By John Helmer, Moscow

Vadim Moshkovich – Senator from Belgorod, owner of Rusagro (aka Ros Agro Plc), which sold its shares in London last week — has been singing this [1] golden oldie from The Searchers (1963). Don’t miss the last chorus line: “I’ll never ever let you go…Oooooo, Oooooo, Ooooo” Rusagro was 94% owned by Moshkovich until the initial public offering (IPO) which was implemented in London last week; his wife, Natalia Bykovskaya, owns another 1%, both of them through Shiny, a British Virgin Islands-registered company. Vadim Basov, their employee and chief executive of Rusagro, owns 5%. Basov bought his stake from Moshkovich a few days before the listing began, paying $15 million. He and Moshkovich thus valued their company at $300 million.

But Rusagro is reported in the trade media to be the third, possibly the second largest sugar producer in Russia (after Prodimex and Razgulay). It reports assets worth a total of about $1.4 billion, and last year, when Sberbank was reportedly intending to buy most of the shares for sale, the market was asked to value the company at between $1.2 billion and $1.6 billion. This month, almost a year later, the irrepressible Bloomberg reported (according to “two people with knowledge of the sale”) that Rusagro was valuing itself at between $1.8 billion and $2.2 billion – a 37% to 50% premium over last year’s IPO attempt.

What can have lifted the valuation of Rusagro so strongly, and what reason would a creditor bank, or state lender like Sberbank, have for accepting this liftoff in Moshkovich’s share value, unless that is already pledged and collateralized for Rusagro’s current debts of more than $735 million? Who else would gain from a premium-priced share, apart from Sberbank and Alfa Bank, as Rusagro’s biggest creditors?

In addition to sugar growing, processing and refining, Rusagro has a meat division, an oil and fats division, and other agro-businesses. But in the latest report for 2010, sugar accounts for 66% of the group’s sales, and 57% of its earnings (Ebitda). Rusagro claims to be “a leading Russian sugar producer”, and reports that it accounts for 16% of the domestic sugar produced, processed and sold in the Russian market. The company says it has the ambition “to become the largest player in the sugar market in the Commonwealth of Independent States”. But it won’t assist investors or the markets at large by comparing its market shares to those of its domestic peers, and it won’t identify its competitors.

For a long time Russia has been the world’s biggest raw sugar importer. In the Soviet era, it was supplied by Cuba and other countries in exchange for oil and other commodities and goods. The dynamics of this business changed dramatically after the collapse of the USSR in 1991. By 2005 Russia was refining almost 3 million tonnes of raw sugar, most of which was imported from Brazil. But – and this is the key to the current business rivalry in the Russian c sugar sector — the share of domestic consumption produced from imported sugar has been declining, and import substitution by domestic sugar beet growers and processors has gained in strength and market share.

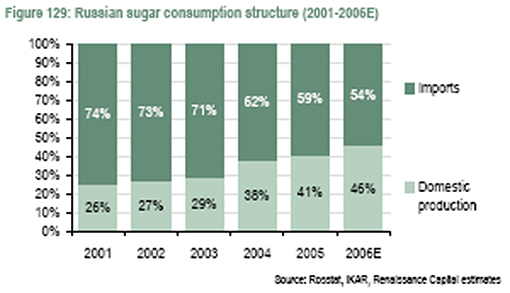

One of the best reports in the marketplace on the Russian sugar business, and who runs it, was produced in 2006 by the Renaissance Capital (RenCap) analyst, Natasha Zagvozdina. Since then neither she nor Rencap has reported in detail on Rusagro. Here is her chart on the growing role which the government-aided sugar producers have been playing in the Russian sugar market up to 2006:

Almost five years ago, then, Zagvozdina was forecasting that in the Russian sugar market, “moderately high consolidation will increase. There are more than 90 sugar producers in Russia. Three producers – Prodimex, Rusagro, and Razgulay together accounted for 41% of all white sugar sales while the share of the top five was 57.4%. Overall, 27 medium and large sugar enterprises in Russia account for 80% of total production. We consider the consolidation level in this segment to be moderately high and expect some more industry consolidation. High domestic white sugar prices result in growing investments into sugar beet

production.”

| Here is the market-share forecast by Rencap from 2006: |  |

“Prodimex (21 sugar plants, FY06 modernisation capex $30mn) is looking to increase its market share to 25%, its volume of own produced sugar beet processing is forecast to grow from 3.1mn tonnes to 3.6mn tonnes in 2006.

Rusagro (7 sugar plants with an outlook to increase number of plants to 12) plans to invest up to $100mn in 2007-2009 to modernise its sugar refineries. It also plans to increase its market share to 25%.

Evrosevice (12 sugar plants in Russia and 6 in Ukraine). Sugar revenue in 2005 $360mn. Also involved in grain processing and trading, meat and dairy production.”

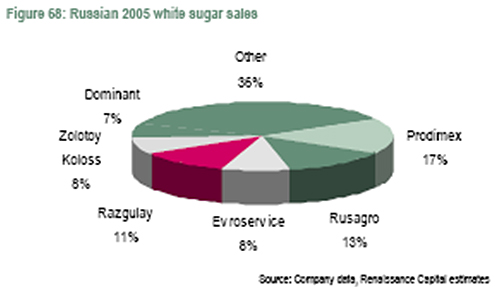

Here too is Zagvozdina’s charting of the domestic market carve-up by the main sugar companies in 2005:

If the London market judges a proprietor or a company on its performance, it appears that at 16% today, Rusagro has fallen well short of its 25% market-share target. On the other hand, Rusagro’s financial data show that the sales figure for 2010 of Rb31 billion ($1.02 billion) was up 26% on 2009. At Rb5.2 billion ($168.5 million), bottom-line income was up 122%.

