By John Helmer, Moscow

It can be no surprise, not even to Russian dunces, that Suleiman Kerimov, the only Russian oligarch and senator of the Russian parliament who has never answered a question in public, has been trying to cash out of Polyus Gold, and can find no takers. Especially not at the current price of gold.

Why then would Polyus Gold report this week that it has discovered that Natalka, in Magadan, the largest new goldmining project in Russia, has vastly less gold in reserve and resource than it has revealed to shareholders before? Why reveal that the loss of future gold sale revenues just announced would be worth $52 billion at the current gold price?

Answer: having no alternative to recover his capital from Polyus Gold by selling out, Kerimov is sacrificing market capitalization of his company stake, and by halting the expenditure of cash on the Natalka mine, Kerimov has decided to put the money into his own pocket as dividends.

In economies outside Russia, this is called disinvestment, cash-stripping, even money laundering, especially if, as in Kerimov’s case, the dividends flow to Switzerland. In the Russian economy, the name for this used to be oligarch capitalism. Since the start of civil war in Ukraine and the sanctions war against Russia, it is called crony capitalism. Except that Kerimov doesn’t appear on any government’s proscription list – except for Belarus. And that’s another story that can be read here [1].

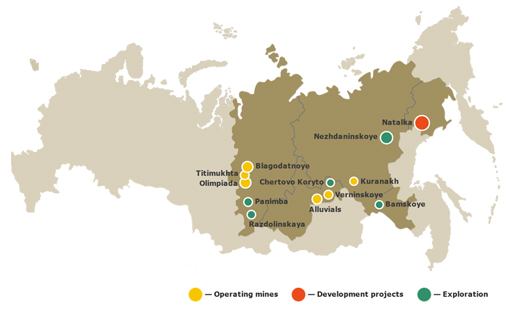

Kerimov owns [2] 40.2%, and controls another 37.8% of London-listed Polyus Gold. He bought out Mikhail Prokhorov in February 2013. This week, on November 13, Polyus Gold announced [3] that the Natalka mine – the big red spot on the company’s map of its operations – has up to 20% less gold in its reserves and up to 65% less gold in resource, two of the standard categories of mineable metal on which the value of the company’s assets can be calculated, and its market capitalization and share price derived.

The company release says “commissioning of the project in 2015 is no longer targeted”, which is pussyfoot for stopping the project altogether and at once.

Until now, the company has been reporting [4] Natalka to be the biggest source of its future gold and thus future earnings. Proven and probable reserves at Natalka amounted to 613.8 million tonnes of gold-bearing ore and 31.6 million ounces of gold. These numbers were almost equal to the total ore and aggregate gold of all Polyus Gold’s active mines combined. Natalka’s measured, indicated and inferred resources were reported at 1.1 billion tonnes and 60 million ounces. Those numbers represent just under half the 2.3 billion tonnes of aggregate ore, and 47% of the aggregate gold. The company reports several well-known international mining and geological consultancies for the calculations. Those for Natalka came from an audit by Micon International in February 2012.

A close reader would have understood that when Prokhorov controlled Polyus Gold, he maintained the fiction of El Dorado at Natalka, because the Kremlin wouldn’t release Sukhoi Gold, a much bigger and more accessible gold prospect in Irkutsk region; and because Prokhorov was hoping to gull a major international goldminer into buying him out of Polyus Gold at a premium. Even then-President Dmitry Medvedev recognized the scheme on September 24, 2008, when he upbraided Prokhorov and the company for failing to invest. “I understand that it’s difficult for businesses to work, that we have an unwieldy bureaucracy, but don’t whine,” Medvedev warned [5]. “If gold mining profits are too marginal for you, give up this work; we’ll find someone else. If you want, we can take the license back.”

Two years, and more abortive scheming by Prokhorov later, he announced he was taking over the chief executive’s job. The company share price kept falling; the gold price kept rising. Publicly, Prokhorov conceded “mistakes”, but not the big one which the other goldminers, the stock market, and Prokhorov’s former shareholding partner Vladimir Potanin had all acknowledged – that Polyus Gold was over-valued. For the history and the detail, read this [6]. In 2011, Barry Ehrlich, then of Alfa Bank in Moscow, warned that Natalka remained a fiction on the Polyus Gold books, because no serious investment in bringing the mine to production was intended [7].

In early 2013 Prokhorov persuaded [8] Kerimov to pay $3.62 billion for his entire 37.8% stake, broken up into pieces to front-men so as to fool the UK market regulator that there was no violation of takeover and minority shareholder rules. Noone was fooled. Today at current market capitalization of £5.7 billion, and an exchange rate of $1.57 to the pound, the stake is worth $3.4 billion. Kerimov and his associates can count a 6% loss of capital value, not to mention their bank financing charges.

