By John Helmer, Moscow

Andrei Melnichenko (lead image, left) and Nathaniel Rothschild (right) are offering $100 million in cash, plus refinancing of at least $450 million in debt notes expiring in eight weeks. That’s money London bankers say Rothschild doesn’t have, and Melnichenko can’t borrow. The offer is for the takeover of Asia Resource Minerals Plc (ARMS), a London-listed operator of coalmines in Indonesia.

From his Channel Island headquarters Rothschild has announced the deal with Melnichenko for a joint takeover bid. But in Cyprus, where he is headquartered, Melnichenko is saying nothing. In Moscow, the Russian interpretation is a combination of scorn for Rothschild, and a determination to make out of an improbable business deal in Borneo the appearance of international clout which Russian business has lost. According to Russian investment banker number-1: “I have spent enough time in Indonesia so that I never even try to do business here – the deck is stacked against you. Nat is a serial [expletive; translation, passive recipient of forcible intercourse], and he is in for yet another treat.” Russian investment banker No. 2: “Russians are trying to break out of the corner in which the Americans have confined them. They will use any pretext. – any kind of foreign venture is designed to make Russian business legitimate and powerful looking. This is driven by the huge inferiority complex now felt by highly leveraged men like Melnichenko. They need to show they still can [expletive; translation, active initiator of forcible intercourse].”

On Monday (April 20) Rothschild said through his eponymous NR Holdings (NRH): “NRH and SUEK are considering a possible cash offer, to be made by a special purpose vehicle jointly owned and controlled by NRH and SUEK, to acquire the entire issued and to be issued share capital of ARMS not already owned by the NR Concert Party. Any such offer made would be conditional upon the Recapitalisation being completed.”

SUEK posted an identical statement. Readers were invited to make contact with its Cyprus office, but noone picks up the telephone at the listed number. Melnichenko owns 91.2% of SUEK; 7.8% is held by Vladimir Rashevsky (right) , the chief executive.

SUEK posted an identical statement. Readers were invited to make contact with its Cyprus office, but noone picks up the telephone at the listed number. Melnichenko owns 91.2% of SUEK; 7.8% is held by Vladimir Rashevsky (right) , the chief executive.

The history of the consolidation of coalmines in their present Russian hands is as fraught as the steel and aluminium industries with which they are connected. The asset and trading records of the major coalmining companies have limited their ability to list and sell their shares publicly, especially outside Russia. This in turn means they are not analysed by the major Moscow institutions. One consequence is that when SUEK withdrew its attempt at an initial public offering of 25% of Melnichenko’s shares on the London Stock Exchange in 2010, Rashevsky didn’t have to explain. Neither did Melnichenko’s advisors at the time — Citigroup, Credit Suisse, VTB, Renaissance Capital, and Bank of America Merrill Lynch. Melnichenko’s net work to them is a fraction less than the Forbes gross estimate of $2.7 billion. Quite a fraction.

ARMS is presently worth just 27 pence per share, £65 million in market capitalization. It has been plummeting towards worthlessness since April 2011, when the share peaked at £13 for a market cap of £3.1 billion. The wizardry of Rothschild started a year earlier in 2010. That’s when Vallar Plc was listed on the London market, with favour-calling and arm-twisting from Jacob, Nathaniel’s father. The initial idea was that the Russian iron-ore miner Metalloinvest, owned by Alisher Usmanov and Andrei Skoch, might be bought and reversed into the London listing which Usmanov and Skoch were unable to persuade the Listing Authority to approve on their own names. Read all about that here and here.

At the time, Rothschild’s reputation was for a knack of stepping away from lossmaking before his co-shareholders. That changed after he selected the Indonesians for his partners in November of 2010. The old Borneo habit of head-hunting and head-shrinking was civilized by comparison with what the Indonesian stakeholders have done to each other, and to Rothschild.

On its most recent report – dated last August — ARMS claims to be targeting production of 24 million tonnes of coal per annum at mines in three locations in the archipelago:

Source: http://www.indonesia-investments.com

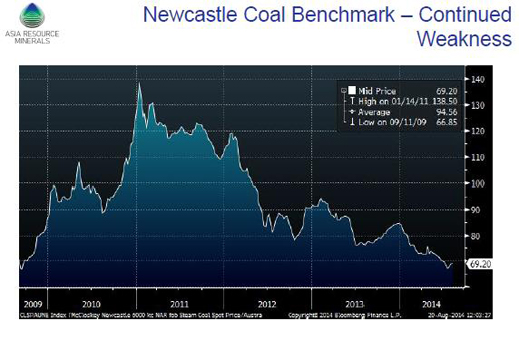

The stock market doesn’t think that’s such a good thing when the collapse of the coal price is what the company report calls “continued weakness.” In fact, the report admits that 30% of coal moving from mine to market is loss-making. Asian demand for coal accounts for 75% of the seaborne trade; according to ARMS “its consumption is forecast to grow steadily.”

