By John Helmer in Moscow

In the junior goldmining business, hope springs eternal. So naturally it did, when GV Gold, the Irkutsk-based junior goldminer controlled by Sergei Dokuchayev, went before a recent Moscow miners’ beauty contest to announce a new share issue bid. Maxim Gorlachev, head of corporate development, told the Adam Smith Institute metals conference in Moscow that “an IPO is one of the options we are considering in order to fund growth.” The target for fund raising is $300 million, he said, in order to lift the volume of current gold produced from 111,000 troy ounces to four times that amount, 438,000 oz., in another four years. The shares might be listed and sold in Hong Kong, London, Moscow or Toronto, Gorlachev is also reported to have said.

Asked to confirm what GV Gold is planning (GV stands for its principal gold deposit in Irkutsk, Golets Vysochaishy), the company spokesman told Minesite: “Maxim Gorlachev spoke about the possibility of placement. He did not indicate it as an IPO or a private placement, etc. Moreover, he did not indicate the terms for such a placement, neither in 2010 nor in any other year. Certainly the placement, if it is carried out, will differ from the one planned in 2007. The company has grown. It has become a holding with two mining assets, in Irkutsk and in Yakutia.”

As to what valuation GV Gold thinks the market should put on its current size and future prospects, and hence what target share price it is considering, the spokesman added: “The target share price has not been finalized”. And if GV Gold is considering selling itself to a Russian gold major – Severstal Resources, owned by Alexei Mordashov, and Highland Gold, owned by Roman Abramovich, have been rumoured as potential buyers – that price is also undisclosed.

The latest operating results, issued for last year on February 19, indicate that this year GV Gold hopes to increase gold production by 20% to 133,000 oz; improve yields by completing a third processing plant; add several millions oz to gold reserves; and bring two new deposits into operation – at Bolshoi Kuranakh in the fareast Sakha region, and at Chudnoye, in northwest Komi. Financially, GV Gold’s last published financial statement, for the year ending 2008, reported net profit of Rb1.1 billion (now equivalent to $37 million).

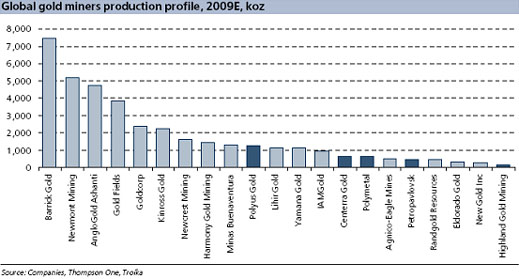

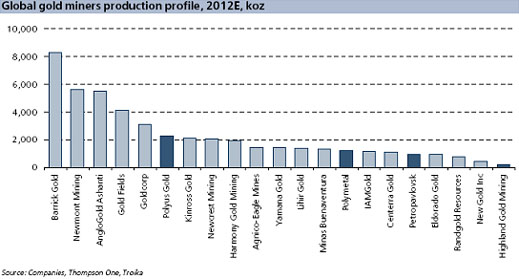

The trend toward rapid growth at the junior level is being led by the Russian major goldminers, according to a recent report by Troika Dialog’s gold analyst, Mikhail Stiskin. “We argue that domestic gold miners are well positioned to stage remarkable earnings momentum from 2H09 driven by a confluence of two factors: healthy margins and volume increases. While from a historical perspective this is nothing more than a confluence, the impact from these developments on the bottom line will be most pronounced.”

Here Stiskin compares Russian goldminer production with their international peers – last year, according to results, and in 2012, according to plans. “There is an abundance of credit available and bottom lines are ballooning,” Stiksin reports. “Senior and intermediate miners are expanding their operational scope not only within Russia but also within the CIS, with Kazakhstan being the prime target. While Polyus Gold and Polymetal’s appetites have largely been satisfied, other miners like Highland Gold Mining, Severstal Gold, Centerra Gold and Petropavlovsk (via a JV with Leader) may pursue inorganic growth [buying other goldmines]. Miners have been taking advantage of the prevailing (so far) optimistic sentiment to sell new/old equity to either deleverage the balance sheet (Polymetal’s SPO) or allow controlling shareholders to cash out (Polyus Gold’s SPO). A number of intermediate and junior producers (Severstal Gold and GV Gold) may conduct IPOs as well.”

In production, GV Gold reported that its 2008 output of just over 4 million oz put it at 8th rank on the Russian gold producers’ table. In terms of reserves and resources, the Golets Vysochaishy (literally, “Bare-Top Mountain”) deposit is estimated to hold 2.3 million oz (Russian categories C1 and C2), with another 3.3 million oz in resources (P1,P2, P3) to be proven in the area. The Sakha region placer deposit, called Bolshoi Kuranakh, is reported to have 2.4 million oz of reserves (B, C1, C2), and 2.8 million oz of resources (P1). “Forecast potential” at the company’s Amur licence area is 1.9 million oz. At his appearance at the Adam Smith Institute conference, Gorlachev reported that these gold resources added up to 16.6 million oz, giving the company a value, he estimated, of at least $500 million.

This is less than GV Gold said it was worth when it tried to sell shares in London three years ago, when GV Gold was producing less gold, and counted significantly fewer reserves on its balance-sheet.

The first report of an IPO plan for GV Gold appeared on the Russian wires in mid-December 2006. The following January-February 2007 saw a concerted effort to sell a 25% bloc of GV Gold shares; the managers were Credit Suisse and Moscow investment bank Troika Dialog. The involvement of Credit Suisse appears to have been arranged by the independent director on the GV Gold board, Reinhard Schmoelz. He used to work at the European Bank for Reconstruction and Development, and before that was a board director and managing director for Credit Suisse in London and Frankfurt. The target valuation of the company reported publicly during this attempt was between $420 million and $515 million.

