By John Helmer, Moscow

There are only so many ways a Russian company can make its performance look better to the markets without resorting to magic tricks.

Ed Balducci was a well-known American magician, but he died long before Oleg Deripaska, the current chief executive of the Russian aluminium monopoly Rusal, owned anything of significance. Ed’s famous trick, known as the Balducci Levitation, goes like this: the magician lifts his arms by his sides and his feet appear slowly to rise a few centimetres off the ground, before they return to earth. The illusion is managed by placing the audience within 3 meters of the performer, and at a 45-degree angle of view. It is the restrictive angle which does the trick.

And so it happens that Rusal and its promoters are trying to position the shareholding markets at a peculiar angle from which the company and its share price appear to be taking off. Take, for example, the appearance of a surge in positive sentiment in the Hong Kong stock market in recent days. According to a press release, the company says its share price “has also increased by 29% to HK$10.50 on 11 November 2010.”

The increase depends on where you start counting. Compared to the initial share price fixed when Rusal launched its listing on the Hong Kong Stock Exchange on January 27, its best price lift so far this year remains 3% below where it started. If up actually turns out to be down, here’s why — and how the illusion was pulled off behind the scenes in the Hong Kong market. The story appears in Lai See, the financial column of the South China Morning Post by Howard Winn. Lai See is the name for the Chinese custom of giving money as a New Year present in a special red envelope:

| “Readers will be aware that there was some excitement in this column earlier in the week at the prospect that the Russian aluminium stock Rusal might finally close above HK$10.80 for the first time this year, the price at which it was listed. It spent half of Monday in this rarefied zone before slumping back to $1.70 by the close. Turnover had rocketed to HK$245 million compared with a range of HK$4-HK75 million in the preceding weeks. We had assumed that its advance was due to increasing enthusiasm for the stock. |

| “However it appears this thought was misplaced. Rusal was taken off the list of designated short selling stocks at the end of October, thereby reducing the number of short sellers. At the same time commodities worldwide were lifted by news of the a second round of quantitative easing by the US and those holding short positions began to feel vulnerable and scrambled to buyback the stock thereby creating a classic short squeeze which pushed up the stock price sharply. |

| “However Lai See has since discovered that Rusal was removed from the short list in error and will be back on the short list on Monday. ‘There was an internal miscommunication,’ a stock exchange spokesman said. ‘We are strengthening our procedures.’ So there’s a good chance Rusal will be back on the slippery slope again next week.” |

In fact, by the close of Friday trading in Hong Kong, Rusal was down 6% to HK$9.96.

From the start of trading, the Hong Kong exchange has done its best to protect the Rusal share price from negative sentiment and falling price. Without explaining what it was doing, or why, between January 27 and March 25, the exchange did not allow short-selling of Rusal shares at all. This prevented anyone betting on the fall of the Rusal share price. A popular combination for share traders – betting on the rise of the aluminium metal price, but covering the bet with a wager that Rusal would fall if aluminium went down – was prohibited while this restriction was in place. Despite this, the Rusal share price collapsed 31% in the first weeks of trading.

The exchange spokesman, Scott Sapp, explained that one in three of the exchange-traded stocks was allowed for short-selling, but in March he refused to acknowledge the reason for the short-selling ban for Rusal, nor say why the ban was lifted in late March. Yesterday, the exchange issued a press release saying that “with effect from 15 November 2010 (Monday), United Company RUSAL Plc (Stock code: 486) will be admitted to the list of designated securities eligible for short selling.” No explanation for the delisting or the restoration.

Hong Kong investment institutions say there have been other forms of protection for the Rusal price which have inhibited short-sellers, and supported a floor for the Rusal price. One of them, the restriction on the lot size of shares allowable in a trade, restricted the amount of small money that could be placed. According to an announcement from Rusal this week, the board lot size is being reduced to encourage positive demand for the shares, and higher pricing. Rusal says: “the board lot size for its shares for trading on the Hong Kong Stock Exchange will be changed from 6,000 to 1,000 shares with effect from 9:30 a.m. Hong Kong time on 13 December 2010. The change in board lot size may improve the liquidity of the shares and enable the company to attract more investors and broaden its shareholder base.”