Rothschild’s solution: “Much depends on the outlook for the thermal coal price, but we are continuing to focus on optimising our asset base through cost control and our Life of Mine plan…We also continue to enhance our financial controls and governance framework.”

Source: http://www.asiarmplc.com

ARMS is operating below break-even level, and to its book debt of $91 million must be added $450 million in obligations to be paid by July 8 of this year; and $500 million falling due in two years’ time. The company admits it tried to go to the market last year to refinance the first $450 million with a stretch to a redemption date of 2019; it couldn’t, it says, “due to adverse market conditions.” The last auditors’ note warned of “the existence of a material uncertainty which may cast significant doubt about the Group’s ability to continue as a going concern.”

More details of the buyout and recapitalisation can be found in Rothschild’s prospectus, issued on March 31. His move amounts to “an Open Offer of 271,002,710 Open Offer Shares at a price of 25 pence per share, representing a premium of 79 per cent. to the Closing Price of 14.0 pence per Ordinary Share on 6 February 2015 (being the last Closing Price prior to 9 February 2015, the date on which the Company announced that it had entered into Heads of Terms with NR Holdings to underwrite an equity transaction), to raise gross proceeds of approximately £67.8 million, which has been underwritten by NR Holdings.”

Maybe that was believable in London, but not in Djakarta and Hong Kong. There a rival takeover offer materialized in the market from the Sinarmas Group, an Indonesian conglomerate belonging to Eka Widjaja (right) and his family. Operating through a front called Asia Coal Energy Ventures Ltd. (ACE) and Argyle Street Management, a Hong Kong hedge fund, they are stuck with a 4.7% block of ARMS shares, and have as much enthusiasm for Rothschild’s buyout offer as many of Rothschild’s co-shareholders in the past. Widjaja, ACE and Argyle are offering more cash — 41p a share, making a contribution of $150 million to the company — but they are less certain on the refinancing of the $950 million.

Maybe that was believable in London, but not in Djakarta and Hong Kong. There a rival takeover offer materialized in the market from the Sinarmas Group, an Indonesian conglomerate belonging to Eka Widjaja (right) and his family. Operating through a front called Asia Coal Energy Ventures Ltd. (ACE) and Argyle Street Management, a Hong Kong hedge fund, they are stuck with a 4.7% block of ARMS shares, and have as much enthusiasm for Rothschild’s buyout offer as many of Rothschild’s co-shareholders in the past. Widjaja, ACE and Argyle are offering more cash — 41p a share, making a contribution of $150 million to the company — but they are less certain on the refinancing of the $950 million.

This week’s fillip for Rothschild’s bid is the appearance of Melnichenko and SUEK. On 2013 data, Russia ranks sixth in total coal output in the world, trailing China, US, Australia, Indonesia, and India. Russian coal reserves rank third in the world. From the Kremlin’s point of view, the important point is that Russia leads in terms of unmined reserves, so Russian coalminers, government officials think, should be investing at home. Melnichenko, who is Belarusian by birth and has a home in New York, has had difficulty with this.

Rothschild has also leaked to the London papers that he has lined up the support of most bondholders and creditors for putting off the July deadline and recapitalizing the full $950 million owing. According to Rothschild’s version, printed in the Financial Times, he had in his pocket a bond debt deal from Ashmore, Pimco, Taconic, Fidelity, and Raiffeisen Bank.

TOP TEN PRODUCERS OF COAL IN THE WORLD, 2013

¹ commercial solid fuels only, i.e. bituminous coal, anthracite (hard coal), lignite and brown (sub-bituminous) coal

² million tons oil equivalent

Source: BP Statistical Review of World Energy 2014

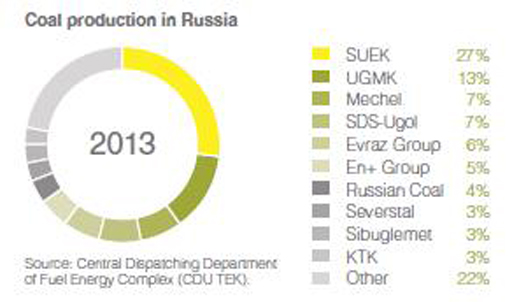

Among Russian producers of thermal and coking coal, SUEK (Siberian Coal Energy Company), with about 93 million tonnes of output a year, dwarfs ARMS. Roughly half of SUEK’s output is sold to related companies, also owned by Melnichenko, in the domestic market. Exports of coal go through Melnichenko-owned port terminals on to trading fronts in Switzerland and Cyprus; these appear to be holdings, with a network of subsidiaries, conduits, and fronts in other countries.

