By John Helmer in Moscow

Shares of uranium mining companies, like other energy sources, generally follow the commodity price, so when oil and the others collapsed a year ago, the Russian uranium miner, Priargunsk Chemical and Mining Company (ticker PNGO:RU), went down with them. From a historical peak of $800 per share struck in April of 2007, it drifted down, despite the upward movement of spot uranium prices, to the 2008 peak of $585 on May 22, 2008. Then in July, the share price started diving, and hit bottom of $100 on February 16. How then to explain the 140% takeoff from then to this week’s price of $240?

Part of the answer is that the glow of the share is coming from tiny trades of 300 or less shares. Just 18% of the company’s share issue is potentially open to trading; 82% is closely held by the state-owned uranium mine holding called Atomredmetzoloto; ARMZ for short. The other part of the answer is the upward pull of the Russian stock market (RTS) index as a whole, driven primarily by the rising spot price of crude oil.

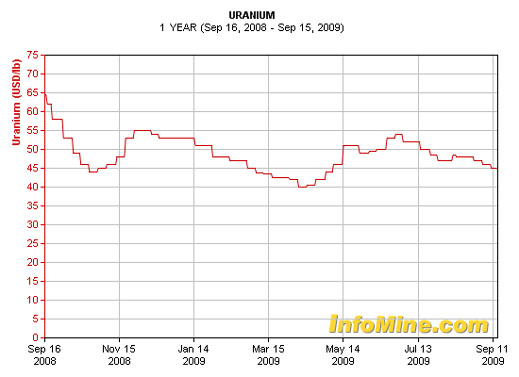

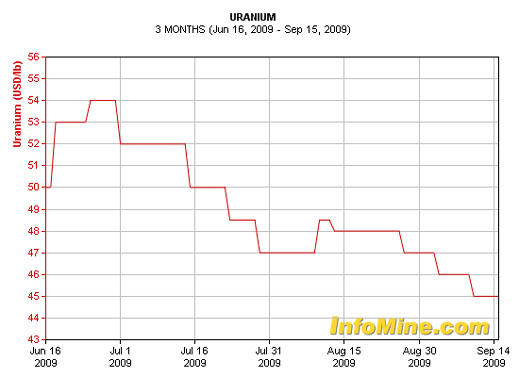

The uranium spot price can be seen pulling the share price down since last year

until April. Uranium’s price then started moving upwards until July. That is when it started downwards again:

According to the Bloomberg charts, just two trades have occurred in the interval for the Priargunsk share – 300 shares in May, 21 shares in September – and these have created the appearance of a gravity-defying gain. A new report by Uralsib Bank in Moscow, issued by Anna Kupriyanova this week, says that the law of gravity isn’t the only one being defied. The PNGO share is way over value, calculated according to her discounted cash flow (DCF) model.

The report indicates that this year Priargunsk should generate sale revenues – entirely to domestic Russian consumers, also controlled by the state – of $250.1 million; this is down 23% on last year. In 2010, the revenue figure is expected to rise by 13% to $282 million. Costs in 2009 will be $224 million, a drop of 30%; next year, they should come in at $253 million. Earnings (Ebitda) this year will be $25.6 million; next year, $29.3 million. The net profit line is in the single digits, according to the Uralsib report: $6 million in 2008; $2 million this year; $7 million in 2010. Net debt is currently at $98 million; enterprise value (EV) estimated at $283 million. The Uralsib report figures that on this basis, PGNO should be worth $84 per share. Accordingly, it is 65% over-priced.

A peer group comparison with the handful of dedicated international uranium miners, whose shares are publicly traded, and calculating the ratio of enterprise value to earnings (EV/Ebitda for 2009), indicates, according to Kupriyanova, that Priargunsk is priced at present at a 77% premium to the average of the others; those counted are Areva of France (CE:FP); Cameco of Canada (CCO:CN); Uranium One (Canada, UUU:CN); and Energy Resources of Australia (ERA:AU). Making the comparison on the basis of the price/earnings ratio for 2009 (P/E), Kupriyanova calculates that Priargunsk is at a 1,035% premium to the others. Uralsib recommends SELLING NOW.

But not so fast — for as a little history will show, the structure for managing and capitalizing the mining of uranium in Russia, and Russian uranium mining ventures abroad, has taken time to become even this clear. And also this large, as Russia has recently moved into the number-3 spot in the world ranking of uranium reserves — number-2 if Russia’s equity stake in Kazakhstan reserves is counted. In the short run, ARMZ is making sure that cash profits can be accumulated quickly offshore, so that, in the medium and longer term, there will be enough to finance one of the biggest unmined uranium deposits in the world in the Russian fareast.

After a confusing spell, in which it was preceded for a year by the Uranium Mining Company (UMC), ARMZ has been authorized to take equity and operational control of Russia’s three operating uranium mines; five planned new mines; and joint ventures in Kazakhstan, Namibia, and Canada. Atomredmetzoloto — literally, “atomic, rare metal and gold” — is a venerable name from the Soviet era of the nuclear industry administration, when it was an enterprise of the atomic energy ministry in Moscow. In those days, it not only supervised uranium mining, but also gold at the well-known Muruntau deposit in Uzbekistan.

