[1]

[1]

By John Helmer, Moscow

@bears_with [2]

Russian oil and gas producers and the state, which taxes their revenues for the budget, will gain from the war on three conditions: if the closure of the Strait of Hormuz remains a short supply shock; if war damage to Arab and Iranian oil and gas fields, pipelines, port terminals, and refineries can be repaired quickly; and if global demand for oil and gas holds steady.

In this new assessment, Vzglyad [3], the Kremlin-backed platform for security analysis, weighs the war benefits and the risks. Published in Moscow on March 3 [4], this was before the tweeted announcement from President Donald Trump that he will keep the Strait of Hormuz open, Iranian shore and naval threats suppressed, and restore maritime movement in the Persian Gulf : “at a very reasonable price, political risk insurance and guarantees for the Financial Security of ALL Maritime Trade, especially Energy, traveling through the Gulf. This will be available to all Shipping Lines. If necessary, the United States Navy will begin escorting tankers through the Strait of Hormuz, as soon as possible. No matter what, the United States will ensure the FREE FLOW of ENERGY to the WORLD”

This translation into English is verbatim; the charts and other illustrations and links have been added for illustration and corroboration.

[5]

[5] [6]

[6]March 3, 2026

When will the conflict in the Middle East become dangerous for Russia

By Olga Samofalova

Even without the official blocking of the Strait of Hormuz, there is a now disruption of shipping in the region. And attacks on Saudi Arabia’s largest refinery and the infrastructure of Qatar, a major LNG supplier, create even more problems for the supply of oil, petroleum products and LNG. Russia is almost the only one to whom the Middle East conflict promises great economic benefits. But only if the situation does not go beyond manageable risks. Where is the line between benefit and harm?

The conflict between the United States and Iran threatens the established global structure of hydrocarbon supplies. Moreover, we are talking about interrupting the traditional flows of not only crude oil, but also of petroleum products and LNG.

Firstly, there is a dangerous situation in the Strait of Hormuz, through which about 20% of the world’s oil and petroleum products exports (from Saudi Arabia, Kuwait, Iraq, United Arab Emirates and Iran) pass, as well as between 20% and 30% of LNG supplies (from Qatar and United Arab Emirates).

There is no official Iranian blockade of the strait, but there is still no normal traffic there.

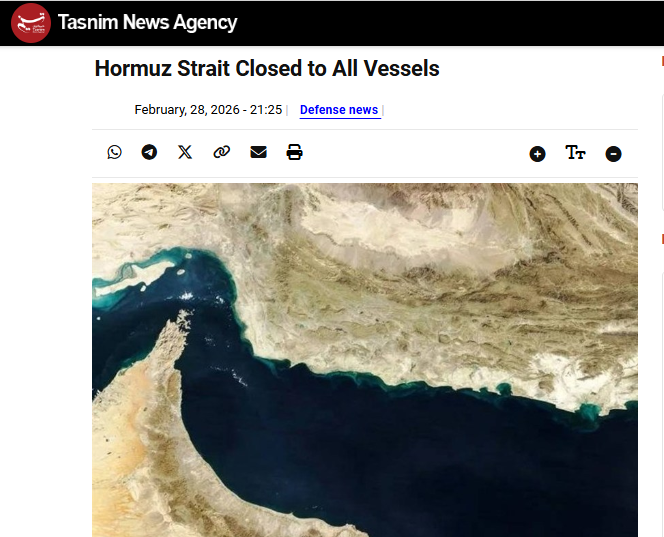

[7]

[7]Source: https://www.tasnimnews.ir/en/news/2026/02/28/3527976/hormuz-strait-closed-to-all-vessels [8] Also: https://www.aljazeera.com/news/2026/3/2/iran-says-will-attack-any-ship-trying-to-pass-through-strait-of-hormuz#:~:text=A%20commander%20in%20Iran's%20Revolutionary,according%20to%20Iranian%20state%20media [9].

Companies themselves have stopped the passage of their ships through the Strait due to the risk of attacks. This was done, for example, by the Danish shipping company Norden, which has a fleet of about 500 ships. The media have reported about three victims of the attacks on tankers transporting crude oil which have been damaged. The deaths of sailors have been reported. Hundreds of tankers carrying oil and LNG have begun to accumulate in the area of the Strait, and hundreds more tankers are now located in areas outside the Strait itself, avoiding its passage.

The Strait of Hormuz is a fairly narrow “gateway” to the Persian Gulf, its width at its narrowest point is only 54 km. Due to the narrowness of the Strait of Hormuz, it is easy to launch missile strikes and attack ships with drones. These risks are deterring and have already led to tanker freight rates doubling since Friday.

