By John Helmer, Moscow

@bears_with

If NATO advanced toward the Russian border with the aim of attacking Russia with weapons made of chocolate, the Russian defense and counter-attack strategy, firing Russian-made chocolate, would overwhelm the attackers in the first wave of Russian creme, praline, nuts, waffle, and soufflé.

That’s because Russians, and not only Russians, think Russian chocolate tastes better, with higher quality of ingredients, more variety, and less synthetics, fats, and sweeteners. In 2001, in the only survey of Russian consumer attitudes towards chocolates, including children, it was discovered that “in the image of domestic chocolate products [there were] in particular, a genuine care for the consumer, sympathy with national traditions and patriotism…. Western chocolate products had associations of vitality, well-being and self-confidence, counterbalanced by greed, artificiality and aggression.”

The only way NATO chocolate can conquer Russia is by the Fifth Column – that is, the takeover of the domestic market by the NATO brands Nestlé, Mars, Mondelez, and Ferrero. And this is exactly what has happened. In the current Russian chocolate market, these four manufacturers account for 61% of revenues – the money Russians spend on confectionery. Together, the two US groups, Mars and Mondelez, hold a 29% market share; Nestlé of Switzerland, 24%; Ferrero of Italy, 8%.

Russian chocolate experts see the future for Russian chocolate in rapidly increasing exports to new markets like China where chocolate eating is negligible. But they predict little chance the Russian chocolate manufacturers will be able to take domestic market share away from the foreign companies. This is because, under the pressure of falling income during the pandemic, rising inflation, and shrinking profit margins, Russian chocolatiers are replacing their traditional ingredients with cheap substitutes, wiping out the taste difference and advantage over their rivals.

The taste for chocolate comes with money. The more of the latter you have in your pocket, the more of the former you put in your mouth. As relatively poor consumers, Russians have valued chocolate for celebrations of anniversaries and holidays, but consumed less in their diets than other Europeans or Americans.

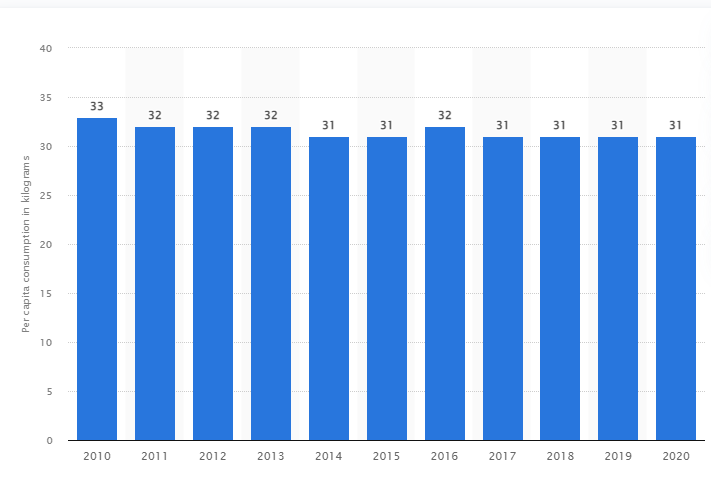

According to the Russian Association of Confectionery Industry Enterprises (ASCOND) in 2018, the consumption of confectionery in Russia had been steadily growing since 2010 by an average of 1% to 3% every year. At the same time, Russian consumers had far to go to match the Germans, who annually eat an average of 34 kilogrammes per head of population; or the British whose per capita average is 27 kg. The comparable Russian level is 25.5 kg. Of that volume, just 5 kg is chocolate.

But that has been growing since Vladimir Putin replaced Boris Yeltsin in the Kremlin. In 1999 the average Russian consumer ate 2.3 kg of chocolate; in 2000, 2.7 kg; in 2001 3.6 kg.

The Putin sweet years peaked at the economic downturn of 2009-2010.

ANNUAL PER CAPITA CONSUMPTION OF SUGAR AND CONFECTIONERY PRODUCTS IN RUSSIA, 2010-2020

(in kgs)

Source: Statista

It isn’t clear whether these static numbers reflect a surfeit of consumer demand, or the calculation by domestic manufacturers that market demand was saturated. Industry media have been reporting that domestic production was stable in 2019 and 2020 at about 4 million tonnes, of which about 16% — one tonne in six – was exported.