Promotional claims, reported by Reuters at the time, suggested GV Gold was hoping to “raise about $200 million in a share listing in London and Moscow next month [February 2007] that will help boost output at its Siberian mine….” That suggested a target valuation of $800 million (for a 25% sale). “The initial public offering should enhance the international recognition of the company as well as contribute to the company’s further growth,” Dokuchayev, then chairman of the board, was quoted as saying. “This will be especially important to our strategic plans to increase gold production and ensure the stable growth of gold processing.”

At the time, Chief Executive Sergei Vasiliev said, the February 2007 placement was a success everywhere but in Moscow. “Three-fourths of the book was closed by foreign investors,” he claimed. “But the Russian market didn’t work optimally. Work with [Russian and foreign] investors wasn’t correlated, and we missed the Russian market.”

Vasiliev also claimed that another try would be made, but that pricing and market cap weren’t the overriding considerations. “The idea of the IPO was not to attract funds,” he claimed, “but to establish a public company.” Referring to London listings for Polyus and Polymetal, Vasiliev said: “we monitored [them]. All had a share price fall [after listing]. So we want a stable establishment. Polymetal’s aim [in February] was to attract the money, but we want to be a public listing. So volume [of shares to be sold] will be reduced substantially.”

In May of 2007, Credit Suisse and Renaissance Capital tried for the second time to sell GV Gold shares on the London market, this time with a reduced valuation of the company at $400 million to $450 million. It too failed.

In November of 2007, BlackRock, part-owned by Merrill Lynch, bought 209,000 shares in GV Gold at $80 per share for $16.7 million. This transaction for 10% of GV Gold’s stock apparently valued the mining company at just $167 million. Vasiliev and Dokuchayev were understandably upset that the reported sale price of the BlackRock transaction suggested a drastic discount in valuation to which they had publicly agreed just months before.

BlackRock has refused to corroborate any of the reports of its purchases of GV Gold shares. This has allowed contradictory reports of the size of the BlackRock stake to circulate. GV Gold’s annual report for 2008 – issued in March 2009 – identifies BlackRock as a shareholder, but does not disclose the size of its shareholding. The report counts Dokuchayev and his associates as holding 67% of the shares, with three other small stakeholders with a total of 13.4%. The implication is that BlackRock holds a 20% stake.

In his recent Moscow conference presentation, Gorlachev confirmed that BlackRock had paid $16.7 million for 10% of GV Gold in 2007, and holds 19.99% today, the maximum it can hold in a company that isn’t publicly traded, according to Gorlachev.

The power behind GV Gold is Lanta Bank, which trades much of GV Gold’s output. A closed shareholding company, Lanta is also a family business, run by Sergei Dokuchayev and his two brothers Pyotr and Alexander, and their children. In 1998, when GV Gold was launched, Lanta held 49% of the shares, while Lenzoloto, the gold production association that dominated goldmining in the Irkutsk region, held 51%. Over the intervening years, Lenzoloto has sold its shares, although the Lenzoloto veteran, Vladimir Kochetkov, remains on GV Gold’s board of directors, with an equity stake of 5.7%.

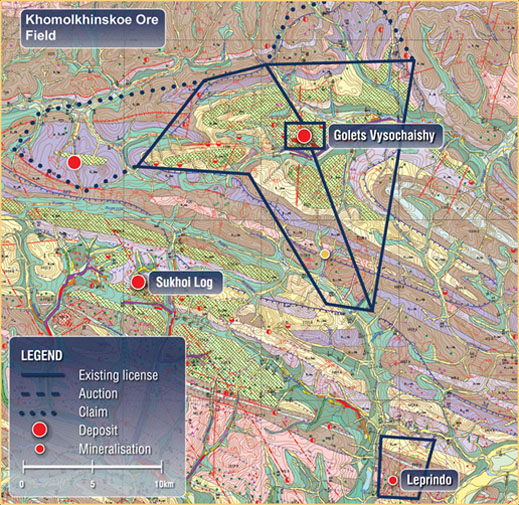

Since BlackRock bought into the goldminer at a valuation of $167 million, it stands to make a threefold gain if GV Gold can strike a target price of $500 million in a new transaction in the coming months. Investment bankers, apparently eager to share in this upside, have also been circulating the story that GV Gold is well placed to gain the support of state conglomerate Russian Technologies, run by Sergei Chemezov, in a bid to take the licence to mine Sukhoi Log. With more than 60 million oz in gold reserves, Sukhoi Log is Russia’a largest unmined gold deposit, and one of the largest in the world. It was once part of the Lenzoloto mining area in Irkutsk, and, as the following map illustrates, the deposits which GV Gold has been mining since 1998 are on the periphery of the main Sukhoi Log licence area.

But there are many contenders for Sukhoi Log; and because an open auction is likely to drive the licence price up to $1 billion, before capital expenditure of another $1 billion is required, the Russian bidders will require finance. This gives the advantage to the frontrunners, Polyus Gold and Polymetal. If oligarch influence counts, as it is bound to do, then Mordashov’s Severstal Resources and Abramovich’s Highland Gold would also be contenders. Avoiding an open auction by state decree, or securing bid financing from a state bank, would enable a smaller goldminer to compete. That appears to be what GV Gold is hoping for. Establishing an international market value for its existing assets and price for its shares is what it is trying to achieve first.

Leave a Reply