By John Helmer in Moscow

Sacre-Coeur Minerals (SCM) is a small Toronto-listed goldminer prospecting the malarial swamps of Guyana (South America), so far without striking El Dorado.

The company is so small, its website doesn’t publish financial reports. But the required filings with the stock exchange indicate that it is producing no gold; its operating expenses exceed its income; it paid out more in compensation last year to its Canada-based employees and consultants than to its Guyana prospecting organization; and it has obligations to share, warrant and options holders amounting to C$40.8 million.

Asset value in Guyana comprises C$3.8 million worth of costs in acquiring exploration rights from Alfro Alphonso and other locals, plus C$30 million in exploration costs expended to date.

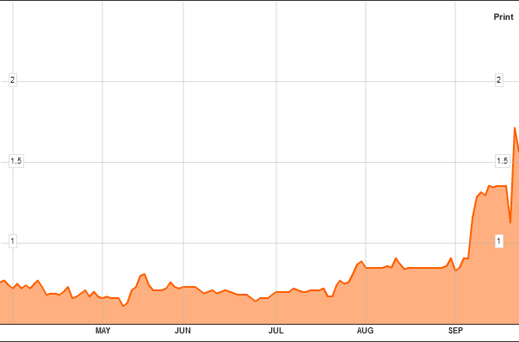

This week SCM announced it has struck gold in Moscow. This is an agreement with one of Russia’s most famous over-spenders, Alexei Mordashov. The deal is for SCM to sell all its shares to him and become a wholly owned subsidiary of his Severstal Gold company. The price Mordashov paid of C$1.60 per share represents a premium of 88% over the average of SCN’s share price for the twenty days preceding the start of the sale negotiations on September 8. Because Mordashov had already bought a small stake in SCM without disclosing it, his buyout of approximately 93% of the shares will cost him about C$60 million.

| SCM reports that its assets comprise 388,458 troy ounces of measured gold under the ground, and another 62,940 oz of indicated gold. These numbers were reported in September 2008. Since then it isn’t clear why SCM’s programme of drilling, sampling and assa ying has turned up no news for two years. But perhaps it has, if you can wait for a few seconds to find out. |

|

The seller in the transaction is Irwin A. Olian. Between collecting degrees from Princeton and Harvard and looking for gold in Guyana, he has had a career in the Los Angeles movie business, selling cures for cancer, lawyering, and broking shares, before he started out in mineral search with African Queens Mines. This is not one of Olian’s movies; it’s a junior miner, also listed in Canada, with prospects in Africa. One of the prospects is the King Solomon Project in Mozambique. Olian has taste.

Mordashov has an addiction — paying too much for assets. His promoter in London, Peter Marsh, explains this as healthy ambition rather than clinical profligacy. “I’m still committed to globalisation,” Marsh recently quoted Mordashov as saying. “However, it has to be the right [globalisation] strategy, not just any globalisation strategy.” Marsh and Mordashov omit to say that Mordashov’s strategy as a global steelmaker ran up debts of almost $8 billion between 2002 and the crash of autumn of 2008.

To make sure he would repay and try to give him a cure for his addiction, Mordashov’s bankers put him in a strait jacket of strict repayment, earnings, divestment and asset purchase conditions.

Mordashov has told his bankers that if they will be a little patient, they can assist him to amass a portfolio of gold assets and then resell them in an initial public offering on the London Stock Exchange. The golden vehicle is named Severstal Gold. The listing is being managed by Morgan Stanley and Credit Suisse. JP Morgan, which was reportedly in the syndicate several months ago, has dropped out. The first promo for the London listing was released in the Financial Times on Tuesday, according to “several people close to the company” who don’t yet want to be named. Several more people close to Mordashov’s heart and pocket were reported as saying the valuation of the new company “was likely to hit $4bn or possibly $5bn as details about the assets and the company’s growth plans were disclosed to the market.”

That’s a hefty hype already. An experienced Russian precious metals analyst, Vladimir Zhukov of Nomura, reported on September 16 that he values Severstal Gold at US$18.70 per share. That makes a market capitalization estimate of between US$3 billion and $3.6 billion. Zhukov explains that he has raised this number because Mordashov had taken over the Guinean goldmine reserves and production of Crew Gold earlier this month. “Following the acquisition of Crew Gold as well as the disclosure of more details on Severstal Gold, we have raised our valuation of Severstal Gold from $2.2bn-2.6bn to $3.0bn-3.6bn.” Zhukov didn’t know that Mordashov was also taking over Sacre-Coeur.

| But if Mordashov figured SCM to be worth paying 88% over the market price, he can’t believe this is an empty hole in the jungle. So what is its value in the Severstal Gold IPO? |  |

For all of last year, Mordashov attempted to buy out the minority shareholders of another Canadian goldminer, this one producing – High River Gold (HRG). The full story of that abortive effort can be read here. Led by a handful of determined internet bloggers, the Canadians resisted a series of low-ball price offers and more unpleasant pressure tactics to sell out. The outcome is that Mordashov has been unable to accumulate more than 70% of HRG, and the minorities retain their shares for the revival of value they are confident will come at or after the Severstal Gold listing in London.