Source: https://statinvestor.com/

In 2017, this source estimated Russian consumption at 4.8 kgs compared to the US at 4.4, France at 4.3, and China at just 0.1.

On the other hand, since 2016 Russian consumers added more chocolate to their sweet baskets, and ate chocolate bars more often. As a result, their average consumption for chocolate rose to between 6 and 7 kg by the start of last year. Russia is such a large market in Europe that when Russians started eating more chocolate like this, it became visible as a pressure on the demand side of the worldwide supply of the basic ingredients for chocolate – cocoa beans, cocoa butter, cocoa syrup, and cocoa powder.

THE COCOA BEAN PRICE IN THE WORLD MARKET – 10-YEAR PRICE TRAJECTORY

Source: https://tradingeconomics.com/

Actually, the prospect on the supply side is for increasing production pushing down on the cocoa price for the next two or three years, according to this commodity market analysis: “Favorable rains in top grower West Africa boosted optimism of larger yields, which further pressured the prices. Elsewhere, the International Cocoa Organization (ICCO) in its 3rd quarterly report showed that although grindings increased significantly in Europe (+8.7% YoY), South-East Asia (+3% ) and North America (+6%) they are insufficient to absorb the excess production, while it estimated the world’s cocoa production to go up by 10% to 4.7 million tonnes at the end of 2022-23.” Rabo Bank research has a different view: “Production risks in West Africa with the potential for drier than normal weather in the months ahead. We reduce our previous global S&D estimates lower on the back of weather risk and strong demand: 2020/21 is now seen with a surplus of 123,000mt and 2021/22 with a deficit of -8,000mt. High consumer confidence in Asia may be driving demand growth in the region with plenty of space for a further recovery in the US and Europe.” At present, Russian imports of cocoa beans come mostly from west Africa -- Côte d'Ivoire (86%), Ghana (9%), Nigeria (4%). Most Russian imports of cocoa powder come from The Netherlands and Denmark.

Then Covid-19 struck. The cocoa price was rising in 2020 and it has continued sharply up, then down, during this year. So the domestic price of Russian chocolates was growing at the same time as there was less to celebrate, and less consumer income to do it with. The latest industry reports suggest that average per capital consumption has now fallen from 7 kg to 6.

The taste has changed, too, as manufacturers have substituted imported cocoa ingredients and milk with palm oil and synthetic dairy products and sweeteners. Fr more detail, click to read this and this.

In the only consumer market survey of its kind, the unique Russian taste for chocolate was revealed. The strongest preference was for chocolates in their traditional mixed assortment boxes, followed by chocolate flavoured cakes. Cocoa and chocolate flavoured icecream, yoghurt, and other products trailed far behind. The survey was conducted in the first quarter of 2001 by Megadesign 2000, and was paid for by the International Cocoa Organisation, ASCOND, and the Scientific Research Institute of the Confectionery Industries. Read the full report in English here. Nothing like this has been attempted since 2001.

Source: https://www.icco.org/

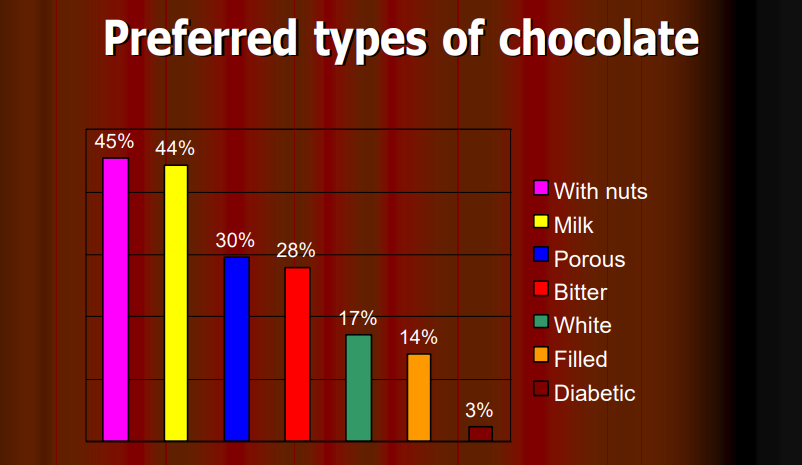

The same study also discovered that for taste and flavouring Russian chocolate eaters prefer nuts and milk.

