By John Helmer, Moscow

For the first time Alrosa, the state-owned diamond miner, has come out in public and said it wants to buy Grib, the only commercially developed Russian diamond mine owned by LUKoil and its chief executive, Vagit Alekperov. Why it should say so now, when earlier announcements by Alrosa have veiled the target and concealed sale and purchase talks with LUKoil a year ago, isn’t clear.

“If the asset proves to be interesting,” said Igor Kulichik, Alrosa’s chief financial officer, “and if we agree on the price then we are prepared to discuss with Lukoil the purchase of this asset.” Kulichik was briefing sector analysts on Alrosa’s third-quarter financial results on December 5. He was explicitly asked about the Grib sale by a VTB analyst. “We know this asset quite well and we follow it. Yes, Lukoil is targeting to commence production and beneficiation early next year and in the next year they are targeting to already sell from there. We discussed with Lukoil a potential sale of that pipe about a year ago. But our geologists find it difficult to assess exactly what raw material is there in that pipe. So we decided not to rush, basically to let Lukoil start production there, see what comes out of that pipe, see how it develops and then to consider the potential purchase of the asset.” Kulichik made his comment on December 5; Alrosa published the transcript five days later.

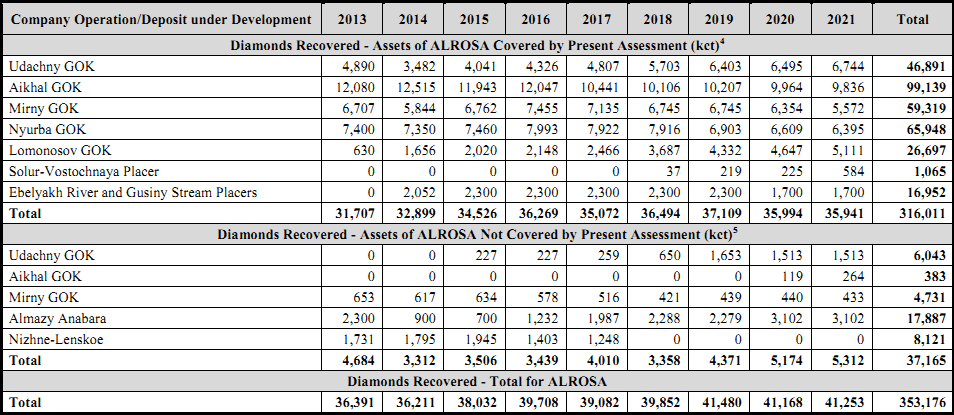

In June of 2012 Alrosa revealed its plan to lift diamond sale revenues to about $12 billion by 2021, an almost threefold jump compared to the Rb136.4 billion ($4.3 billion) result reported for all of 2012. This was achievable, the company claimed, if diamond demand grows by 38% to 2021, according to the Alrosa forecast, and if it can capitalize on higher grades and qualities from the underground mining sources it is developing in the Sakha region. Output of diamonds is planned to rise from 33 million carats in 2012 to more than 41 million carats by 2021. Reserves, according to this plan, are to jump from the current estimate of 607 million carats to 1.2 billion carats. Investment to get at the additional stones over the decade, Alrosa estimates, would total Rb234.6 billion (about $7 billion). The additional reserves, Alrosa said in its plan, should come from “the possibility of purchasing diamond-mining assets, first of all, on the territory of the Russian Federation.”

Kulichik was being disingenuous when he claimed last week that “our geologists find it difficult to assess exactly what raw material is there in that [Grib] pipe.” The data prepared first by De Beers, then by LUKoil, and confirmed by Rio Tinto, have indicated the new Grib mine holds mineable reserves of at least 98 million carats; that is roughly twice the volume of mineable diamonds compared to Alrosa’s Lomonosov mine next door.. Only one Alrosa mine, Aikhal in Sakha, has a mineable diamond reserve to compare with Grib, at least according to this expert analysis on which Alrosa’s long-term production plan is based.

Production Targets from the 2013 to 2021 ALROSA Long Term Development Plan

Source: MICON, Independent Expert Report on Reserves and Resources, September 2013

For details of the older reports by De Beers, which once owned Grib through Archangel Diamond Corporation, read here. For Alrosa to enlarge its reserve base from 607 million carats to 1.2 billion carats, the Alrosa geologists are already counting on Grib.

Presentations by the LUKoil management at Grib led by Maxim Mescheryakov indicate that more than $500 million has been spent to date on the new mine. At an average grade of 1 carat per tonne of ore, and at the three-year old price of $100 per carat, LUKoil is expecting to recover the cost of the mine in seven years. But given the rise in diamond prices to date, annual sale revenues by 2015 could be more than $650 million, and the payback period cut in half.

By volume of mine output, Grib trails behind the biggest of the Sakha region mines of Alrosa, which peaked at over 13 million carats per annum several years back. Today, the largest of Alrosa’s open-pit mines, Nyurbinskaya and Jubilee, are producing, respectively, 7.3 and 6.3 million carats per annum (2012). Grib will produce 2 million carats in 2014, and reach capacity the year after of between 4 and 4.5 million. Thirty kilometres away from Grib, Alrosa subsidiary Severalmaz is building its Lomonosov mine which is planned to produce about 2 million carats next year. Alrosa reports spending Rb120 billion ($390 million) on building this mine since 2010.

Arguably, Alrosa needs Grib more than LUKoil needs Alrosa. So the latter has played down Kulichik’s declaration of buying interest. An Alrosa source says: “This phrase is premature to be interpreted as a statement of a particular transaction; about that there is currently no talk. If a decision is made about whether to buy the Grib pipe, and both sides will offer a mutually satisfactory price, then we will discuss.”

LUKoil has replied: “Today the question of selling the deposit doesn’t stand at all. We’re going to start commercial production. Judging by yesterday’s media reports, we were included in the list of exporters of diamonds in 2014, along with Alrosa and its subsidiaries. Therefore, our task is now to begin commercial production and, accordingly, the implementation of these products. So now the question of the sale of this project is not being considered. As for price, it’s always a question of bargaining. We probably will count our total investment from how much we have invested for the entire period from 2008 to late 2013. This is the least of what we are likely to recover. But the international market is very difficult. We, of course, have certain valuations, estimations. But when we will enter into this market, understand how it works, then, perhaps, we will put our value on the assets [for sale].”

According to LUKoil, its plan for ceremonial commissioning of the mine, with President Vladimir Putin presiding, has been postponed from November to a date after the Sochi Olympics, which conclude at the end of February. Production at the mine will start this month.

Sergei Goryainov, a leading analyst at Rough & Polished, the Russian diamond industry bible, puts the likely acquisition price of Grib at over $1 billion; that is almost one-quarter of Alrosa’s current debt of $4.58 billion. The only way Alrosa will be able to manage that, he suggests, would be a government-arranged swap of assets in the oil and gas sector. “The Grib project has a very high cost. Lukoil has reported that capital expenditure has amounted to more than a billion. And this certainly is a big problem — whether Alrosa can allocate the free cash for the acquisition of the asset. Though of course Russia is Russia, and different variants are possible — LUKoil’s compensation is possible in different ways and in time and in space. Probably LUKoil will not require that kind of money to be laid out all at once.”

Goryainov says he does not expect that Alrosa would fight LUKoil at the Kremlin to gain control over the new mine. Nor does he anticipate that LUKoil would lack the administrative resources to resist if Alrosa tries.

Leave a Reply