By John Helmer, Moscow

If Sergei Frank, chief executive of Sovcomflot, the state-owned Russian shipping company, had not been judged recently in the UK High Court to be dishonest, vindictive, and unbelievable, a warning from a global ratings agency of potentially bad news to come about his company may not be as serious as the red flag raised this week in London.

On September 28, Fitch Ratings issued a release announcing that it “has placed Russia-based OAO Sovcomflot’s Long-term foreign currency Issuer Default Rating (IDR) of ‘BBB-‘ on Rating Watch Negative (RWN). SCF Capital Limited’s senior unsecured notes, which are guaranteed by SCF, rated ‘BBB-‘ have also been placed on RWN. The RWN is pending completion of a review by Fitch of additional details including but not limited to the issuer’s increased capital expenditure programme over the next few years compared to Fitch’s previous expectations. Fitch expects to resolve the RWN within the next week.”

Why the warning has been issued when just a few days remain before the ratings agency will issue a full report, and no shares of Sovcomflot can be traded in the meantime – its $800 million unsecured bond of October 2010 traded down 3% on Thursday – is not disclosed.

Fitch analysts also won’t respond to questions about the impact of the High Court judgements on Sovcomflot’s standing in the marketplace. Frank and his spokesmen in London and Moscow refuse to comment on the ratings warning, and on the Fitch hint in the release that one of the reasons for the possible downgrade is Sovcomflot’s “increased capital expenditure programme” – that’s chartered accountant camouflage for saying Sovcomflot’s debts have been ballooning, costs rising, and its ability to service its debts dwindling.

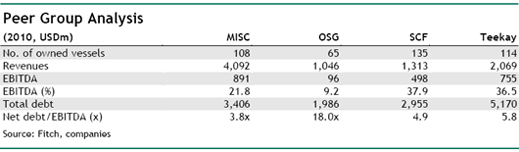

In its previous report on Sovcomflot almost four months ago, Fitch noticed that compared to other leading global tankers companies – MISC Berhad of Malaysia, Overseas Shipping Group of the US, and Teekay of the US – Sovcomflot’s fleet is bigger, but its revenues and earnings smaller. Result – Sovcomflot’s debt is much larger in proportion to its earnings than two of these international peers:

Fitch has tried explaining this away by saying that as a state-owned company, Sovcomflot is protected from bond or loan default by the Russian treasury. Also, according to Fitch: “high leverage credit metrics reflect the bottoming of the shipping cycle.” Read – if there is no decline in crude oil prices or onset of global recession; if the demand for oil tankers revives soon; and if vessel charter rates go up, then Sovcomflot can cover its debts with greater comfort. The obverse, unstated, is now what Fitch’s analysts have gone back to their drawing-boards to figure out.

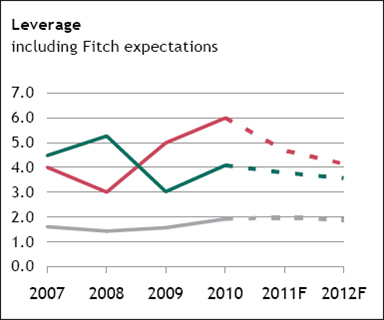

In this June 9, 2011, chart, Fitch tried to show that the future is looking rosy, and so the debt line and the debt to earnings ratio are bound to improve, i.e., go downwards in the chart:

Part of the problem is, of course, that Fitch isn’t as sure of the pencil marks as the chart suggests, especially because Sovcomflot’s debt position today is not half as serious as it will be in three years’ time:

That suggests Frank is living on borrowed time.

