By John Helmer, Moscow

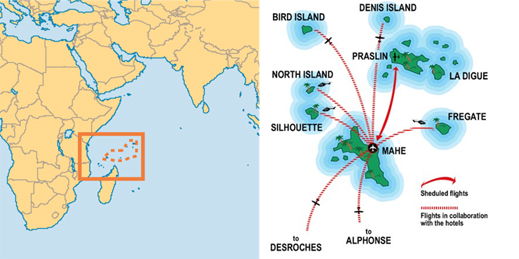

Smelting aluminium is a dirty business, so it’s every smelterman’s dream to recuperate on a tropical island far from the Big Smoke. Denis Island, for example, three balmy degrees south of the Equator in the Indian Ocean. And so, once upon a recent time, Oleg Deripaska (lead image), control shareholder of the Russian aluminium monopoly Rusal, downed tools, shut the door on his potline, and flew off. To Denis Island, where he was accompanied by his own valets, cooks, servers, and maids.

Or is this the fantasy of Rusal employees, fearful of wage payment delays and job losses looming in the management’s new plan, according to an insider at Rusal headquarters in Moscow? “The crisis will not miss a single industry,” Deripaska predicted early in the year. “’The worst is yet to come.” For whom? Rusal insiders at Moscow headquarters ask.

Sources on Denis Island say that keeping Deripaska’s visit secret by using a local agent’s name and replacing the hotel staff with its own entourage, a Russian group took over the entire island and the 25 cottages of the hotel complex in March of 2014. “What could be more natural”, reports the hotel, “than celebrating the promise of love in this magical, exclusive retreat. Here, neither time nor convention will intrude upon your tryst of moonlit strolls and intimate privacy. And, from the most simple, elegant wedding… to sophisticated events with the whole island privatised for you, our dedicated team is on hand to ensure that your every wish is met ; that this most personal and romantic of occasions is truly memorable.”

The outlay was more than €23,000, according to a Financial Times estimate of the rental of the Denis Island for one blissful day, one sublime night. Rusal insiders say there was a repeat visit for Deripaska this past Russian summer. The Denis islanders say it wasn’t their island, pointing across the water at North Island; that’s where Deripaska’s partner and Rusal shareholder, Mikhail Prokhorov, has been the owner of the island and Mine Host of the hotel since 2011. The hotel continues to keep Prokhorov’s name out of its history. It also says it is obliged to keep confidential the details of its latest Russian visitor; Deripaska’s spokesman refuses to respond.

Islands in the Seychelles group

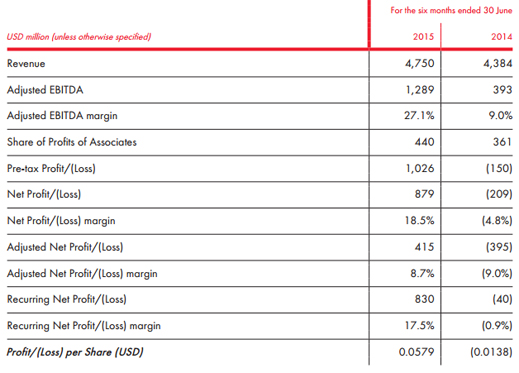

As the holiday was ending in August, Rusal announced good financial news for the six-month period to offset the poorer sales results it had released the month before for the three months to June 30. Production of aluminium in the second quarter was flat, compared to the first quarter; but volume of sales dropped 5.1%. The realized sale price for the metal fell 7.7%, as the London Metal Exchange cash price and the warehouse premium declined. For more on the importance of the warehouse premium to Rusal’s bottom line, read this.

Comparing the first half of 2015 with the same period of 2014, aluminium prices and premiums were better, so Rusal’s revenues followed upwards by 8.4%. The collapse of the rouble reduced the equivalent dollar value for Rusal’s costs, so the cost-of-sales line on the balance-sheet fell by 11.9%.

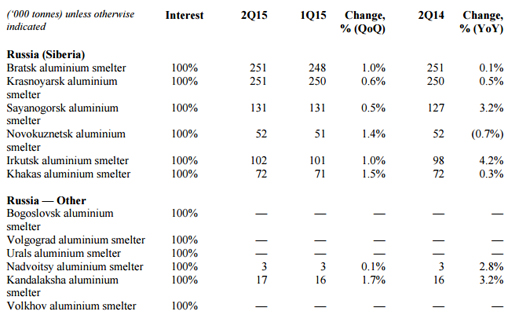

RUSAL’S ALUMINIUM PRODUCTION IN RUSSIA

Source: http://rusal.ru/upload/uf/695/28%2007%202015%20RUSAL_Trading%20updates%202Q15.pdf

