By John Helmer in Moscow

President Dmitry Medvedev is lying when he claims that his modernization slogan, under which he is running for re-appointment by Prime Minister Vladimir Putin, means free and fair competition; security for foreign investment; and private ownership in place of state control. I mean lying, as in lying on the fakir’s bed of nails. Medvedev knows that this location is a sensitive one. If he moves unpredictably, he risks Putin’s wrath, and the pain of many other pricks.

What Medvedev is doing is to make the Kremlin program of oligarch debt bailouts, monopolization of economic resources, concentration of state control, and eventual reprivatization to the same favoured elite, which has already benefited from Putin’s patronage, appear to be two adjectives Medvedev enjoys using – legal and modern.

Stanislav Belkovsky, whose National Strategy Institute in Moscow has served a variety of Kremlin and oligarch masters over the years, warned last week that noone should be fooled: “Medvedev is Putin today. According to the logic of the system, he must bring Putin’s cause (more precisely, that of the late Yeltsin and Co.) to its logical conclusion. To preserve principally unchanged all the centers and mechanisms of viability of the system, having somewhat adorned its crumbling false facade.”

Not so quick on the draw, Stan. Let’s ask what Medvedev is doing in bed, so to speak, with the Renova holding of Victor Vekselberg and Basic Element, the hoilding of Oleg Deripaska, who also controls the Russian aluminium monopoly, United Company Rusal; Vekselberg is also chairman of Rusal’s board.

| Medvedev’s spokesman won’t say if these two oligarchs are accompanying Medvedev on his US tour this week, which commenced with two days at Silicon Valley in California. But Vekselberg is there, signing an agreement to help cover the annual $1 million cost of preserving the Russian theme around Fort Ross Park, in the north of the state. |  |

Medvedev has already designated the two oligarchs his harbingers of modernity – Vekselberg at the Kremlin’s proposed version of Silicon Valley outside Moscow; and Deripaska in charge of the Russian aluminium and car industries.

Vekselberg was at the meeting Medvedev chaired of his Presidential Commission for Modernisation on June 19, when the President announced that he had seen “all sorts of miracles”. One of them may have been Deripaska’s application to the commission for Rb1.4 billion ($45 million) – the biggest grant so far sought by a Russian company – to pay for research into new technologies for the manufacture of aluminium. “After their introduction in manufacture,” Rusal is claiming, “Russia’s aluminium industry will become the unconditional world leader for many years ahead.”

Among the foreign members of the commission whom Vekselberg proposed, and Medvedev accepted for the commission, there is Eric Schmidt, chief executive of Google. Under intensifying pressure to restrict the ownership and the content of the Russian internet to a handful of Russian oligarchs, Google is struggling. No surprise that Schmidt hopes US business lobbying of Medvedev will improve Google’s competitive position in Russia; or as he told the New York Times, “help pressure the incumbents who fear change and will also clearly benefit the citizens overall.”

Vekselberg and Deripaska also deserve to be examined as potential partners in modernity for US businesses, because among the Russian oligarchs, they stand alone in the federal US courts charged with asset stealing, racketeering, and fraud. Vekselberg has been fortunate so far – US judges are still deciding at the appellate level whether they will take jurisdiction over the claims against him, which involve oilfield assets.

Vekselberg is also facing criminal prosecution in Switzerland, after the Swiss Federal Finance Department and the government market regulator, the Financial Market Supervisory Authority (FINMA), have separately ruled that he is culpable in cases of shareholder and market fraud in his takeover of two high-technology Swiss companies, Oerlikon and Sulzer. He and Renova have professed their innocence, intimating they have been framed by Swiss competitors and disgruntled former employees. “Renova Group,” it has declared, “denies these unproven allegations and asserts that it has always meticulously upheld all legal rules within the area of its responsibility and influence, including disclosure laws.”

Medvedev lobbied in Switzerland last year to clear Vekselberg, but didn’t succeed. He will try again when the Swiss President, Doris Leuthard, comes to Moscow in August. If the Swiss give up pressing Vekselberg for fines or prison, he might arrange lucrative imports of Swiss-made goods for the Russian high-tech sector, he has hinted in the press.