Source: https://www.icco.org/

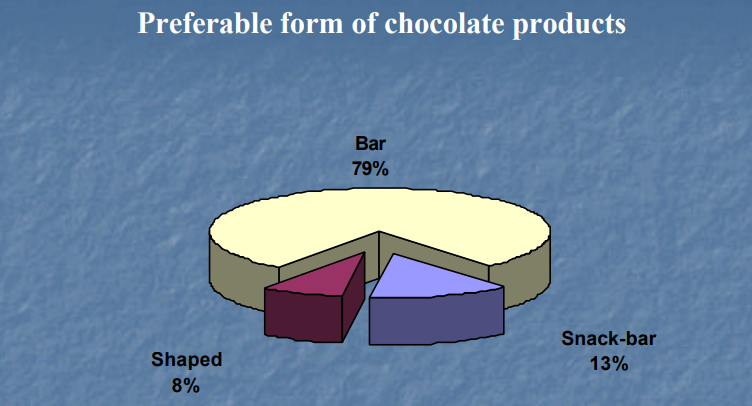

Then as the Putin administration has chewed on, there has been a generational revolution in demand for the chocolate bar instead of the chocolate box. According to the 2001 report, “the favourite type of chocolate product is a bar chocolate; it is mentioned by respondents in almost 80% of responses. Snack bars are consumed mainly by young people, being the preferred form of product for 13% of the respondents only. As to shaped chocolate, it is particularly liked by representatives of the 33 to 55 year age group, which is probably explained by the fact that the product is bought for their children and grandchildren.”

It’s far from certain, though, that the adolescent Russian preference for snack-bar chocolate has erased the traditional preference of boxed chocolates.

The latest report on the Russian chocolate market from Euromonitor, dated July 2021, says: “The gifting of chocolate confectionery for special occasions has historically provided a boost to boxed assortments and seasonal chocolate. While higher unit prices and the restrictions imposed on social gatherings limited sales during COVID-19 in 2020, the improving situation is renewing interest in these products. Chocolate confectionery [is now] set to rebound as consumers return to pre-pandemic lifestyles. The prospects for chocolate confectionery are likely to be influenced by the extent of the measures taken to limit consumer movement as the threat of COVID-19 lingers, including restrictions on access to stores and the pace of the return to the workplace, educational institution or social activities… A wider offer and the resumption of social gatherings [are] set to boost boxed assortments and larger tablets. Boxed assortments and tablets are projected to register the highest retail volume CAGRs [compound annual growth rates] over the forecast period. These categories are set to see activity in terms of novelties and benefit from a widening variety of products and brands.”

This suggests that Russian consumer sentiments towards chocolate haven’t changed much in the past twenty years. In 2001, for example, it was reported that Russians, whatever their age or income level, think of chocolate as a happiness product. “Chocolate products helped consumers to improve their emotional state, relieve stress and enhance mental activity. Chocolate products were intimately associated with happy relationships with children, loved ones, relatives, friends and colleagues. It was a traditional present and a universal treat. …Consumers’ income did not immediately affect the quantity of the products they consumed (except in the case of consumers with an extremely low income). Consumers with different levels of income bought different types and qualities of chocolate products.”

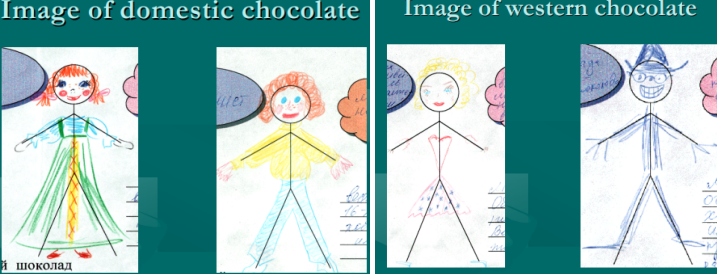

The 2001 survey not only questioned adult consumers individually and in focus groups. They survey also asked children to make drawings to illustrate how they thought of the Russian and foreign chocolate products they had tried. “The following positive characteristics predominated in the image of domestic chocolate products: in particular, a genuine care for the consumer, sympathy with national traditions and patriotism. But negative characteristics were seen as well, such as poverty and diffidence. Western chocolate products had associations of vitality, well-being and self-confidence, counterbalanced by greed, artificiality and aggression.”