RUSAL’S ALUMINA PRODUCTION IN RUSSIA

Source: http://rusal.ru/upload/uf/695/28%2007%202015%20RUSAL_Trading%20updates%202Q15.pdf

RUSAL’S BAUXITE PRODUCTION IN RUSSIA

Source: http://rusal.ru/upload/uf/695/28%2007%202015%20RUSAL_Trading%20updates%202Q15.pdf

The output numbers for the Russian plants in these tables are positive, with just two exceptions — the Achinsk alumina refinery (Krasnoyarsk) and the North Urals bauxite mine (Sverdlovsk). Last week a survey of unions representing Rusal workers at each of these plants, and of regional government agencies responsible for employment and wages, reveals no sign of layoffs or wage arrears.

But there are problems of growing wage arrears across the country. The government is reporting that by August 1 company arrears (delayed wages, not delayed state budget payments) had jumped 6.1%, compared to July 1. The worst affected regions were Novosibirsk, Moscow, Murmansk, Irkutsk, and Komi. But not at Rusal, not this year– not yet. The social media in the areas around the aluminium smelters, refineries, and mines also reveal no current complaints.

The company’s financial reporting reveals there has been a 32.1% fall in personnel expenses in the first half of 2015, compared to a year ago. Management explains this as the consequence, not of layoffs, but of devaluation of the rouble. Read the financial evidence and the management analysis here.

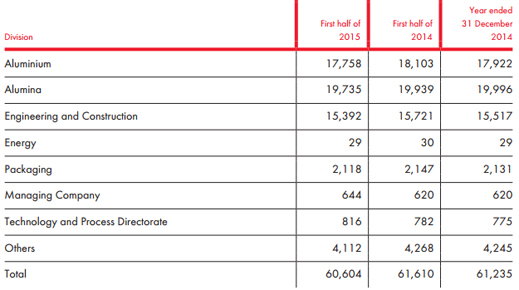

The latest report also reveals employee numbers are down by 1.6% overall in the first six months, compared to 2014. The numbers in the aluminium division were cut by fractionally more at 1.9%. With a total head count as of June 30 of 17,758, Rusal’s aluminium division comprises 29% of the company aggregate. The Russian smelters produce almost all (97%) of the metal the company sells.

Rusal’s alumina division is slightly larger – 19,735. That makes 33% of total company head count, including non-Russians employed at alumina plants in Ireland, Ukraine, Australia, and Jamaica. These non-Russians turn out 64% of Rusal’s alumina; the Russians, just 36%. The payroll cut in the alumina division has also been slight — just 1% year on year.

RUSAL HEAD COUNT – FULL-TIME EMPLOYEE EQUIVALENT

Source: http://rusal.ru/upload/uf/5cd/EWF101.pdf -- page 33

The output, the wage cost and the head count numbers all indicate that Rusal is delivering what the Kremlin stakeholder and the state bank creditors demand – stability at home. The bottom line on the balance-sheet also produces a positive recurring profit – that’s Rusal’s business without counting the dividend from the Norilsk Nickel shareholding:

Source: http://rusal.ru/upload/uf/5cd/EWF101.pdf -- page 3

The good news on paper ought to have been as good on the Hong Kong stock market, Rusal’s primary listing exchange since 2010. But since August Rusal’s share price has seesawed in a narrow range between HK$3.20 and HK$3.55; that’s close to the bottom of its value in the year to date, and well below last year’s share value. Market confidence in Rusal’s financial performance isn’t evident.

RUSAL’S SHARE PRICE, ONE YEAR TRAJECTORY

Source: http://www.bloomberg.com/quote/486:HK

Nor has the good news been convincing inside management in Moscow. This is where the reports of worse to come are discussed, and anxiety is growing. But not at the very top, not those on the roster for the Seychelles.

Source: http://rusal.ru/upload/uf/5cd/EWF101.pdf -- page 87

The company won’t explain who is “key management”, who is not. Those who are not are the sources for the disclosure of Deripaska’s trip to Fantasy Island.

The chief executive, Vladislav Soloviev, has

The chief executive, Vladislav Soloviev, has

warned that the smelters at Novokuznetsk in Kemerovo and Kandalaksha in Murmansk might soon suffer big production and job cuts if the regional and federal governments refuse Rusal’s demands for cuts to state railroad and electricity charges. Soloviev is also asking for Russian government measures to combat the surge of Chinese exports of semi-finished aluminium, which he describes as “fake

exports – ingots in a different form, called semi-finished product.” According to Soloviev, Rusal is thinking of taking back

the rolling and pressing of aluminium into sheet and plate in Samara and Rostov, which Deripaska sold to Alcoa of the US in 2004. For that story, and for other assets Deripaska was attempting to sell to Alcoa that year, read this.