[10]

[10]Click on source for enlarged view: https://www.investing.com/indices/baltic-dirty-tanker-chart [11] The Baltic Exchange Dirty Tanker Index (BDTI) is a daily benchmark index measuring the cost of transporting unrefined crude oil by sea. It covers 17 key global routes, focusing on tankers carrying "dirty" cargo—crude oil and heavy fuel oil—as opposed to refined products.

Another problem has arisen due to a drone strike on the largest refinery in Saudi Arabia, in the port of Ras Tanura. After that, Saudi Aramco announced the shutdown of the plant. At the same time, the refinery produces 550,000 [per day]. 40% of the fuel from this plant goes to the domestic market, and the rest is exported.

An attack on the infrastructure of Qatar Energy is also reported, and Qatar is one of the largest gas suppliers in the world, providing almost 20% of global LNG production. According to media reports, QatarEnergy announced the suspension of LNG production. Attacks on the Iranian oil infrastructure may also follow in response. Damage to this oil and gas infrastructure is dangerous because it cannot be launched as quickly as the passage through the Strait of Hormuz. It may take a long time to restore it.

At the same time, experts call the blow to the Qatari LNG the most sensitive. First of all, it’s easier to hurt it. “The bulk of LNG production in the Persian Gulf is concentrated in small Qatar, which is one of the three largest LNG suppliers in the world. This means that it takes much less effort to cause serious damage to the Qatari LNG industry than to damage the oil industry of Saudi Arabia or the UAE,” says Sergei Kaufman, analyst at Finam.

Secondly, LNG is more vulnerable because gas is more difficult to replace than oil. “If part of the shortage with oil can be covered by reserves and the redistribution of flows, then for LNG bottlenecks lead more quickly to price spikes and problems for specific buyers. At best, the consequences will be market-based. A sharp increase in the risk premium, rising freight and insurance prices, interruptions in individual shipments, but without a prolonged shutdown of production. In the worst case, this is a physical loss of volumes if key facilities at Ras Laffan and Mesaieed are stopped, and companies and insurers are actually blocking shipments,” says Vladimir Chernov, analyst at Freedom Finance Global.

“If there is significant damage and repairs will take months, then there will be restrictions on LNG exports. Whereas the market was counting, on the contrary, on an increase in Qatar’s gas production and liquefaction. The global market needs gas, and Europe in particular, because the winter was quite cold and Europe took a lot of gas from underground storage facilities. Therefore, Europe should import more in 2026 than in 2025. In addition, the Europeans wanted to ban the import of Russian LNG under short–term contracts from April 25, and under long-term contracts from January 1, 2027. This means that they need to stock up on even more LNG. With limited LNG supply and price spikes, Europe will find itself in a difficult situation in terms of gas purchases,” says Igor Yushkov.

[12]

[12]Vzglyad appears not to have been aware of the apparent allied strike at the Russian-flagged Arctic Metagaz tanker on March 3. For details, click to read: https://gcaptain.com/russian-lng-carrier-arctic-metagaz-reportedly-ablaze-off-malta-as-maritime-patrol-aircraft-circles/ [13] and https://gcaptain.com/crew-of-sanctioned-russian-lng-carrier-arctic-metagaz-found-alive-after-fire-incident-off-malta/ [13] For the registration and flag history of this vessel, read more [14].

China, which has received large volumes of Qatari LNG, and other Asian markets will also suffer. This region accounts for more than 80% of Qatar’s LNG supplies.

However, in general, absolutely everyone on the market will feel the consequences, regardless of whether they bought Qatari LNG or not, because the price will rise for everyone, the expert adds.

The shutdown of the largest refinery in Saudi Arabia is affecting the supply of petroleum products. “If a large Saudi Arabian refinery is really losing capacity, the country must either spend fuel reserves, increase imports, or redistribute flows within Aramco. This is rapidly hitting the gasoline, diesel, and kerosene market in the region and raising premiums in Asia because buyers are starting to look for alternative shipments,” says Chernov. At the same time, there has already been an increase in premiums in the Asian market of medium distillates against the background of Middle Eastern risks and concerns about supplies through the Strait of Hormuz.

As for the Strait, it is not the very fact of the announcement of the blockade that is important here, but the fact that the disruption of navigation has actually already occurred. “The complete blocking of the Strait of Hormuz is unprofitable for virtually no one and is an extreme and largely suicidal measure for Iran, whose number of allies is already small. China, which is an important economic partner of the Islamic Republic, buys oil and LNG through the Strait. At the same time, the potential for redirecting oil, for example, through a pipeline to the west coast of Saudi Arabia, is quite limited, and the potential for redirecting LNG is zero,” says Kaufman.

