstruction and Development (EBRD).

The current shareholding position is that TPG holds 58.3% of the voting shares; and the state bank VTB holds 14.1%; VTB is Lenta’s controlling creditor with asset pledges securing its Rb24.5 billion ($742.4 million) loan. The EBRD stake is 21.6%. The 6% remainder has not been identified.

The fact of shareholder conflict at Lenta over five years is very well-known, not least because it turned into gangland violence in 2011, in the Bloomberg version [1] of the story.

But what exactly Zherebtsov and the others were fighting about has not been disclosed by the company, nor reported in the Russian media. If personnel and policy are stable today, Lenta refuses to say what policy consensus the company management, TPG and VTB have reached. TPG refuses to say what its intentions are for the company. With a history of what the Russian media have been calling a scandal, this silence is deafening. Read this account [2] of the trouble in 2007; and this one [3] a year later.

Applying the cash-and-carry formula to himself, Zherebtsov (3rd from left) has turned to yacht racing [4] since he abandoned ship at Lenta.

Applying the cash-and-carry formula to himself, Zherebtsov (3rd from left) has turned to yacht racing [4] since he abandoned ship at Lenta.

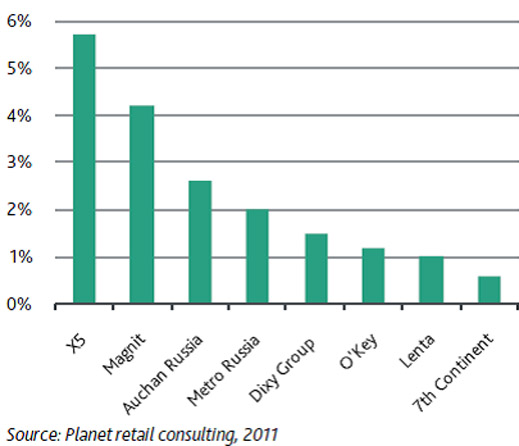

The chart illustrates market shares for the biggest Russian retailers as of 2011, with Lenta trailing at just 1%:

SUPER-8: RUSSIAN MARKET SHARES OF THE MAJOR GROCERY CHAINS

After Zherebtsov, whoever controls Lenta appears to have decided that the only way to lift its market share, along with its market capitalization and resale value internationally, is to compete head-on with the larger Russian operators. This strategy requires adding more stores and more Moscow exposure, costing more and more debt, and postponing the risk of failure by concealing financial reports behind a screen of advertisements.

The first test of the new strategy failed when Wal-Mart and Lenta opened sale and purchase talks in 2010, but failed to agree [5].

A recent report by Moscow investment house Finam claims it was told by Lenta that revenues for 2012 came to $3.44 billion dollars, and net profit of $199 million. Lenta’s cost line – where the risks of related-party trading and cash stripping are greatest – was not disclosed. According to Finam, the debt to earnings (Ebitda) ratio was growing faster than revenues, and had reached 3.36x by the close of the March quarter this year. Said Finam: Lenta plans to open 18 hypermarkets each year, spend at least $2.49 billionover the next three years, and by 2016 will reach annual sales of $9.2 billion.

There is, however, no way of telling whether Lenta’s financial claims are accurate. That’s because it publishes data according to Russian accounting standards (RAS) which fail to account for a wide range of subsidiary transactions and offshore transfers. Here [6] is a sample.

For the company to sell its shares on an international market and to qualify for a London IPO, Lenta must disclose three years of audited financial reports, compiled according to international financial reporting standards (IFRS) and accompanied by auditor’s notes on related-party transfers, import trading and pricing schemes, tax optimization, and use of offshore units. The holding company itself is registered in the British Virgin Islands. Asked for these records, Lenta’s spokesman Yana Mogileva said that Lenta doesn’t disclose financial reports “because we are not a public company.” That’s not quite the truth.

TPG refuses to identify the executive in charge of its Lenta investment, and refers all questions to Vladimir Melnikov, a public relations agent at Grayling in Moscow. Melnikov and TPG were asked to say whether they intend to sell their stake, either in a private placement, or at an IPO. They were also asked to say why they refuse to disclose audited IFRS financial reports for Lenta. Melnikov refused to reply.