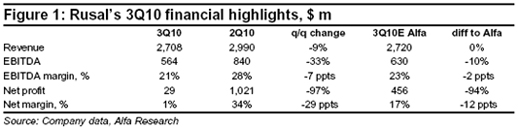

Manipulation of exchange trading rules to protect or boost a share price cannot be effective if the financial performance of the company is transparent. One reason for the downturn that is being predicted for Rusal is that it is selling less aluminium, suffering higher costs, earning less money, and making less profit. A report issued today in Moscow by Alfa Bank metals analyst Barry Ehrlich says the latest company report for the third quarter, ended September 30, is “NEGATIVE owing to rising costs and the larger-than-expected decline in adjusted EBITDA [earnings]. Our revenue forecast was in line with the reported number, which declined 9% q/q owing to lower sales volumes. However, adjusted EBITDA of $564m was 10% lower than we anticipated and 33% below the figure for 2Q10. We estimate that the EBITDA miss was due to an increase in total cash costs that was much greater than we expected, and we expect accelerating cost growth to be one of the main items on the agenda of today’s conference call.”

Rusal’s website presentation of the new financial report makes it difficult to spot the downturn that has occurred between the second and third quarters. Instead, the company highlights nine-month results for 2010 and compares them to the 9-month period of 2009. Another Balducci levitation trick by angling the perspective.

Here’s Alfa Bank’s easier-to-read chart, with the negative changes more obvious:

The small print in the Rusal release reports the company’s cost of sales reached $5,456 million, an increase of 10.8%; of which energy costs are reported to be $1,453 million, up 4.4%. But this comparison is with the 9-month period of 2009. If you look closely at the 3rd quarter costs, and compare them with the third quarter of 2009, the picture is much worse. Rusal admits that costs in the latest quarter came to $1,961 million. That was up 33% since last year.

That reveals a dramatic jump in electricity prices – and one which is especially sensitive in the Hong Kong market right now. All Rusal will admit to is that “the increase in energy costs over the period resulted primarily from the liberalisation of the electricity market in the Russian Federation…Key factors contributing to the increase in Aluminium Cash Operating Costs in the third quarter of 2010 were increases of USD22 per tonne in power, USD34 per tonne in raw materials and USD10 per tonne in other expenses, which were partially set-off by decreases of USD18 per tonne in exchange rate effects due to the appreciation of the Ruble and USD6 per tonne in alumina expenses.”

The reason for the reluctance to broadcast the 33% increase in costs is that Deripaska is trying to list his electricity company, Eurosibenergo, on the Hong Kong exchange. To succeed at that, he needs to explain to potential share-buyers into which of his pockets he intends to put his profits, and into which his losses – Rusal or Eurosibenergo. Since this report was published, Deripaska’s financial advisors have been forced to lower their valuation of Eurosibenergo by 25%, and cut their target for the initial public offering from $2 billion to $1.5 billion. And this is before the prospectus has been released.

Rusal refers to Eurosibenergo without mentioning its name in a disclosure of a year-old pricing agreement between the two companies. This appears to show that the price of electricity from Eurosibenergo will be held down if the London Metals Exchange (LME) price of aluminium fails to rise. “In November 2009,” the Rusal financial report says, “the Company entered into long-term electricity contracts with related parties through 2019-2021. The contract pricing contains a fixed or a cost based component and an LME-linked price adjustment. Management has analysed the contracts and concluded that the price adjustments represent embedded derivatives which were valued at USD570 million as at the end of 2009. Estimates of the fair value of the embedded derivatives are particularly sensitive to changes in the LME aluminium price. A change in the LME aluminium price between 31 December 2009 and 30 September 2010 resulted in a gain from revaluation of embedded derivatives amounting to USD181 million.”

Investors may scratch their heads over who gains, Rusal or Eurosibenerego, from these so-called “embedded derivatives”. Rusal spokesman Vera Kurochkina refuses to answer questions from reporters on the company black-list. Kurochkina herself has been gaining in spending money, and since her promotion to the Rusal board of directors, personal compensation. The quarter-on-quarter financial data reveal that Rusal’s press, investor relations and lobbying bills, for which Kuroochkina is responsible, have ballooned, as the cost of promotion rises to hold back the tide of scepticism. Administrative expenses for Rusal, according to today’s report, came to $172 million in the September quarter, up 25% since a year ago; up 12% since this year’s second quarter.

Rusal’s profit line has also been shrinking significantly over the past quarter. Before tax, the quarterly profit was in fact a loss of $3 million. The after-tax profit line was also down — by 97% compared to the second quarter of this year. It would have been worse if not for a tax credit of $32 million. There is no report of why Rusal received this. The company’s profitability as measured by its operating margin and its net margin was significantly less in the latest period compared to the June quarter.

Leave a Reply