By John Helmer in Moscow

The first major Russian corporation to attempt to issue shares on the London Stock Exchange since the 2008 crisis has now failed, after the UK Financial Services Authority (FSA) opened an investigation into Dmitry Mazepin’s fertilizer holding Uralchem.

Undisclosed shareholders; a mysterious $200 million share transaction involving insiders; and inadequate financial disclosure by the company and its auditor, are among the problems newly revealed to the FSA in a 59-page complaint lodged by the Brown Rudnick law firm on April 26.

This is the second time an investigation by the FSA has put a stop to a Russian initial public share offering (IPO). The first was in mid-2007, when United Company Rusal, controlled by Oleg Deripaska, withdrew its IPO, claiming that timing and market conditions were unfavourable. A Spanish criminal court order — issued a year ago in Madrid, but recently come to light — has revealed that during Rusal’s attempted IPO, the FSA produced a report on Deripaska, which has been kept confidential until now.

Rusal went to issue a 10% bloc of shares three months ago on the Hong Kong Stock Exchange, after the Hong Kong regulator decided to waive or suspend the applicable regulations.

Uralchem’s withdrawal, acknowledged this morning, will have reverberations throughout the Russian and international stock markets, as other Russian companies and their shareholders prepare fresh bids of their own for foreign shareholder trust. Not least of all, the investment banks which have signed their names to prospectuses later discovered to be less than credible, may be face censure for misleading investors. Goldman Sachs, under investigation for fraud in the US, had been an advisor to Rusal before its London listing attempt was abandoned; Goldman Sachs reportedly withdrew from the subsequent Hong Kong listing attempt.

Morgan Stanley was one of several of the banks responsible for Uralchem’s IPO bid and the prospectus that was issued on April 19; Morgan Stanley was also an advisor to the Rusal IPO attempt in London in 2007. There is speculation that after the Uralchem disclosures were lodged with the FSA, Morgan Stanley may have been one of the banks urging Uralchem to withdraw. Graeme Russell, head of compliance at Morgan Stanley in London, and Jim McKeague, another Morgan Stanley executive, have been identified as addressees of the text of the FSA complaint, as they may have been involved in reading the prospectus before issue, and in considering the issues that have become the focus of the subsequent FSA complaint and investigation.

The other banks engaged on Uralchem’s behalf were UBS, Unicredit, Sberbank and Renaissance Capital. The auditor vouching for the accuracy of all the financial presentations is Deloitte Touche.

Renaissance Capital is currently under investigation in the US for sanctions busting in Zimbabwe, as part of a broader US Treasury investigation of Mikhail Prokhorov’s business practices; Prokhorov owns 50% of Renaissance Capital after Stephen Jennings, the controlling shareholder of Rencap, was unable to repay Prokhorov on a $500 million loan during the 2008 crisis. Rencap was one of the promoters of the Rusal listing in Hong Kong;it is attempting to open an office in Hong Kong.

Sberbank, the state savings bank, is one of the guarantors of Rusal’s solvency and one of the bookrunners of the Rusal listing in Hong Kong. This week it has been targeted in the FSA investigation in London on charges of conflict of interest. At issue for the FSA is whether Sberbank, as a major lender to Uralchem, and also an agent for Uralchem’s attempted share sale to London investors, has failed to “undertake due and careful enquiry”, as the FSA complaint document charges; and whether the “potential conflicts” recommend disapproval by the FSA of the Uralchem prospectus on the ground that the information contained may be “misleading, false, or deceptive.”

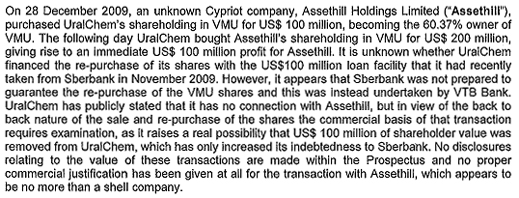

The torpedo for Mazepin’s share sale was launched by a company called Shades of Cyprus, which is connected to Uralchem’s bigger Russian rival in the phosphates business, Phosagro. The submission to the FSA was prepared by lawyers at the request of Shades, which has been in long-running Moscow litigation to recover the equivalent of $106 million from Uralchem for a 24% stake in one of Uralchem’s fertilizer production units, Voskresensk Mineral Fertilizers (VMF is the Englouish acronym, VMU the Russian acronym). Sberbank is the current target of the Moscow court case because it was the guarantor of Uralchem’s payout for minority shares tendered in a mandatory buyback process in mid-2008, after Mazepin acquired 70% of VMF.

The FSA filing claims that the attempts by Uralchem to block this payment for the shares were illegal. The Uralchem prospectus acknowledges the pending court case; denies liability; and tells investors that if the courts end up ruling in favour of the Shades claim, it can draw on a fresh credit line from Sberbank to pay. Nonetheless, the prospectus concedes that “any such payment would have a material adverse effect on our financial position.”

An apparently new disclosure in the FAS submission intimates that there was insider dealing over VMF shares last December. Here is what the document alleges:

Uralchem was asked to say what relationship there is (or was) between Uralchem shareholders and Assethill Holdings, and why the December transaction was undertaken. The spokesman Olga Astrova promised to respond but has failed to do that during the working day.

