By John Helmer, Moscow

Ten months ago in Russia, the venerable Chinese idea of penitence silver was proposed as a method of making the most powerful wrongdoers of the land pay for their sins — at least their original ones. It was recommended as an alternative to that Bolshevik cue, Expropriate the Expropriators!; the Khodorkovsky remedy, or the Chinese invitation to commit suicide (allowing the heirs to retain the dead man’s estate).

The original idea was Emperor Qianlong’s, whose 59-year rule came to a close in 1795, when he decided to step down from the throne. His plan was to prepare a retirement home in a corner of Beijing’s Forbidden City, and stock it with treasures to keep his mind occupied instead of power politics.

The latest Chinese research reveals that Qianlong used to commission miniature models of what he had in mind for interior decoration, and send them off to wealthy bureaucrats, generals, and business types on whom the emperor’s Secret Accounts Bureau had enough evidence to send them to the chopper. The targets were told that they could either finance the emperor’s fancy; or face trial and punishment for their crimes. The response was almost unanimous – approximately five million ounces were subscribed. The nickname at the time for the payoff was yizui yin – penitence silver [1].

Prime Minister Vladimir Putin didn’t have interior decoration in mind when he opened the tab from the Secret Accounts Bureau at yesterday’s pre-election session at the club of oligarchs. He may have in mind a fund for the Russian Commonwealth into which he now proposes they will contribute, with the invoice still to be composed in proportion to the size of the ripoff.

Here is what Putin said, according to the official translation [2] into English of the Prime Ministry:

“We should be straightforward in admitting that the existing attitude toward entrepreneurship and private property dates back not only to our Soviet past, although it does have roots in this period, but it also has to do with what was going on in Russia in the 1990s. We have spoken a great deal about this, and we know that business back then amounted to nothing more than slicing up the state-owned pie. Certainly, we need to turn this page as well. I spoke with Mr Yavlinsky about it. He is right when he says that we need to close this period, I agree. There are different ways to do this. We need to discuss them with society and with experts, but we must do so in such a way that society agrees with the resolution of problems dating back to the 1990s, including patently unfair privatisation and auctions of all kinds. The solution lies in either a one-time contribution or something else, but we need to think about it together. I believe that society and particularly the entrepreneurial class are interested in finding such a solution. We must resolve this issue.

“What we absolutely have to do is ensure public legitimacy of the institute of private property and public trust in business. Otherwise we will not be able to develop a modern market economy, let alone create a healthy civil society that is not divided by deep contradictions, since they would get in the way of the evolution of our society and would interfere with economic growth and economic freedoms. We need to put an end to this.”

The tone of the response from the investment banks and business media is already more categorical than Putin’s tentative.

| “This opens an enormous can of worms that stretches right back to the beginning of the post-Soviet period,” said Roland Nash, chief strategist at Verno Capital, a Moscow hedge fund. “The assumption is that property rights |

|

This is not a question professional hedge fund strategists need to debate, especially not in public. They simply buy short-sell contracts on the shares of the listed oligarch companies. If between now and Election Day in three weeks, those share prices look like disconnecting from the price of crude oil or other commodities, falling instead under the penalty pressure, the hedge fund will be able to capitalize on pure oligarch risk, and help itself to hefty profits.

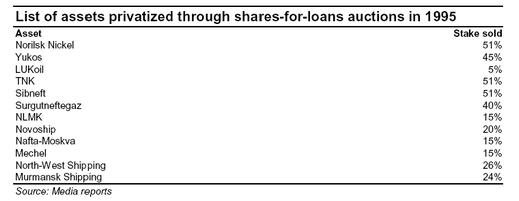

Here is Alfa Bank’s tabulation of the companies which would be targeted if Putin intends to tax the difference between market value and price paid in the shares-for-loans schemes:

Other oligarchs would become vulnerable to the penitence tax if Putin decides to attack transfer pricing, most especially Oleg Deripaska’s Rusal and Iskander Makhmudov’s Kuzbassrazrezugol.

Putin also made the point that his target is broader than the shares-for-loans schemes. Referring to an additional measure he favours for taxing luxury expenditure, he explained his reasoning with a combination of economic and moral terms. “It should become the universally accepted payment for refusing to invest in economic growth in favour of hyper-consumption and vanity. I’d like to call your attention to the following fact. Many of you sitting here have known me for years, and they know what I’m about to say. People in so-called developed economies, whose capitals pass from generation to generation and might be 100, or even 200 years old, don’t look any different from the rest of the crowd. Unfortunately, this is not always the case in Russia….I’d like to say that this tax on wealth is not fiscal in nature. No one is going to overstate its fiscal importance. The fiscal component of this measure is insignificant. This is sooner a moral standard and I’d like the business community to understand this. It’s also obvious that this tax should not be levied on the middle class. We must very clearly define the principles and criteria for imposing this tax. I think we must elaborate these criteria in an open dialogue with society and, of course, with the business community. We must also utilise modern mechanisms of public communication and appraisal of government decisions in applying this measure.”

No Russian policymaker since 1991 — none since 1917 — has ever spoken like that. The analysis of Alfa Bank’s chief economist, Natalia Orlova, confirms as much, but puts a price on the institutional and administrative problem Putin is exposing. “As Putin was speaking broadly of the malpractice of the 1990s, it is unclear whether he meant this list only. In terms of the potential size of the charge, Putin hinted that the potential taxable base would be close to the current market price of an asset; however, the proposed tax rate has not been revealed. The topic is thus entirely subjective and leaves huge uncertainties for the business community.

“Putin’s speech also has wider implications for the market overall. We understand that initially the idea looked like a “tax amnesty” approach, focused on lowering the legal risks to large business and thus to improve the business environment. However, in the present weak institutional environment, and with the weak legal system in particular, Putin would become the sole guarantor of “cleaned” property rights. In this scenario, this potential privatization charge would cause additional capital outflow and lower investment activity. In turn, this charge system would substantially reinforce the position of state companies, reducing economic efficiency and limiting economic activity. While we wait for further details, we expect Putin’s proposal suggests an increase in the risk premium for Russian assets.”