In the US, Deripaska has been the more carefully scrutinized of the two, and the outcome for him hasn’t been positive. In a briefing for the US Senate Committee on Intelligence early this year, the then Director of National Intelligence, Admiral Dennis Blair, intimated that Deripaska’s control of the Russian aluminium monopoly threatens US economic security. “An increasing risk from Russian organized crime,” Blair said, “is that criminals and criminally linked oligarchs will enhance the ability of state or state-allied actors to undermine competition in gas, oil, aluminum, and precious metals markets.”

Deripaska has reported to investors that US Government action to deny him an entry visa on the ground of “alleged connections to organised crime” is “unwarranted and unsupported”. He has added – in the Rusal investment prospectus of December 31, 2009 – “to the best of his knowledge, he is not under investigation by any U.S. authority.”

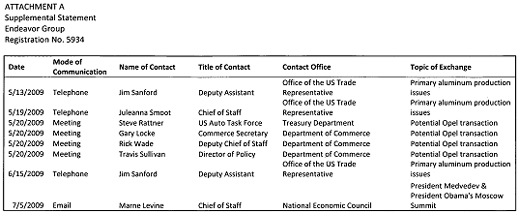

Deripaska lobbied hard last year to persuade US Government officials, New York investment banks, and General Motors (GM) to agree to sell GM’s Opel auto division to Deripaska’s GAZ group, his heavily indebted Russian automotive holding. US Government records show that Deripaska was paying a Washington lobby firm, Endeavour, more than $45,000 per month to arrange his permit to cross the US border, and win the Opel sale. The records also show that, although Deripaska was the client in Moscow, he paid Endeavour from a company called Taviner Ltd., with an address belonging to Arias Fabrega & Fabrega in Tortola, British Virgin Islands. The law firm, which originates in Panama, says it specializes in offshore services.

The money was spent on meetings with US officials, as detailed in this report on file at the US Department of Justice

But the lobbying failed. The US voted its shares, along with others, to persuade GM to reverse an earlier approval of the Opel sale, and cancel Deripaska’s deal.

Deripaska has largely avoided the jurisdiction of the US courts, although not entirely. One claim against him – of fraud, bribery, and rigging the privatization of the Aluminium Smelter Company of Nigeria (Alscon) – commenced in the US courts at the request of one of the bidders for Alscon, the California-based Bancorp Financial Investment Group. The case has been moved from the US to the Nigerian courts, on condition Rusal accepts the latter’s jurisdiction and ruling. That case is also still pending without a ruling.

The evidence on Deripaska’s business practices has also surfaced in the UK High Court case by Deripaska’s original business partner, Michael Cherney, who is suing for contract fraud; in a separate Swiss federal court ruling in Cherney’s favour; and in an ongoing Spanish court investigation of money-laundering.

Like Vekselberg, Deripaska has a more sympathetic ear in Medvedev. After Deripaska and his companies plummeted into $21 billion worth of insolvency at the end of 2008, he asked Medvedev to swing his weight behind a scheme to exchange the Rusal debts to the state banks with special non-voting, non-dividend shares Deripaska proposed that Medvedev order them to buy. The scheme was not approved by others in government, and Medvedev didn’t declare his support for it.

But he did make public statements to protect Deripaska from his creditors, endorsing thereby the schemes by which Rusal, GAZ, and other Deripaska companies have evaded scores of payment awards and debt rulings against them in the Russian Arbitrazh Court system.

| “I fully agree with what Oleg Vladimirovich [Deripaska] said about situations when the crisis leads to settling scores,” Medvedev announced in February of 2009. “There should be no situations when different structures’ rivalry can lead to the collapse of an entire group of companies…Such actions should get adequate reaction from the state. For that purpose we have one serious institution, the government of the Russian Federation … There are situations when power must be used.” |  |

Early this month, Medvedev agreed to participate in a scheme in which Deripaska would bring the acting ruler of the west African republic of Guinea, General Sekouba Konate, to the Kremlin for a hand-shake over an agreement Konate was prepared to sign, granting Rusal controversial bauxite mining concessions in that country. The scheme was illegal under Guinean law, and Konate backed down at the last minute. The Medvedev hand-shake was called off.