Moshkovich cannot be found easily in the documentation circulated last week by his company to London investors. One reason – the company doesn’t publish shareholding or financial reports on its website. Its spokesman, Sergei Tribunsky, said today that Rusagro will not disclose its prospectus, or the audited, international-standard financial reports for its last three years “because of the silence period of 30 days since April 14”.

So to understand what Rusagro was selling, and how successful the sugar oligarch was, you have to find someone who received a prospectus and is willing to share it. Here it is [2].

And if you look carefully at Rusagro’s corporate governance code, here is what the prospectus reveals – no code at all: “Although we are incorporated in Cyprus, because our shares are not listed on the Cyprus stock exchange, we are not required to and do not comply with the corporate governance regime of Cyprus. In addition, notwithstanding that a substantial majority of our operations are conducted in the Russian Federation, because we are a Cyprus company we are not subject to and do not comply with the corporate governance standards applicable to Russian companies, except in so far as our Russian incorporated subsidiaries are required to comply with the corporate governance requirements contained in Russian company law.”

The history of Moshkovich’s asset accumulation is also ignored. The Russian media reports on the company’s history are replete with allegations that he used unlawful asset takeover tactics to fill out his sugar division and also his seed and vegetable oils division. It is also alleged (in an unsubstantiated report by Kommersant, February 26, 2006) that Moshkovich sought his seat on the Federation Council to assure himself of immunity from prosecution, in the event of repercussions from this history. There is no comment from Moshkovich at his Senate office to the claims, allegations, and innuendoes. This silence doesn’t make them more credible, nor Moshkovich in any way culpable. But the silence doesn’t make his company creditable either.

This is the only history of his company which the prospectus provides: “OJSC Rusagro Group owns 100% less one participation interest of LLC Group of Companies Rusagro, which was formed on February 3, 2003. The predecessor to the Group was founded in 1995 to supply Ukrainian white sugar to major Russian confectioneries, and since then the Group has developed into a diversified food processor by expanding its operations into sugar processing, meat production, agriculture and oil and fats production.”

The company acknowledges there are risks associated with Moshkovich’s dominance:

“Our controlling beneficial shareholder and his family have the ability to exert significant influence over us, and their interests may conflict with those of other holders of our Ordinary Shares or the holders of the GDRs.

• We have engaged and may continue to engage in transactions with related parties that may present conflicts of interest.

• Our minority shareholders or minority shareholders of our subsidiaries may challenge past or future.interested party transactions or other transactions, or may not approve interested party transactions or other transactions in the future.

• Speculations or allegations about the beneficial shareholder or senior officers of the Group may harm our reputation.”

In its disclosure of related party transactions, Rusagro appears to have played sugar-daddy to other Moshkovich companies, including real estate developer Avgur Estate. In the three years, 2008-2010, it loaned the other Moshkovich companies Rb1.6 billion (about $53 million). It was also on the receiving end of loans from two Moshkovich companies, Finansoviy Resurs and Masshtab, for Rb7.2 billion ($241 million). These latter are all reported as having been cleared by the end of last year.

When Bloomberg reported promotionally in January of this year, it claimed that the company was aiming at raising $500 million in its IPO, “according to the people, who declined to be identified because the matter is confidential.” By this month, as Rusagro’s promoters started their marketing campaign, the fund raising target was down to $330 million. The Russian newspapers were told the shares on offer were “three times oversubscribed” at a price of $15 per share, indicating a market capitalization of $1.8 billion.

The prospectus reveals that 20 million general depositary receipts (GDRs), equivalent to 4 million ordinary shares (5 GDRs = 1 share), have been sold by Moshkovich for the company’s benefit. The prospectus says: “Company will receive gross proceeds of US$300 million from the Offering. The Company expects that its expenses (including underwriting commissions, fees and expenses) incurred in connection with the Offering will be approximately US$12.5 million. The Company expects to receive net proceeds of approximately US$287.5 million from the Offering. The Group intends to use such net proceeds to modernise and expand its production and processing capacity, through expansion of existing facilities and construction of new facilities, and finance potential acquisitions, including acquiring control over additional agricultural land, and for general corporate purposes.”

But if Moshkovich changes his mind about investing the IPO cash in the company, Basov will presumably be ready to give the order. “The Group will retain significant discretion over the use of the net proceeds received from the Offering, and changes in the Group’s plans or in the business environment in which it operates could result in the use of its net proceeds in a manner that is different to that described above.”

The prospectus also reports that in the dealing Moshkovich arranged for his own account in last week’s IPO, he sold 2 million GDRs (400,000 shares), with another 3 million GDRs (600,000 shares) for sale in the special allocation (over-allotment option) for the underwriters – Credit Suisse, Renaissance Capital, and Alfa Capital. His cash take appears to total $75 million. The ratio of the company’s take to the oligarch’s — 4 to 1.

And that’s what one London market analyst judges to be the reason for the success of the IPO. He goes further: he argues that if Russian oligarch companies selling shares to the international market aim to take cash out of their companies, and expect the markets to pay them off, they are making a bad mistake. If, by contrast, the oligarch owners limit their cash take, and invest in their company’s growth, then international investors may be ready to join them, and will focus, less on oligarch or asset risk, more on the financial growth prospects of the line of business and the company. This, says the source, is the “new paradigm.”