HOW RUSSIAN CHILDREN VIEW “AGGRESSIVE” FOREIGN CHOCOLATE

Source: https://www.icco.org/ -- page 54. The bare-toothed, military-hatted image on the far right is also illustrated in the lead image, upper left.

Time, money, war conditions, reproduction and death have accelerated the dominance of the chocolate snack-bar in the market.

Source: https://www.icco.org/

The most recent market reports confirm that the pandemic was bad for sweets in general, chocolate in particular. But this year there has been a recovery of demand. In 2020, sales of chocolate and cocoa products in Russia decreased by 13.3% to 0.91 million tonnes, according to a market analysis by Businessstat. From 2016 to 2019, sales were growing at a rate of between 1.9% and 3%. In 2019, about 1.05 million tonnes of chocolate products were sold in the country, which was 7.5% more than in 2016. But then in 2020, sales decreased by 13.3% to 910,000 tonnes. Businesstat concluded: “Chocolate and cocoa products are an expensive type of confectionery. In the face of a reduction in real incomes, buyers made a choice in favor of less expensive and more nutritious flour and sugar products…

Due to the self-isolation regime, the number of personal meetings and congratulations for the holidays, which are often accompanied by the delivery of sweets in boxes, decreased.”

Predicting the future for Russian chocolate from now through 2025, Businesstat is not optimistic. “In 2021-2025, sales of chocolate and cocoa products in Russia will recover at a rate of 1.1%-3.9% per year. In 2025, 1.03 million tonnes of products will be sold in the country, which will exceed the level of 2020 by 12.8%, but will be 2.2% lower than the pre-crisis level of 2019. The expected stagnation of the incomes of Russians and a decrease in their number will limit the growth of sales of chocolate and cocoa products in the forecast period.”

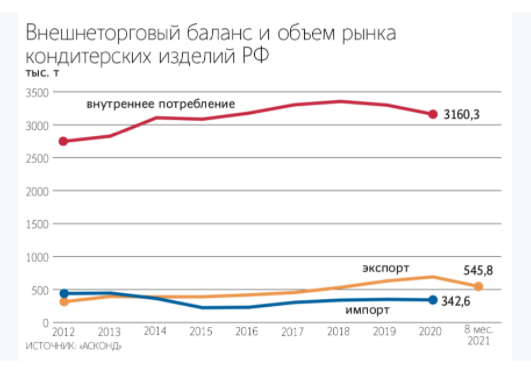

RUSSIAN CONFECTIONERY CONSUMPTION, EXPORTS AND IMPORTS

(in thousand tonnes)

KEY: Red line=domestic consumption; yellow=exports; blue=imports. Source: Vedomosti, November 9, 2021.

This year, Russia overtook Switzerland in chocolate exports and entered the top-10 in the world, according to data published this month by ASCOND. The industry association is also estimating that for this year the export of Russian confectionery will increase by 19.1% to 824,500 tonnes for a value of $1.68 billion. These figures are a record for the Russian industry. Here is the world's top-10, Mars, Mondelez and Ferrero leading Nestlé.

Another recent market study indicates that the chocolate bar is making a faster comeback than the chocolate box. A NielsenIQ study for the first nine months of this year reports that purchase of chocolate bars is up 9.5% year-on-year; packaged non-chocolate candies, up 5%; sweet biscuits and cakes, up by about 2%.

According to ASCOND, 1.85 million tonnes of confectionery products were produced in the first nine months to September 30; this is 2.9% more than last year. The growth rate for this year appears to be 1.5%.

Most chocolate manufacturers and the retail chains prefer to be tight-lipped about the current market trends and their forecasts, so that those who do comment to the industry press have contradictory things to say about the popularity and prospects for the range of chocolate products in the market. The consensus, reported last month, is that slowness in this year’s recovery of demand and sales will be “more than compensated by the growth in demand for such products on the eve of the New Year holidays.”