Lilia Shevtsova, an analyst at the Carnegie Endowment’s Moscow branch was referring to another organ, when on the eve of Medvedev’s arrival in San Francisco, she said his purpose isn’t what US investors are being encouraged to think. “Western capital helps to support the status quo. It injects financial and technological Viagra to the existing system,” Shevtsova, a partisan of former President Yeltsin, said. “Western capital could become an engine of modernization only under new rules of the game — that is, when Russia moves toward real competition and rule of law.”

Now Vekselberg and Deripaska are preparing a much bigger test for Medvedev: this is perhaps the biggest test of Kremlin favour since his term began two years ago. The outcome may determine whether Medvedev goes down as the champion of corporate transparency and law reform, or the purveyor of private favour. This test is whether Medvedev will back a hostile takeover of Norilsk Nickel, Russia’s largest mining enterprise, by Rusal.

The first signal of the takeover plan was in October 2007, when Deripaska arranged to buy a 25% stake in Norilsk Nickel from its owner Mikhail Prokhorov, who had fallen out with his co-shareholding partner, Vladimir Potanin. Potanin continued to control Norilsk Nickel, while Rusal announced it had taken “a first logical step towards a possible full consolidation of Norilsk.”

Potanin fought back, taking his case against Rusal’s takeover to Prime Minister Putin and the Deputy Prime Minister in charge of resources, Igor Sechin. They decided against Deripaska, and he was called into Sechin’s office, along with Potanin, in July of 2008. Sechin said the government would not countenance or allow Rusal to take over Norilsk Nickel.

The Russian bust then followed. Putin, who also chairs the state bailout bank VEB, decided to keep Deripaska afloat, adding to $4.5 billion in state loan support, the underwriting of Rusal’s share listing on the Hong Kong Stock Exchange on January 27 of this year. A week later, Deripaska announced he was on the warpath again with Norilsk Nickel. On February 4, 2010, through Prokhorov’s deputy, Dmitry Razumov, the takeover strategy was publicly revived: “Now that Rusal has liquid shares,” he announced , “I see no obstacles for a restart of the dialogue between the shareholders on the merger of Rusal and Norilsk Nickel. We believe that in the long run Norilsk and Rusal combined will be able to compete more successfully on the international level than separately. Sooner or later the enlargement will become a necessity, or else you won’t be able to compete with big international players.”

A few days later, Prokhorov reiterated the takeover challenge. “We want to create a Russian BHP Billiton. A merger between Norilsk Nickel and Rusal is good not only for shareholders, but for all the country. But it’s a shareholder question, a question for all the shareholders, not only majority shareholders.”

Potanin controls about 33% of Norilsk Nickel. The free float held mostly by US and international institutions amounts to almost 30%. Through loans to Potanin and security pledges of Norilsk Nickel stock, the state banks and the government hold a 4% stake, with influence over another 10% of the shares.

Potanin and the international shareholders are opposed to the Rusal takeover. Last month, and again this month, they blocked attempts by Deripaska to take more cash out of Norilsk Nickel in dividends than the company earned in profit last year.

The Russian government appeared also to be behind Vladimir Strzhalkovsky, Norilsk Nickel’s chief executive, a former KGB operative and government official before he was appointed to his corporate role, who has publicly accused Rusal of trying to strip Norilsk Nickel of cash to solve its own problems. “We have an ebitda margin [earnings before interest, tax, depreciation and amortisation] of 43 per cent while Rusal has less than 16 per cent – and this is only when they have tolling [a transfer pricing system that provides tax breaks on raw materials supplies] and special tariffs for electrical energy and transportation. What if all this was brought to a normal situation? What would be the sense of such a merger? I understand that often in business the processes of mergers and acquisitions give a certain boost to the initiator of the process but I don’t see any need for their bid for success to lead to a loss for normal shareholders.”

Even the international banks, which were advisors and book-runners in the Rusal listing in Hong Kong, and are currently holding Rusal shares or share warrants, acknowledge that the improved net profit figure reported by Rusal for 2009 results from booking a debt refinancing and deferment as interest income of $1.2 billion; and from counting Rusal’s 25% stake in Norilsk Nickel’s 2009 profit of $1.265 billion as added asset income.