Alcoa re-sold the Rostov plant, Belaya Kalitva (BK), in April of this year to a Russian alloys specialist, the Stupino Titanium Company; this is controlled by the state-owned Russian Technologies (Rostek) group. Industry press reports of this sale failed to note that the deal was lossmaking for Alcoa. In the small print of Alcoa’s financial report to the US Securities and Exchange Commission (SEC) on July 17, the company revealed it had taken a $159 million charge on the deal. According to Alcoa, last year the BK plant generated sales of $130 million, and employed 1,870 workers. But the Alcoa report fails to say that BK has been loss-making for several years, as Russian sources concede. Alcoa does admit that one reason for its losses was “the inability to pass-through the cost of metal premiums to can-sheet packaging customers in Russia.” For premiums, read Rusal charges.

The BK aluminium sheet rolling-line; source: http://www.amr-trading-ag.com/Default.aspx

For the time being, Alcoa is hanging on to the Samara Metallurgical Plant (SMZ). It produces flat aluminium products (below, left), pressed extrusions (right) and forgings.

Source: http://www.alcoa.com/russia/en/info_page/photo_gallery.asp

“There is now a discussion within Rusal,” Soloviev acknowledged, ”– whether we return back to semi-finished production, or even to some end-products such as wheels or cables. At the board of directors we plan to discuss this before the end of the year.”

Soloviev didn’t exactly accuse of Deripaska of making a mistake when he abandoned the Russia-first strategy of integrating all aspects of aluminium fabrication inside the country, opting instead for the offshore strategy of selling aluminium ingots worldwide. Nor did he acknowledge fresh state pressure on Rusal to make Russia less vulnerable to US economic warfare. Soloviev explained why, without fresh state financing, what was profitable for Deripaska a decade ago can’t be profitable in the Russian economy now. “Then it was the right decision,” Soloviev said. “There are special types of products — plates, can stock. These are complex and specific products. They require huge investments. Such a plant costs $400 to $600 million. We are not yet ready for such capital investment in our situation. But some simpler kinds of products, of course we can produce them.”

Even as Rusal is being obliged to retrace Deripaska’s tracks towards re-nationalization, he has announced that EN+, the asset holding through which he controls Rusal, wants to take its electricity sales downstream into large-scale data processing in the Irkutsk region. “Cheap electricity, combined with lower cooling costs attributed to the Eastern Siberia’s cold climate, will increase the competitiveness of our data centre in the fast-growing Asian market,” Maxim Sokov (below left), chief executive of EN+, said as a memorandum of understanding was signed in Beijing with Wan Biao (right) , head of Russia for China’s Huawei communications group on September 3.

“En+ Group, HUAWEI, Centrin Data Systems, LANIT Group and the Irkutsk region Government today signed a framework agreement in Beijing to build one of Asia’s largest datacenters and related infrastructure… The objective of the project is to create a 1,800 rack datacenter by 2018. It will be extended to 8,000 racks by 2024, or about 1% of the Silk Road Economic Belt countries’ total cloud computing market. The datacenter will provide hi-tech IT solutions such as cloud services, high performance computing and big data analysis systems to Russian and Asian markets, particularly in China.”

The capital cost estimates vary sharply. According to one, a pilot project costing $2 million is to be built by next year. According to EN+, the stage to 2018 will cost $55 million; a third stage to 2024 will cost another $300 million. Cutting the power cost for cloud computing and data storage isn’t the only issue on which the project depends. Securing computer operations, data storage, and internet transmission from foreign espionage is another. It is unclear too how the Chinese and Russian governments view each other for cyber security.

EN+ appears to think that Huawei will draw Chinese clients into the new centre; statements by Wan Biao suggest Huawei is looking to Deripaska to attract Russian clients. On Huawei’s website this month the company announced project plans with Bosnia, Egypt, Ethiopia, Jordan, Kuwait, and Serbia. Huawei ignores Russia, the agreement with EN+, and Deripaska.

IKS-Consulting, a leading Russian analyst of the domestic cloud computing market, is forecasting the doubling of computer capacity and value for the commercial segment. The electricity requirement is tripling. The state segment of the market, covering state companies, personal data, and security services, is developing rapidly in parallel, financed by the state budget. The state telephone company Rostelecom and Rostek, the state technology conglomerate, are building new data centres to meet the state demand.

Russian computer experts say they are sceptical that the Russian security services will encourage the participation of Russian corporations in the EN+-Huawei project, or the Chinese security services for their companies. “This is a fantasy on Oleg Deripaska’s part”, claims a Rusal insider.

Leave a Reply