Since 1996, ARMZ has been a chartered open joint stock company, in which all shares are owned by the Russian state. It is wholly owned by Atomenergoprom (“Atomic energy industry”), a state holding company, which also owns 100% of Tenex, which enriches uranium fuel and exports it; TVEL, which fabricates uranium fuel; Rosenergoatom, the nuclear utility company and owner of Russia’s reactors; Atomstroiexport, builder of reactors; and other research centres and equipment manufacturers. Rosatom, a state corporation, supervises the entire structure, and is headed by Sergei Kirienko, a former prime minister under Boris Yeltsin, and regional representative under Vladimir Putin.

In briefings for Minesite, ARMZ sources describe the ARMZ stucture as including the Priargunsk, Khiagda, and Dahur mining companies. Altogether, their uranium output was 3,413 tonnes in 2007; that indicates a 7% increase on the 2006 result. If uranium produced in Kazakhstan is added to the total, then ARMZ can claim total production of 3,527 tonnes. The modest difference of 114 tonnes is accounted for the Zarechnoye joint venture. This is one of two Kazakhstan joint ventures in uranium mining, in which ARMZ has been engaged. The Zarechnoye deposit has estimated reserves of 19,048 tonnes, with a production plan calling for output of 2,000 tonnes per year. The joint venture partner is Kazatomprom (“Kazakhstan Atomic Industry”).

Russia produces 8% of the global volume of uranium, and last year ARMZ produced a total of 3,687 tonnes, marking growth of almost 5% year on year. The breakdown for the year was 83% by Priargunsk; 11% by Dalur, 1% by Khiagda, and 5% by Zarechnoye.

The second of ARMZ’s Kazakh JVs is called Akbastau, which plans to mine the Budenovskoye deposit; this has over 25,000 tonnes in estimated reserves, with substantially more suspected. An inter-government agreement between Russia and Kazakhstan allocated half-shares in the venture to the two sides. Kazatomprom holds 50%, while ARMZ holds the other half. The problem for ARMZ is that Kazatomprom expected ARMZ to finance the project – and ARMZ doesn’t have the money. The solution to this problem came out of Uranium One’s misfortune.

In May of this year, the Canada and South Africa-listed junior uranium miner ran into trouble with the Kazakh authorities, who charged officials of the state uranium enterprise Kazatomprom of selling to Uranium One too cheaply, and dealing in assets corruptly. An investigation led to arrests of Kazatomprom executives, and UUU’s shareholders began selling out, crashing the share price by 38% on May 27. A fortnight later, ARMZ came to the rescue, with a deal that mollified Kazatomprom; rescued Uranium One; and gave ARMZ a seat on the Uranium One’s board, representing a stake of 16.6%. As announced, Uranium One purchased ARMZ’s stake in the Karatau uranium mine in Kazakhstan, plus the option to buy ARMZ’s stake in Akbastau, plus any other ARMZ stake in a foreign uranium concession outside Russia. In exchange, ARMZ received 117 million shares in Uranium One, plus $90 million in cash, plus the right to earn a production and tax-related royalty of up to $60 million over the 2010-2012 period. ARMZ also acquired the option to purchase the greater of 50% of Karatau’s annual production, or 20% of Uranium One’s attributable production in Kazakhstan for which it has the marketing rights. ARMZ agreed to cap its shareholding in Uranium One at no more than 19.9% without the prior consent of Uranium One’s majority shareholders. Vadim Zhivov (pictured), the chief executive of ARMZ, took a board seat immediately, with the option to appoint a second director next year.

The transaction neatly circumvented the profit restrictions facing Priargunsk, putting ARMZ in the jump-seat for short-term profit-making by Uranium One; and fund-raising for the more costly, but large-reserve Russian projects in Priargunsk’s and ARMZ’s future. The sources of the growth in ARMZ’s production plan for the next seven years are, in order of magnitude, Khiagda, Akbastau, Zarechnoye, and Dalur. By 2025, however, and supposing the project finance materializes, the big uranium feed for ARMZ will come from the Elkonsky deposit in the fareastern Russian republic of Sakha. With estimated reserves of almost 320,000 tonnes, a mine production plan of 5,000 tonnes per year, and investment of $3.5 billion, Elkon has lifted ARMZ’s aggregate reserves in the newly issued Red Book of the International Atomic Energy Agency (IAEA) to third place in the world, behind Australia and Kazakhstan.

In 2007, before ARMZ took the lead, there was an agreement by Tenex to explore for uranium in Namibia. This remains one of the offshore priorities for ARMZ, company spokesman Dmitry Shulga says, following the establishment of SWA Uranium Mines. That incorporates the joint venture between ARMZ and a Moscow-based diversified investment fund called Arlan. Shulga and Arlan partner, Dmitry Razorenov, told Minesite this week that they are currently exploring the Klein Spitzkoppe deposit, with a target date to start production in 2011. Capital spending on the project is modest at less than $10 million. ARMZ says it is also negotiating for other uranium prospecting ventures in Namibia with Areva. For uranium projects in Mongolia, according to Shulga, there were talks early this month with potential Chinese partners.

Leave a Reply