By John Helmer, Moscow

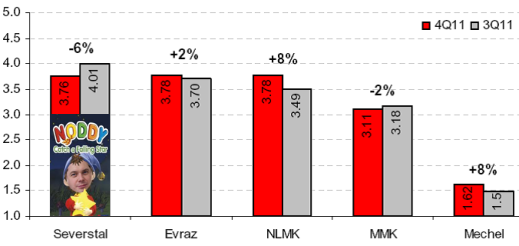

In the final quarter of 2011, Severstal, owned by Alexei Mordashov, lost its footing from the previous quarter as Russia’s leading steelmaker, falling behind Evraz, owned by Roman Abramovich, and Novolipetsk Metallurgical Combine (Vladimir Lisin) in total production of crude steel.

The chart, issued this morning by Alfa Bank steel analyst Barry Ehrlich, reveals what Ehrlich calls “a major negative surprise”. The recent production cutback is bigger at Severstal than for any of the five Russian steel majors.

But there is more to Noddy’s tumble than that. Over the last three months of the year, Severstal suffered a sharper downturn in steel sales from its Russian operations than was registered by the group’s North Americans mills. That has never happened before.

On a full-year basis, counting only crude steel produced in Russian mills, Severstal also appears to have slipped behind Novolipetsk (NLMK), Magnitogorsk (MMK), and Novolipetsk (NLMK).

Its Russian steel mills account for about three-quarters of Severstal’s global output but just over half of its sales volume. For 2011, the trend reported for sales volume was modestly above the levels in 2010, but less in percentage terms than the increase in average product sale prices over the year.

His semi-finished steel sales in Russia during the 4th quarter came to 312,431 tonnes (t), down 9% on the quarter. Russian rolled steel sales dropped 17% to 1.84 million tonnes (mt) in the same interval, including a decline of 15% for hot-rolled strip and plate to 1.08mt; cold-rolled sheet, down 6% to 345,551t; galvanised and metallic coated sheet, down 30% to 177,116t; colour-coated sheet, down 26% to 54,082t; and long products, down 31% to 183,456t. These are the sharpest indicators so far released among the Russian steelmakers of the contraction in domestic demand, despite the latest.

Severstal’s pipemaker, the Izhora Pipe Mill (IPM, Izhstal), has registered a 35% decline in fourth quarter sales of large-diameter pipes (LDP) to 92,481t, while sales of other pipes rose 12% to 187,792t. This was the only gainer in the report for the Russian steel division over the quarter.

What these figures mean is either that Russian manufacturers of cars and refrigerators, oil and gas pipelines, and girders, beams and reinforcement bars for new buildings have lost more of their confidence in Mordashov than they have in his rivals. Or else Mordashov has been cutting his costs of production and his Russian wage bill ahead of the profit squeeze, and preparing to reap more of his reward, relatively speaking, in the US. Manoeuvres like this are precisely what the Kremlin has been anticipating when it moved last week to prevent the steelmakers from disinvesting in Russia and moving their capital to offshore operations.

During the fourth quarter, the North American steel division, with mills in Michigan and Mississippi, recorded a 5% decline in sales of rolled products (aggregate, 1.02mt), with an 11% decline in hot-rolled strip and plate to a total of 596,523t. Compensating on the upside, sales of cold-rolled sheet grew 8% quarter on quarter to reach 131,302t, and sales of galvanised and metallic coated sheet gained 2% to finish at 295,113t.

The full-year trend shows a static to declining picture, with group-wide hot metal production at 10.54 million tonnes, up just 1% on the 2010 level. Production of hot metal at the Russian steel division finished the year at 8.82mt, also up by 1%. The North American division output was down 4% at 1.73mt. Crude steel output for all divisions was 15.29mt, up 4% on the year before. The crude steel total for Russia was up just 2% at 11.36mt, while for North America the crude steel total gained 8% to end the year at 3.94mt.

A comparison of Severstal steel sales between 2010 and 2011 shows that in Russia sales of semi-finished steel products totaled 1.29mt, a decline of 8%. Hot-rolled sales gained 2% to 7.66mt, but this included a 9% year on year downturn in cold-rolled sheet sales to 1.4mt, and a 1% drop in colour-coated steel sales to 240,589t. The year-end results for Severstal North America are mixed. The volume of hot-rolled.strip and plate sold came to 2.06mt, representing annual growth of 15%, and sales of galvanised sheet gained 9% to 1.23mt. However, sales of cold-rolled sheet fell by 20% to 519,835t.

In a company announcement a week earlier, Severstal reported that its specialist Russian pipemill, IPM, had set a full-year record for production of over 500,000t of LDP. According to Nikolai Skorokhvatov, IPM’s chief executive, “2011 saw the plant operating at full capacity and, despite a declining market for large-diameter pipes at the end of the year, the Izhora Pipe Mill continued to produce and ship tubular products to our key clients.” But the good news is being rapidly overtaken by the lack of new pipeline projects from Gazprom and Transneft to keep the furnaces alight at Izhora.

Severstal’s mining division reports that its two coal-mining divisions at Vorkutaugol in Russia and PBS Coals in the US, suffered declines in coking coal concentrate prices in the final quarter of 20% ($167/t) and 11% ($162/t), respectively. Over the full year, the price of coking coal concentrate rose 35% and 36%, respectively. Sales volume for coking coal concentrate, including both Russian and US mines, fell 5% in the 4th quarter to 1.88mt, but gained 5% for the year to 7.59mt.

In the iron-ore segment, pellet sales for the group came to 2.62mt in the 4th quarter, down 9% from the third quarter; for the year, pellet sales totaled 10.05mt, up 3% on 2010. Iron-ore concentrate sales were 1.22mt in the final quarter, down 3%, while for the year, they came to 4.76mt, up 18%.

The company added no commentary to the results announcement, and has yet to provide new forecasts for this year. In early December, when Severstal reported financial results for the third quarter, management expressed optimism, anticipating “some positive signs of recovery in Q1 2012 related to restocking, stabilizing raw material prices and start of the construction season in Asia.”

That is drawing an unusual degree of scepticism. According to the usually ebullient steel analyst at Renaissance Capital, Boris Krasnojenov, “we believe disappointing 4Q11/1Q12 results may be a common theme for all Russian steel majors.” According to Ehrlich, “although Severstal claims it has successfully sold the volumes into 1Q12, we have no grounds to confirm or deny this statement.”

Leave a Reply