In fact, Lenta has prepared at least one set of IFRS financials. They have been provided early this year to the ratings agencies, Standard & Poors and Moody’s, in order to obtain a rating for Lenta, ahead of bond issues for a total of Rb10 billion ($323 million). But Lenta has withheld these financial data from the market in general. A half-dozen Moscow analysts specializing in the Russian retail sector say they have never seen these Lenta reports.

Standard & Poors (S&P) reported in February of this year that “Lenta’s public disclosure is limited owing to its private ownership. However, semiannual consolidated accounts under International Financial Reporting Standards (IFRS) for parent company Lenta Ltd. and quarterly stand-alone accounts under Russian generally accepted accounting principles (GAAP) for Lenta LLC somewhat mitigate this.” But S&P also concluded [7] that “our assessment of the company’s business risk profile [is] ‘weak’” and its financial risk profile [is] ‘aggressive’.” That last term reflects the rapid accumulation of debt obligations Lenta is issuing to finance expansion of its store network. If Russian business conditions deteriorate for Lenta, and it faces pressure from its creditors or suppliers, S&P claims that VTB, with its 14.1% shareholding, will guarantee refinancing.

Moody’s has issued two reports on Lenta, one on January 18, 2013, and a second on Febuary 26. Read the first [8] and the second [8] here. According to Moody’s, last year’s revenues came to $3.2 billion, but no other financial data were disclosed. The ratio of debt to earnings (Ebitda) calculated by Moody’s was 2.3xin 2012, compared to 3.5x in 2009. This ratio is evidently worsening now, but Moody’s doesn’t provide projections for Lenta’s revenues, earnings, profit, or debt. It does warn that Lenta is planning annual capital expenditure of $600 million, compared with $75 million in 2011, and just $26 million in 2010. Moody’s also warns that there is a problem in forecasting Lenta’s future because the current management has “ a limited track record of operations” and the shareholding structure lacks stability because there is “no strategic investor.” Note that the numbers Lenta provided Finam don’t match the numbers issued to Moody’s.

Moody’s intimates that it doesn’t know when TPG will sell out, but it concedes the risk to Lenta’s value in the market is considerable if TPG plans to exit soon. “Lenta has [a] limited track record of operations following the resolution of [the] shareholder dispute and resulting change of shareholders at the end of 2011. This dispute, which started in October 2009, disrupted the work of Lenta’s top management and board of directors, resulting in a slowdown in the company’s growth and operational inefficiencies. The dispute was resolved by the exit from the company of one [Zherebtsov] of the key shareholders (owned 41% of Lenta as of end-June 2011), and by TPG Capital increasing its voting stake in the company to controlling (58%). We also note uncertainty associated with Lenta’s long-term strategy and financial policies, given the company’s shareholding structure with no strategic investor and that the company’s current shareholders are financial investors that will likely aim to exit the business in three to five years.”

According to Moody’s analyst Sergei Grishunin, “a rating cannot be assigned without the analysis of financial statements made in accordance with IFRS. To assign a rating by the agency, companies provide for Moody’s their IFRS financial statements for the last three years.”

It can also be taken for granted that when Carrefour and Wal-Mart said no to a buyout of Lenta shares, they had the detailed financial records which Lenta is still withholding from the market. At the very least it can be inferred that the selling price for Lenta was much too high for the international chains to accept. Last week Lenta announced it has hired JP Morgan, Credit Suisse, UBS, Deutsche Bank and VTB to take another shot. They in turn have been advertising a 20% stake at a market valuation of $5 billion for the entire company.

There is no justification for this number. In 2011, the EBRD announced it was spending $170 million for a 21.6% stake. That implied a valuation of all of Lenta at $787 million. The EBRD claimed [9] it was making its investment to “support improvements in corporate governance and transparency as well as improved operational efficiency in a successful Russian company.” Implied in the announcement is that the total value of EBRD’s stake, together with that of TPG and VTB, came to $1.14 billion. This in turn implies the calculation of 100% of Lenta, as of August 2011, was $1.21 billion.

The new asking price, according to the selling shareholder TPG and its underwriters, is four times that figure.