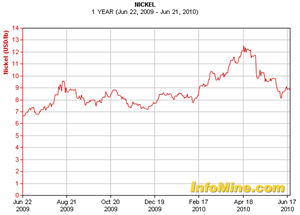

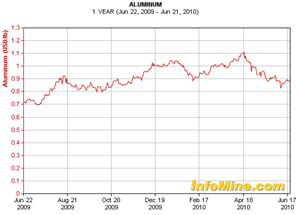

Investment fund managers in Hong Kong and London believe the need on Deripaska’s part for a takeover of Norilsk Nickel is driven by the failure of Rusal’s Hong Kong Stock Exchange listing to generate sustained market confidence, or the share value promoted by its bankers, brokers, and advisors. The course of the Rusal share price over the past five months indicates repeated failure by the supporting institutions to boost Rusal’s share price to targets above the listing fix of HK$10.80 (US$1.39). Worse, Rusal’s share price has been sinking, while the price of aluminium metal has been rising, along with the shares of US and Chinese-listed rivals, Alcoa and Chalco, and the value of other large companies on the Hong Kong Exchange.

The private consensus of the London and Asian investment institutions is that Rusal is uniquely risky, and subject to unusual discounting of its share value in relation to its peers. Even Rusal promoters like CLSA, the leading Asian brokerage, reports that Rusal’s corporate governance score puts it at the bottom of the table of sector companies assessed. “According to the CLSA report of March 2010, “the company [Rusal] scores poorly in areas of discipline, fairness and responsibility due to several factors, including material-related party transactions (Rusal’s largest shareholder and CEO is the controlling shareholder of two plants that supply power to Rusal), the controlling shareholders’s stake of over 40%, the necessity for debt restructuring, and the large size of the board (18 members).”

| In the international market, therefore, there is no pricing support for the merger with Norilsk Nickel or hostile takeover. So Deripaska must once again apply to the Kremlin to support the takeover by administrative influence. One of the arguments in favour is that Rusal’s value to the state can only be salvaged if it diversifies its asset base away from aluminium, and re-rates the weak Rusal share in terms of the stronger Norilsk Nickel share. |  |

| Another of the arguments is that if the global aluminium price continues to decline, and the rouble depreciates, there is a growing danger that Rusal’s financial position may worsen to the point of default again. |  |

Ahead of the annual general shareholders’ meeting for Norilsk Nickel, scheduled in Moscow on June 28, the company’s shareholders have been saying that Deripaska is toxic, Rusal is viral for the share price of Norilsk Nickel.

They claim that Deripaska rarely acquires assets without ‘administrative resources’ at the regional, and also the federal level. That is a Russian phrase implying political influence. US and UK court papers filed against Deripaska’s takeovers have not reversed Deripaska’s acquisitions, but court action has induced him to settle out of court, with compensation for former proprietors.

At the current market capitalization of Norilsk Nickel at $31 billion, an attempt at a market-based purchase of a 25% shareholding to make the controlling stake would cost Rusal not less than $7.8 billion; the control premium is likely to increase this price over $8 billion. Neither Rusal nor Deripaska can afford such a price. Nor can Prokhorov, although his cash assets are substantial.

The most likely source of the money would therefore be the same Russian state banks which backed Deripaska for his Hong Kong listing – VEB chaired by Putin, and Sberbank, headed by German Gref – with other state or state-controlled banks, such as the VTB group and Gazprombank ready for additional funding, if required. The current market cap of Rusal is $13.6 billion, less than its indebtedness, and less than half of Norilsk Nickel’s value. Although the Rusal buyers would no doubt wish to reduce their cash offer, and increase the paper swap, it is unlikely that Norilsk Nickel shareholders would find Rusal paper acceptable even on better than a 2 to 1 ratio. State money is the only way to sustain the takeover bid Rusal says it wants.

Therefore, the likely scenario for Deripaska – quite possibly his only option — is to attempt to compel Norilsk Nickel to accept a Kremlin diktat. That is where Medvedev’s program of legal reform and modernization comes in. That, too, is the bed of nails on which the President of Russia is presently lying.

Leave a Reply