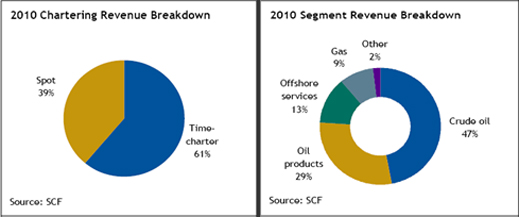

These charts from Sovcomflot show how the company has been betting into the future. Almost-two thirds of its vessel operating contracts are time-charter, so even if the spot market rates improve, the company’s balance-sheet will be slow to record the advantage. Three-quarters of Sovcomflot’s cargoes are oil or petroleum products, so, even if it tries diversification into gas, support for offshore oil drilling projects and other things, it is still firmly locked into the worldwide supply and demand cycle for oil, and for oil tankers.

So, Fitch is uncertain about Sovcomflot’s prospects if the future forecast goes red instead of rosy, or doesn’t arrive soon enough. “Fitch expects tanker freight rates and vessel values to remain under pressure in 2011, with no recovery before 2012 This is mainly due to excess supply of new vessels coming to market in 2011 and 2012. The outstanding tanker order book is estimated at about 28% of the existing fleet, with almost half expected to be delivered in 2011. The vessel supply/demand balance is expected to improve in 2013, resulting in a recovery in rates and asset values.”

In June, when Fitch reported this, it acknowledged the risk that this is too optimistic. “The Stable Outlook reflects Fitch’s view that SCF can withstand a deterioration in the current business environment, should weak shipping market conditions persist for a longer period than expected. The ratings may be downgraded if the market value of SCF’s unencumbered assets (USD1.3bn as of March 2011), plus any available secured credit facilities to unsecured debt, falls below 2.5x. An aggressive vessel‐acquisition strategy that increases balance‐sheet debt would have negative rating implications.”

In short, this is an admission that Frank’s “aggressive vessel-acquisition strategy” may turn out badly if the outlook for the tanker market isn’t stable at all. That is why this week Fitch issued its sudden mea culpa, and promised to report again in a week’s time.

Frank himself has told Fairplay in the past that his predecessor, Dmitry Skarga – now vindicated by several UK High Court judgements on Frank’s attempted prosecution – had made mistakes of strategy by locking up too much of Sovcomflot’s fleet in long-term charters, when spot tanker rates were rising. Frank has also been scathingly critical of Skarga’s attempts to reduce Sovcomflot debt and cut the costs of acquiring new fleet.

These are now the management decisions Frank himself has made, which have returned to haunt the Sovcomflot board, led by Sergei Naryshkin, chief of staff to the outgoing President, Dmitry Medvedev.

As one observer of Sovcomflot’s financial condition claims: “with debts and liabilities of about $3 billion, plus a newbuilding programme for $1.7 billion, of which just $200 million has been paid so far, Frank is facing the prospect that he is building two VLCC’s [Very large Crude Carriers] with strong chances to be laid up straight after delivery.”

The problem of Sovcomflot’s tanker costs was flagged much earlier, before tanker rates started to collapse [1].

“It is interesting to compare the fortunes of Sovcomflot during Skarga’s tenure with that during Frank’s”, another maritime industry source comments. “If Frank had continued with Skarga’s strategy of locking up ships on long-erm time charter, Sovcomflot would have been largely protected from the crash from the autumn of 2008 onwards. But Frank’s vendetta against Skarga drove him to implement strategies which were diametrically opposed to everything Skarga had done, thus abandoning the time-charter market at precisely the time that Frank ought to have been consolidating Sovcomflot’s position within it. By the time Frank woke up to the idea that long-term time charters were not such a bad thing after all, the rates achievable were substantially less.”

But Sovcomflot is unprepared to address the market now that Fitch has made the issue of potential misjudgement a pressing one. Sovcomflot’s only response to the week’s news has been to issue on September 29 a press release in which the good news about last year’s bond issue was repeated, with fresh laurels thrown in for good measure. “In June 2011 SCF Group received the prestigious award for “Deal of the Year 2010” in the category “Public debt placement in Europe”, for its successful public offer of Eurobonds. The award was presented in New York City at the 24th Annual Marine Money Week, hosted by the international financial magazine Marine Money [2].”