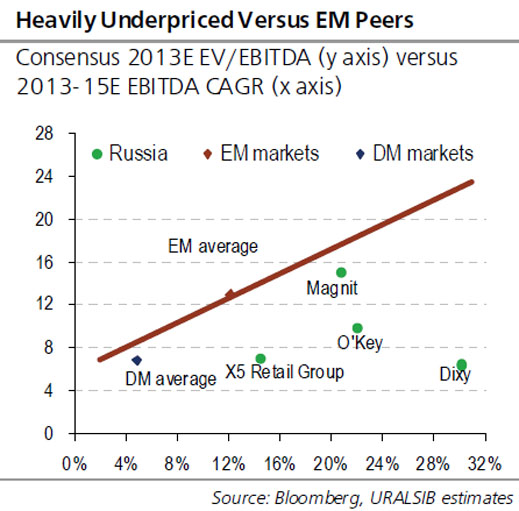

Without elementary data an auditor will sign as authentic, there is no telling whether such numbers are comparable to the valuations of Russia’s listed retailers, or more shots in the dark. A recent report by Uralsib Bank on the share prices and prospects of Lenta’s domestic rivals suggests that they are already well ahead of the developed market and emerging market averages for rate of earnings growth. However, with the sole exception of Magnit, they lag behind their emerging market peers in their ratio of enterprise valuation to earnings (EV/Ebitda).

[10]

[10]

According to Uralsib Bank analyst Marat Ibragimov, the market is discounting some of the retailers more drastically than they deserve. “Our analysis suggests that none of the Russian food retail stocks is fairly priced relative to international peers if future EBITDA growth is accounted for. While for Magnit this discount is around 15%, which could be attributed to general Russian market risk, the same discount for X5 reaches as much as 49%, while for Dixy it is as high as 72%. We also found that the difference in investment sentiment between X5 and Magnit explains at least 46 ppt (or almost 90%) of X5’s massive 53% valuation gap to Magnit, while we estimate a fairer valuation discount at only 7%.”

Ibragimov reports also that a fairly calculated market cap for Dixy ought to be $7.1 billion, while for O’Key it should be $5.6 billion. However, their actual market caps in today’s market are $1.8 billion and $3 billion, respectively. In today’s market too, X5 is just $4.9 billion; Magnit is at $26.3 billion.

Since the start of this year, the share price trajectories of the listed Russian grocery chains have differed markedly. Magnit has jumped by 36%; X5 has retreated by 2%; O’Key is down by 6%; and Dixy is flat

Since Lenta is refusing to meet the disclosure, accountability and governance standards of these competitors, and TPG’s conduct adds to the risk discount, it is difficult to imagine these listed rivals of Lenta will support a sale price of $5 billion for Lenta.

That turns out to be nothing more than a bet on Russian consumer income continuing to rise, sustaining growth in grocery sales. Here’s the wager, according to Moody’s report on Lenta: “Food retailing in Russia presents attractive fundamentals for growth, underpinned by (1) the large size of the market, which has a turnover of RUB9.1 trillion, or around $300 billion (including beverages and tobacco), making it the fifth-largest food retail market in Europe and the ninth-largest globally; and (2) the strong historical growth of the market, which had a compound annual growth rate (CAGR) of around 13% over 2009-11, as reported by Russian Federal Department of Statistics (Rosstat). Aside from the size and dynamism of the sector, its attractiveness is reinforced by the fact that modern retail still accounts for only around 60% of the market and will continue to win market share via organic growth from street retailing. We expect that domestic food retail market will continue to grow in 2013-14, with a CAGR of 8%-10% in nominal terms on the back of growing Russian GDP, a low unemployment rate and moderate growth in real personal incomes.”

So why bet on Lenta when its rivals meet much higher disclosure and shareholder standards?

According to Moody’s, “we also positively evaluate Lenta’s focus on a single format (hypermarkets) given (1) a significant undersupply of hypermarkets in Russia, with only three shops per 1 million people vs. 13 shops in Europe; and (2) strong historical growth of hypermarkets’ selling space in 2006-2011, with a CAGR of 30% (as estimated by research company “Planet Retail”), which is being observed widely in emerging markets.”

When Lenta was asked to clarify its performance and its value, spokesman Mogileva responded: “We are responsible for the operational management of the company. For questions regarding the IPO and development strategy it is better to ask shareholders.” They too are shtum.