At the same time Iran can achieve the same result without officially declaring a blockade: it is enough to carry out selective attacks, increase risks to shipping, and ship owners, insurers and operators will do everything themselves, Chernov notes. In this sense, supplies may be declining right now simply because of the fear of attacks and the refusal of some companies to escort ships through the strait, the expert adds.

The current situation is beneficial for Russia, its economy and budget revenues. Because with all these risks and fears, the prices of all hydrocarbons are rising. Sergei Kaufman agrees that Russian oil and gas is probably the largest beneficiary of the events in the Middle East. Firstly, hydrocarbons are becoming more expensive in all markets. So, the price of Brent on March 2 is already around $ 80 per barrel, and it will rise if the Middle East conflict drags on. Gas delivered the next day at the TTF [15] reference European hub reached $510 per thousand cubic metres on Monday, while on Friday gas cost less than $400. At the same time, [US President Donald] Trump promises to maintain the conflict for up to four weeks.

[16]

[16]Source: https://tradingeconomics.com/commodity/brent-crude-oil [17]

“If tensions persist, but without a massive drop in the physical volume of exports, then Brent may retain an increase in risk, conditionally, plus $5-$15 premium on the “peaceful” level. If the physical loss of oil, fuel or LNG is added, then the range will expand upward,” says Chernov.

According to him, it is beneficial for Russia when the risk is manageable; that is, when oil and gas become more expensive, but global demand has not yet broken down. Then export earnings grow, the budget receives more tax revenues, and the cash flow of the production companies improves, says Chernov. Plus, there is a growing demand for alternative supplies which Russia can provide.

[18]

[18]In addition to the fact that oil prices themselves will go up, we can expect a decrease in discounts on Russian Urals oil. “Russian oil companies benefit directly not only from rising prices, but also from the likely problems for Iranian oil. In recent months, the discount on the Urals grade has been growing, among other things, due to competition between Russian and Iranian oil. After India reduced purchases of Russian oil for both Russia and Iran, China became the main market for which competition increased. Potential disruptions in Iranian oil exports create the prerequisites for a partial reduction in the discount on the Urals grade, which has reached $30 per barrel in recent months. Depending on the timing and intensity of the conflict, we consider it likely that the discount on Urals will return below $20 per barrel,” says Kaufman. Demand and prices for Russian LNG may also increase. “All these events may allow us to increase supplies from the Arctic LNG-2 sub-sanctioned facility. Last year, supplies from the project amounted to about 1.3 million tons, although the first two lines with a capacity of 6.6 million tonnes per year each are technically ready at the plant. The lack of ice-class gas carriers remains an obstacle for Arctic LNG–2,” says Kaufman.

Another advantage is that the EU may reconsider the decision to ban the import of Russian LNG if Iran’s strikes on Qatar result in at least a medium–term halt to Qatari exports, the expert adds.

However, if the situation goes beyond a manageable risk and turns into a global collapse, this conflict will be unprofitable for everyone, including Russia. “The line runs where price increases cease to be a “premium” and turn into a shock to demand and the financial system. The conditional $100-$120 for Brent with a short-term surge in prices is often perceived by the market as a bearable price of risk, and this supports the incomes of exporters. But the longer this level remains, the more likely it is that global inflation will start to accelerate, followed by a slowdown in the global economy, and then fewer barrels will be bought,” explains Chernov.

“When the price of oil goes to $200, the market is usually already in panic mode or there is physical disruption of supplies for months. In such a scenario, the world quickly goes into an economic crisis or recession. This is also a risk for Russia through falling external demand for raw materials, through exchange rate volatility, through higher import and logistics costs, as well as through rising global rates and risk premiums. That is, the high price of oil ceases to be a net plus if it means a global recession and disruption of supply chains,” says Chernov.

[19]

[19]In this 2009 academic study for the World Trade Organisation (WTO), “Oil price volatility: Origins and effects”, it was reported that the recessionary collapse of demand causes much greater and longer impact on the oil price downwards than sudden but short interruptions of oil supply cause price spikes upwards [20].

However, for now, the basic option for the market is not an official lockdown, but wave–like restrictions on navigation. “Today, the main variable is the duration of logistics disruptions in the Strait of Hormuz and the frequency of strikes on the oil infrastructure. It is the duration of the traffic disruption that becomes the key to the price, not statements by individuals,” says Chernov.

[21]

[21]His forecast for the coming weeks is as follows: if military strikes do not expand and shipping is partially restored, the risk premium will remain, but will begin to gradually decrease. If attacks on refineries and gas infrastructure continue, and insurers and operators maintain restrictions, then the market will live in a regime of increased prices for oil, petroleum products and LNG, and the main pain will be in logistics and fuel prices, not just in Brent quotes, the expert says.