In taking cash when he did, Prokhorov has proved that he, not Kerimov, understood the dumb money effect. That’s the well-attested behaviour of small or poorly informed investors to buy after the market has risen or to sell following a market drop. The dumb-money pattern, economists say, occurs when the returns investors earn tend to be less than the time-weighted returns of the assets in which they invest. Investors can counterbalance this tendency by making predictions that place more weight on past results and less on recent outcomes [9].

In short, it’s the timing, stupid!

In April of this year, Polyus Gold reported that “due to unfavorable market situation, the Company has decided to introduce changes to the plan of Natalka project development [below] and to put off until the year 2015 the commissioning of the mining and processing facility which previously was planned for the summer of 2014 [10].”

That was good enough for the literal-minded at Fitch, the international ratings agency, which declared [11] in July that “Polyus Gold’s strong reserve base of 83.12 million ounces of gold… is currently the third-largest among global gold producers with the above-average gold grade of 2.0 g/t compared with the industry’s average of 1.5 g/t.”

Six years after Medvedev warned Polyus Gold not to do that, Kerimov was, er lying about his intentions. This week they became plain [3]: “Preliminary findings suggest a 15-20% downward revision in the resource and a 55-65% reduction in the reserve estimates due to a change in the interpretation of the deposit mineralisation, the more stringent requirements of JORC Code (2012) compared to JORC Code (2004), the application of updated economic assumptions and an increase in cut-off grades…Once completed, the re-estimate of the Natalka ore reserve is expected to result in a non-cash impairment charge to the book value of the project. The scale of the impairment charge is yet to be determined.”

Depending on Kerimov and his board (below), the impairment is likely to push Polyus Gold into loss-making. But the company is saying that won’t happen before January 2015 at the earliest.

The Polyus Gold board as of March 2014 (left to right): Ilya Yuzhanov, Bruce Buck, Adrian Coates, Edward Dowling, Igor Gorin, Pavel Grachev, Anna Kolonchina, Kobus Moolman.

Until then, however, and for calendar year 2014 Polyus Gold can be expected to declare a profit and a sizeable dividend.

The good news, issued the same day as the Natalka write-off, is that “Polyus Gold International Limited announces that due to strong production delivery and ongoing operational improvements, the Company is increasing its 2014 guidance for gold production by 5% to 1.68-1.72 million ounces compared to 1.58-1.65 million ounces as previously announced. In 9M 2014, the Company produced 1,236 thousand ounces of refined gold from continuing operations, which is 4% more than in 9M 2013 [12] (1,185 thousand ounces).”

For the September quarter, Polyus Gold says [13] gold sales reached $603 million, a 14% increase over the June quarter. In the nine-month period to September 30, gold sale revenues are estimated to be $1.58 billion, down 6% on the same period of 2013.

Why then has Polyus Gold announced that it is ditching Natalka? Kerimov’s office at the Federation Council doesn’t respond to telephone calls, and at Nafta Moskva holding a secretary said the press office has been abolished. “We can comment on nothing,” she said.

According to Polyus Gold documents [14], after the takeover in 2013, Kerimov arranged a near-tripling of the dividend payout for 2012 of $320 million; that was 33% of adjusted profit. A plan to suspend the dividend payout for 2013 was adopted in May after heavy impairment charges reduced the bottom-line for last year. There is no sign what the control shareholder plans to do for this year [15].

A leading investment banker for Russian miners explains what has happened: “Top down Kerimov’s team has been generally overwhelmed by having to run a large gold mining concern as they are new to the industry, whilst realising that there is little chance for him to realise value in this investment, especially in the current environment. One way to recoup value is to maximise dividends. The best way to underpin that is to delay large capex [capital expenditute] items. Many gold-mining companies are doing the same after years of excessive outlays on low-return projects. I also doubt that [Kerimov’s] attempts to sell down a stake in the Natalka project, or to attract debt financing have been successful. Add to that the fact that Natalka has always been well known for its local management team, which been incentivised to keep the project going for a long as possible at the most expense.”

“The decline in resources and reserves can be explained by a change in cut-off grades and a tighter block model. That does not seem too drastic. But in itself it is not a reason to stop the project as it’s still a very big project. But in the current climate [Kerimov] just can’t say that too loudly. As for Mikhail Prokhorov, he just traded very smartly, again! Another case of dumb money.”

This morning the Bank of America-Merrill Lynch issued a note on Polyus Gold, reacting to the Natalka closure with the headline: “Downgrade to Underperform… Question: Why is this company London listed? Take a look at PGIL LN