By John Helmer, Moscow

Diamond prices have been growing in the global market since January, but depending on your choice of accounting period, the growth rate is either not much; or not at all; or negative since July. Alrosa, the state-owned diamond miner directed by Fyodor Andreyev (image left), reported [1] its latest financial results this week, noting “positive dynamics in the diamond markets in H1 2013, which resulted in a 7% growth of rough diamond prices since the beginning of 2013.”

The company is hoping to make a start selling 14% of its shares on the Moscow Stock Exchange next month, so it’s putting its best foot forward. A bloc of 7% will come from the 51% shareholding of the federal government; another 7% bloc will come from the Sakha republic’s 32% holding. The regional authorities want the privatization to go no further; so they won’t be too unhappy if share sale demand fails to reach Andreyev’s top of the range valuation at $15 billion. Vladimir Potanin, who was interested in taking over the company in the late 1990s, announced this week he isn’t interested in buying shares, and for good measure accused the federal government of artificially stoking demand [2].

Alrosa’s sales revenue for the half-year came to Rb82.2 billion ($2.5 billion), up 7.4% on the same period of 2012. But cost of sales jumped by 17.3% over this interval, so gross profit actually contracted by 0.4% to Rb42 billion ($1.3 billion). Growing administrative payments, heftier outlays on marketing, and other operating expenses also depressed the operating profit line. Bottom-line net profit fell 10% to Rb14.6 billion ($446.4 million).

A presentation [3] by Alrosa in August revealed that mine output of diamonds in the first half came to 17.1 million carats. That is either growing by 5% since the first half of 2012, or dwindling by 5.5% since the second half of 2012. If you review the production data by the quarter, the second quarter of 2013 was a bumper one. Production was 9.6 million carats, the best quarterly result in years. The financial result for the second quarter of 2013 was growth in bottom-line profit to Rb8.4 billion ($256.7 million), almost three times the level of the second quarter of 2012.

But much of that profit came from the one-time sale of a 51% shareholding in the Timir iron-ore mine in the Sakha region. The buyer was the Evraz steel group. Alrosa’s accountants report the transaction produced cash of almost Rb5 billion ($151.3 million), payable in instalments until the end of 2014. Alrosa also got rid of debts of Rb1.1 billion ($34.3 million) owed by the mine company.

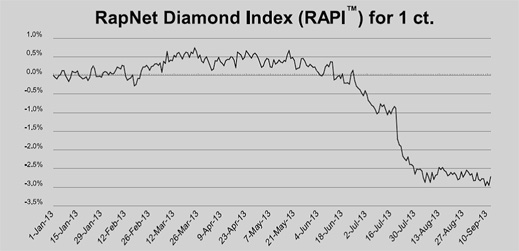

Because the marketable qualities of rough diamonds are many and volatile, and the rough diamond market is an oligopoly of four diamond miners – Alrosa, De Beers, BHP Billiton and the combination of Rio Tinto and Harry Winston, the New York jeweller — gauging the underlying price trend for uncut, unpolished stones is tricky and subjective [4]. PolishedPrices.com of London and Botswana and Rapaport of New York and Tel Aviv are indicating that demand for rough started falling in July, and worsened in August. This is partly the consequence of the rupee collapse in India; this has cut the cash available to Indian diamond manufacturers to buy from Antwerp, where Alrosa sells almost half of its diamond exports, and from De Beers’s sights. Thus, what may have been 7% growth in price for Alrosa’s goods in the six months to June 30 may turn into 7% price discounting from then until Christmas.

Source: Rapaport [5]

The chart from Rapaport suggests the downturn in polished diamond prices commenced in mid-June. An alternative index compiled by PolishedPrices.com hit its year high in late August, and has begun moving downwards this month, although it has not (yet) slipped below the price level when the year began.

Caution — the trend for polished diamond prices doesn’t always track in parallel with the rough diamond price, although this year both price indexes have been moving upwards in tandem in the first half, and now downwards in parallel in the third quarter. So, if the trend for revenue and profit is looking decidedly uncertain, what about Alrosa’s costs and its profitability? Since the company is the most important employer and source of budget in the Sakha republic, can it run the political risk of cutting jobs, reducing payrolls, and reducing personnel costs?

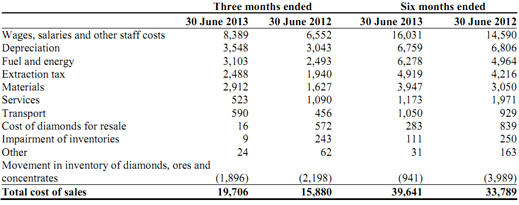

ITEMIZATION OF ALROSA’S COSTS, 2012-2013

The company is showing that its wage bill, at least for mine and production workers, has risen this year by 10%. It is the single largest item of cost, comprising 40% of the aggregate; by contrast, the energy and fuel bill, up 27% on the year, comprises just 16% of the cost total. . Alrosa declines to say what its total employment number comes to. Additional material in the auditor’s notes indicate there has been a cost-cutting effort for administrative wages – down 19% to Rb1.9 billion – and the pay of sales and marketing staff – down 12% to Rb583 million. Cutting white collar staff outside the Sakha republic is easier for Alrosa to do than cutting blue collar and support staff inside Sakha. This reflects the sensitivity of the company as the principal employer of the region. There is also special sensitivity to worker protest at the local level.

For several years Alrosa has been the target of a regional, as well as international, campaign by unions to release from prison Valentin Urusov. He was a maintenance worker at the Udachny mine, one of Alrosa’s largest, when in 2008 he attempted to establish an independent union. A membership drive and public protests threatened the mine with a shutdown of production. That was unheard of until then. But Urusov was arrested, threatened with summary execution, and then tried for possession of a small amount of hashish. Convicted, released on appeal, and then in 2009 imprisoned for five years, the case has been documented in testimony from Urusov and his supporters, and amplified by the international union movement outside Russia. A report on the case by Andrei Veselov in Russian Reporter in August 2012 has been translated into English, and published [6] in this New York source in January of this year.

For several years Alrosa has been the target of a regional, as well as international, campaign by unions to release from prison Valentin Urusov. He was a maintenance worker at the Udachny mine, one of Alrosa’s largest, when in 2008 he attempted to establish an independent union. A membership drive and public protests threatened the mine with a shutdown of production. That was unheard of until then. But Urusov was arrested, threatened with summary execution, and then tried for possession of a small amount of hashish. Convicted, released on appeal, and then in 2009 imprisoned for five years, the case has been documented in testimony from Urusov and his supporters, and amplified by the international union movement outside Russia. A report on the case by Andrei Veselov in Russian Reporter in August 2012 has been translated into English, and published [6] in this New York source in January of this year.

Alrosa was asked to respond to the main allegations in this report – that Urusov was charged and convicted on trumped-up evidence; that the police officer responsible for the operation against Urusov has had a corrupt relationship with Alrosa, and currently works for Alosa after losing his police post and being convicted of “abuse of power”. The Alrosa spokesman declined to respond.

Urusov was released in March of 2013, a year ahead of the sentence term. He declined to answer questions.