By John Helmer, Moscow

EN+, one of Oleg Deripaska’s holding companies, announced today it has swapped $500 million of its debt to VTB, the Russian state bank, for a 4.35% shareholding which the bank will now hold in EN+. Oleg Deripaska, who owns all of EN+ through another of his holding companies, Basic Element, was the seller. The transaction price means that Deripaska accepted a valuation by VTB for all of EN+’s assets of $11.5 billion:

500 ÷ 0.435 = 11.49

According to the EN+ announcement, Yury Soloviev, first deputy chairman of the bank says: “We believe that En+ has an immense growth potential that is primarily related to the strengthening cooperation between Russia and China in the energy, metals and mining sectors.” According to Artem Volynets, the EN+ operating chief under Deripaska, “we are delighted that VTB Capital has become a shareholder of En+ Group. Our partnership is a very important milestone as we grow towards taking En+ Group public.”

(VTB has been too preoccupied this week to mention the Deripaska debt for equity deal. The bank’s preoccupation is with the state-directed takeover of the Bank of Moscow and the neutralization on the VTB balance-sheet of the effects of related-party (read bad) Bank of Moscow loans worth about $14 billion, and the disappearance of the collateral securing those and other loans.)

VTB’s valuation of Deripaska’s assets implies a more parsimonious counting scheme than the one employed for Bank of Moscow. For example, at the current market price of Rusal shares, EN+’s 47.41 stake is worth $9.7 billion in value:

20.48 x 0.4741 = 9.71

That in turn means that VTB counts everything else EN+ owns as worth just $1.78 billion:

11.49 – 9.71 = 1.78

According to a report to clients today by Dmitry Vinogradov, an analyst with UBS Moscow, “while the equity-for-debt swap is clearly a non-core business for a traditional banking corporation, from a valuation perspective we believe the exchange terms provide some upside for VTB. We estimate the current market value of the Rusal and EuroSibEnergo stakes is c$9.4 bn (based on yesterday’s market cap) and $5 bn (the upper end of the valuation range done by investment banks for the company was $5.6 bn), implying the value of a 4.5% stake in En+ is a minimum of c$650 mn, above the forgiven loan amount of $500 mn. We note the holding in En+ will remain illiquid for at least a few years; En+ intends to go public in two-three years.”

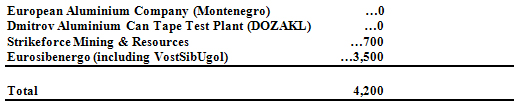

UBS is, to say the least, generous in counting asset value, and estimating how much time VTB is planning to wait to realize a rate of return. If VTB has done its due diligence, it knows that at the attempt by Strikeforce Mining & Resources, one of the assets in the EN+ holding, to sell shares on the Hong Kong Stock Exchange in the spring of 2010, then most anyone in China would value the company at $700 million. Then in May of 2010, EN+ announced it was planning to sell shares of the entire holding, including the little mining company, in an initial public offering (IPO), scheduled for October or November of that year; the announced underwriters were Bank of China and Deutsche Bank. In fact, noone wanted to buy EN+, so Deripaska changed plan, and proposed an IPO for Eurosibenergo, the electric generating asset in the holding. That too failed to make it to IPO, when there was no buying interest above $3.5 billion.

By no stretch of the imagination can this record be described, as does Soloviev of VTB, “the strengthening cooperation between Russia and China in the energy, metals and mining sectors.”

So, to itemize all the non-Rusal assets in EN+, and count the top market value of Strikeforce Mining & Resources and Eurosibenergo when they were last presented to a genuine market, here’s what you get:

4.2 – 1.78 = 2.42 ÷ 1.78 = 1.36

In words of one syllable – VTB thinks the EN+ assets are worth much less than the Bank of China, Deutsche Bank, other financial advisors, and the Hong Kong market have told the proprietor they are worth.

Allowing for the fact that just two years ago, Deripaska’s accumulated corporate debt exceeded $20 billion, making him the most indebted individual in the world, VTB is fixing a conservative valuation on the collateral value of the assets against which the VTB loan has been pledged. But it cannot be ignored that if there were a default and VTB had to try selling the assets, it has determined that some of them are worthless, or would have to be given away for free; while the main ones cannot find a market at half the price at which their IPO underwriters were finding buyers just one year ago. That’s what UBS calls an upside. Another word for it is downside.

Because Volynets looks to be admitting now that Deripaska has gone back to Plan A, selling shares in EN+, rather than Plan B, selling shares in Eurosibenergo and Strikeforce Mining & Resources, the downside valuation by VTB in the latest transaction explains why. The sum of the whole, even at a whopping discount, may turn out to be more promising than the sum of the parts has already proved to be.

And if the UBS client report is also right – that an IPO for EN+ is two to three years away – VTB’s assessment must be that it will be at least that long before an appreciation in capital value of EN+ would rise above the interest rate EN+ is currently paying on its $500 million loan.

So why should VTB think at all of turning a secured loan into an unsecured minority shareholding? What does VTB know about the future of Deripaska’s assets, including Rusal, which the market has yet to learn? The answers to such questions make price-sensitive information which on the equity sales desks of regulated investment banks would count as insider trading, if they traded on it. To be sure in this case, noone is trading, and nothing is known – in the strict sense of the second word.

Leave a Reply