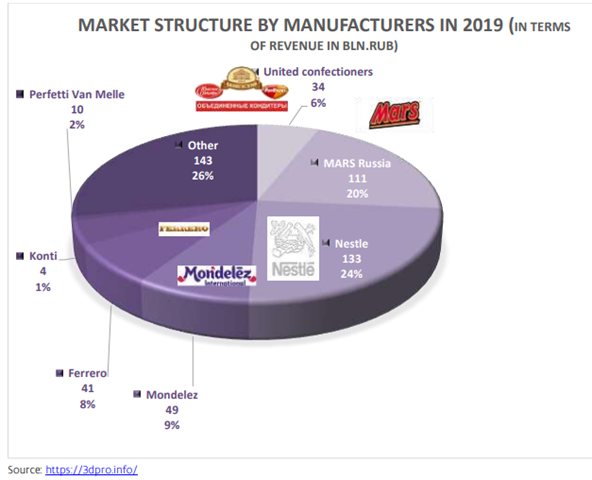

For the leading manufacturers in the Russian market and the most popular brands, the top-10, counted by sale revenues, is unlikely to change significantly. This was how the market shares looked in 2019, based on revenue in billion roubles.

Source: https://www.flandersinvestmentandtrade.com/KEY: United Confectioners groups together Rot Front, Babayevsky, Krasny Oktyabr, and other regional producers. In the global ranking of the largest confectionery companies for 2019, United Confectioners ranks 17th in the world and 1st among Russian companies.

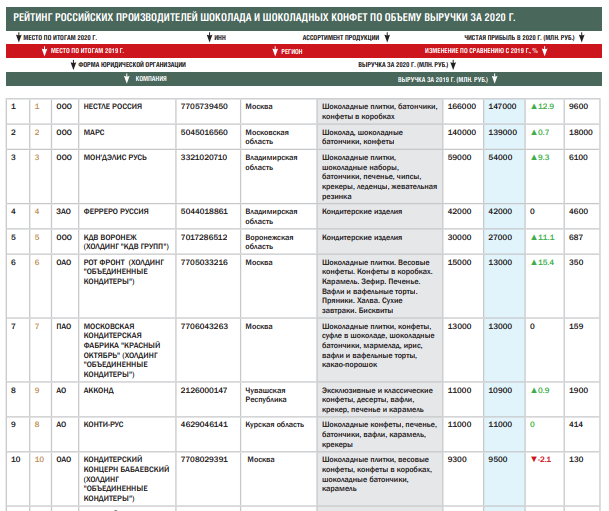

One year later, in 2020, here is the top-10 again. Nestlé, Mars, Mondelez and Ferrero still lead the Russian producers, but the growth rate for Mars has slipped, and Ferrero shows no growth at all last year. The Russian manufacturers, KDV group of Voronezh and Rot Front of Moscow, show the fastest rates of growth, but their sales volumes aren’t enough to challenge the existing market shares of the foreign leaders. Even combining their sales together , the top six Russian leaders fall far short of Mars, and are dwarfed by Nestlé.

Source: http://www.shokolad.biz/ and http://www.shokolad.biz/rynok/

For comparison with a Belgian chocolate industry assessment of the Russian market as of 2019, click to read.

The Belgian forecast, published in April 2020 but before the impact of Covid-19, was for stagnant growth in domestic consumption: “It is expected that in 2020, the market volume will increase to 3.7 mln.tonnes. However, the confectionery market is saturated and every percentage increase can be considered as significant.”

At the same time, the Belgian exporters saw their opportunity in the taste changes of higher-income Russian consumers. “Taking into consideration the trend for healthy lifestyle, there is also an upgrade of the ingredients assortment such as artisanal oils (with oils from various types of nuts, seeds, avocado and argan), sugar substitute syrups, milk alternatives, vegan products, products with a low-sugar content. In this healthy products niche, there is a growing interest for chia seeds and almond milk. According to industry experts, it is expected that within three to five years the turnover of these products will grow at least twice year after year.”

Russian consumers are reported to be tiring of the mass production of chocolates. “They are seeking for new optimal solutions, new taste sensations and new niche products. The manufacturers usually offer such niche confectionery products that can be purchased in their flagship stores, premium network retailers, online stores or directly from the manufacturer via the Internet. This businesses is usually operating in the upper-medium/premium price segments.”

In Moscow this week, the domestic and foreign chocolatiers on the top-10 list were asked to say whether they anticipate significant changes in their market shares, and whether the leading Russian groups are looking to consolidate by takeover or merger. Not one of them agreed to answer.

Leave a Reply