The year-long battle over share price leaves the Canadians convinced Mordashov would never pay a premium for an acquisition if he can help it. But the record of his purchasing of the Arlan and Celtic Resources goldmines in Russia; the sale and repurchase of HRG shares from Troika Dialog; the takeover of Crew Gold; and now the acquisition of SCM suggest that premiums and putting huge profits in other people’s pockets make a habit Mordashov can’t break.

Market sources believe there may be a more reasonable, entrepreneurial calculation for paying over the top for SCM, even as the market reassesses downward what Sacre-Coeur is really worth:

According to the calculation of a major Canadian investment figure, “I believe the Severstal group paid $200M for their HRG interests and then $500M for Crew. Add it all up, and it comes to $1.2B. If the IPO is worth $4B and Mordashov sells 30% to pocket $1.2B or more, he gets all his money back. And he still owns 65% to 75% of the business. In other words, the longer term gain is about $2.8B.”

Russian oligarchs count forward investment returns on their thumbs, not on their fingers. So Mordashov isn’t likely to be projecting beyond 2013. And that indeed is the year, according to the Severstal Gold corporate presentation now on the company website, when he is promising the market that his venture will reach gold production of 1 million oz per annum. That’s two years away, and he’s currently about 350,000 oz short of target.

This was factored in when Nomura issued its report last week on the gold resource and production levels which buyers of Severstal Gold should be anticipating: “ Severstal Gold segment holds 12.5moz of gold in measured and indicated resources, most of which are contained in the West Africa (8.4moz), followed by Russia (3.3moz) and Kazakhstan (0.8moz). Severstal Gold produced 529koz of gold in 2009. The management is guiding for 640-670koz output in 2010E (including Crew Gold since August 2010), of which 63% would come from CIS and 34% from West Africa. In 2011, we expect Severstal Gold to produce over 700 koz. Severstal management targets production of over 1.0moz of gold by 2013E.”

But SCM isn’t producing anything yet, and its resource is just 451,937 oz. That was two years ago. What if Olian and his crew found more gold reserves than he has reported so far? What if prospect no. 9, tested in June of this year, turns out to be as rich as this brief mention in one of SCM’s presentations: “Million Mountain – Zone 9 Area 2.20 sq km; target structurally controlled, Au bearing, mesothermal vein systems hosted in metasediments. Many veins have surface expression and are well mineralized with sulphides and gold. A 1 meter chip sample from a vein outcrop returned 45 g/t Au. Initial scout drilling intersected 13.6 meters @ 4.0 g/t Au, including 0.55 meters @ 84.26 g/t Au (KM0209). Ground geophysics surveys now underway. (June 13, 2010).” (Emphasis in the original.) Look again at those grades – 45 grams to 84 grams per tonne. That’s geologist lingo for big share price.

Naturally, there is no telling what’s really there in Zone 9, and stock exchanges in most places have rules about getting potential sharebuyers too excitable about facts that aren’t tested or proven. Possibly Mordashov leapt out of his strait-jacket this month; possibly he thinks he knows already that SCM is worth more than the premium he paid if it can add big-number reserves to Severstal Gold’s portfolio, and big-number production to its operating target.

The Canadian investment analyst again; “the bigger the production and reserves are, the higher the IPO valuation. Therefore, Mordashov is trying to build the value as quickly as possible. In other words, although Severstal paid $500M for Crew, in the IPO it is worth a multiple of that. I suspect the aim of the South American [SCM] acquisition is to add reserves. Perhaps they have seen reports that show much more reserve potential. Or Mordashov could just be trying to present to the market that he has a global gold company now. Once they reach 1M oz production, supposedly the multiples jump even higher in terms of stock market valuation.”

Stock markets have regulations against reckless misrepresentation and fraud – there’s no suggestion of any of that in this story. In the markets for goldminers, there’s no law against the magic multiplier.

A London investment banker specializing in mine floats warns against dreaming. “They are smoking the kind of stuff that makes them believe that in this gold market they can float anything, anywhere, and that the clamor for their gold IPO issue will be so immense that bulking up with tiddlywinks will add value. Celtic and Arlan are very mediocre assets. Endeavour made over $80mn from them front-running Crew Gold, so the drinks are on them.”

“Severstal believes that the market will indeed ignore sum of parts. They really need to consolidate HRG, but the minorities there are not going to give in so easily after Mordashov tried to shaft them a couple of times. Can’t do that so easily in Canada.”

Leave a Reply