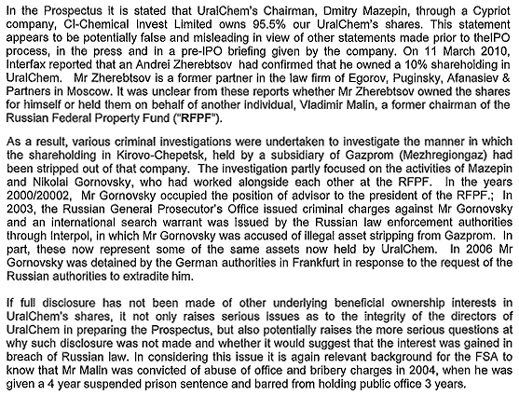

The FSA has also been asked to investigate the accuracy of shareholder disclosures in the prospectus. Identifying all beneficial shareholders in Russian companies is a well-known problem, especially when the publicly identified shareholders are bound by secret trustee agreements or contracts with silent partners, through which the latter are de facto stakeholders – and in some cases, controlling ones. When Russian steelmaker Evraz issued its London IPO in 2005, underwritten at the time by Morgan Stanley, public disclosures revealed there were trustee shareholding arrangements which Alexander Abramov, the seeming control shareholder, had not admitted.

The best known of the trustee arrangements behind a Russian shareholder has been revealed in the UK High Court lawsuit of Mikhail Chernoy (Michael Cherney), who was the founder of Rusal’s predecessor company, and put Deripaska in business. According to the text of a March 2001 contract signed by Deripaska – ruled genuine by High Court Justice Christopher Clarke – Deripaska’s current and purported 59% shareholding in Rusal includes the equivalent of a 13% stake owned by Cherney. The court will open proceedings in May on the contract enforcement suit, worth at Rusal’s current market capitalization of $16.2 billion about $2.1 billion. Entitlement to dividends and shares of asset sales, to which Deripaska has already helped himself, add more than another $2 billion to the potential Deripaska liability to Cherney. The London court has already ruled that Cherney’s claim has a “reasonable prospect of success”.

Mazepin’s problem is similar to Deripaska’s, but trial of the evidence appears to have arrived more swiftly. The FSA submission alleges:

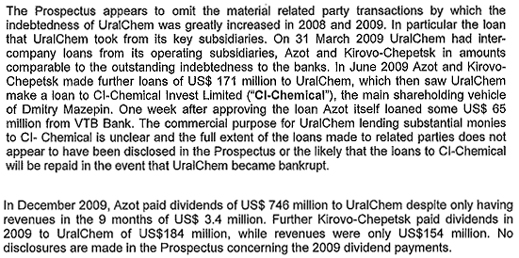

The claim document by Brown Rudnick for Shades charges that the prospectus which was drawn up by Morgan Stanley and the other banks, and vouched for by international accountants and lawfirms, was materially misleading on several financial counts. The allegations suggest that Uralchem’s heavy debts and operating losses have caused bank loan covenant breaches and waivers that “should be disclosed in full”. Uralchem and its auditor are charged with failing to fully disclose and account for working capital deficits and asset and transaction miscalculations.

Two accounting mysteries are identified from the financial statements of the prospectus, one from which Mazepin appears to have benefited, and one which appears to have caused financial loss for Uralchem subsidiaries:

It is not unheard of for Russian corporate and oligarch rivalry to spill into the London market with press campaigns and calls for investigation by the regulator. The policy of FSA officials is not to comment on investigations that are under way, or disposed of without public rulings. Once a proposed share sale and its accompanying application for approval of prospectus are withdrawn, the FSA remains silent. That was the case with the behind-the-scenes investigation of Rusal in 2007. Had the Spanish prosecutor not opened a subsequent investigation into Deripaska and his associates, and requested the cooperation of the British judicial authorities, the fact that the FSA compiled a report on Deripaska would not have been publicly known today.

What FSA sources and underwriters say is that investigations of fitness to list are usually conducted in secret: if there is a negative outcome, that is negotiated behind closed doors. When the FSA finds serious grounds for objection to a listing, the underwriters and the applicant company are usually encouraged to go quietly, and withdraw. The FSA has not commented on the Shades complaint.

Uralchem has responded to release of the FSA submission by saying: “All the information about the company’s financial position is disclosed in its preliminary prospectus in the right order, based on audited financial statements . . . Neither the company nor its subsidiaries have had any claims or orders from state authorities regarding its solvency.”

What makes the Uralchem case unusual is the volume of detailed evidence that has now been made public, including American detective work, which had earlier been passed as harmless for investors by the underwriting banks. The case also opens up for investigation the conduct of the underwriters and auditors if the evidence submitted to the FSA suggests they may have been negligent; or if they had intentionally withheld information from the market for the benefit of their client – and for their own fee, share, and bonus stake in the listing.

If the London regulator has been tempted to agree, quietly and discreetly this time round, that conflicts of interest were motivating the underwriters to persuade investors to buy Uralchem shares, then does the outcome remove the stigma from Russian companies that may follow Uralchem into the same market? According to the Shades submission, the FSA should act to bar listings when they “could undermine investor confidence and be detrimental to the reputation of the London market as a whole.”

That said, what of the reputation of the Hong Kong Stock Exchange and of the Hong Kong regulatory authority, the Securities and Futures Commission, whose parallel investigations of the Rusal application late last year did not call into doubt the fitness of the company, its disclosures, or its controlling shareholder, and the ongoing litigation liability. Russian companies seeking to sell shares internationally are reported to be considering Hong Kong if and when London is barred to them. If misinformation and conflict of interest are recognized as poison for investors in London, what the Hong Kong regulator has done publicly — and the Hong Kong Exchange chief executive privately — is to claim probity on condition that an antidote is published.

Leave a Reply