Most coal experts in the Moscow investment banks say they can’t follow SUEK. A handful of bank studies reinforce the suspicion of transfer pricing and unverifiable bookkeeping. The latest SUEK financial report for 2014 indicates that on sales of $5.1 billion, the group made a loss of $807 million. Long and short-term loans totalled $3.7 billion at December 31 last. The company doesn’t reveal its principal banks; among the Russian houses they include VTB, Sberbank, Rosbank (Societe Generale), and Bank Rossiya. For jot and tittle on Melnichenko’s record for transparency, accountability and likeability, read this archive.

Melnichenko is sensitive to the evidence that he keeps most of his cashflow offshore. He has responded to the Kremlin’s deoffshorization policy by announcing that Kuzbassenergo, a minor subsidiary, has been transferred to a domestic registration. As this report by Victor Andreyev suggests, this is a token fraction of the group’s cashflows and assets. Melnichenko’s last venture in offshore investment – a plan by Eurochem, his fertilizer holding, to build a billion-dollar ammonia plant in the US state of Louisiana – was disallowed in Moscow, and then cancelled by the start of the Ukraine civil war and US sanctions. Melnichenko, who lets his interior decorators, lawyers and wife do the talking to media, has also been hit by US sanctions. In March of 2014 the US Export-Import Bank said it was delaying indefinitely an application by SUEK for $21 million to finance American mining equipment exports to Russia.

SUEK is quoted by Kommersant this week as rationalizing the Indonesian investment as “strengthening its presence in the Asian markets” and providing “significant additional synergies” in selling coal to India, China, Malaysia, and South Korea. The SUEK spokesman also warned that Melnichenko might leave Rothschild in the lurch if Widjaja pushed the price up. “SUEK is considering participation in contributing to this transaction only as long as the possibility of the transaction, and the amount discussed, are not so large as to require additional funding.”

SUEK reports reveal export destinations for its coal by volume; the principal ones are China (12.6 million tonnes in 2013), UK (6.7 million tonnes), South Korea (5.8 million tonnes) Japan (4.6 million tonnes), Germany (1.7 million tonnes), Israel and Finland (1.4 million tonnes), Taiwan (1.3 million tonnes), India and Poland (1 million tonnes), and Spain (700,000 tonnes). SUEK doesn’t report the country breakdown of its sale revenues.

Andrei Tretelnikov (right), an analyst for Rye Man & Gor in Moscow, cautions that the deal “can be a little diversification. After some time the markets will recover and the company can profitably supply coal from Indonesia to China. Whether it strengthens SUEK is hard to say. It is necessary to know the details in order to say whether it is an interesting project or not, whether good or bad for SUEK.”

Andrei Tretelnikov (right), an analyst for Rye Man & Gor in Moscow, cautions that the deal “can be a little diversification. After some time the markets will recover and the company can profitably supply coal from Indonesia to China. Whether it strengthens SUEK is hard to say. It is necessary to know the details in order to say whether it is an interesting project or not, whether good or bad for SUEK.”

Not since the hairy octopus, an endangered denizen of Indonesian waters, was threatened by competing goldmine bids from Australians and a combination of Mikhail Fridman and Alexei Kuzmichev has there been a test of Russian business in Indonesia. That story from 2008 and the island of Sulawesi was told here. That was the year after Oleg Deripaska signed his first memorandum of understanding for a combination of bauxite mine and alumina refinery with Indonesian partners. Like the Fridman-Kuzmichev goldmine, it went nowhere.

A year ago, Deripaska (below 1st left) announced he was trying again in Borneo. The Indonesian partner is called PT Arbaya Energi, owned by the local oligarch Suryo Bambang Sulisto (right) of the Satmarindo Group. Presiding over their exchange of MoU’s in February 2014, was Deputy Prime Minister Dmitry Rogozin (2nd from left).

Source: http://www.kadin-indonesia.or.id

Maxim Sokov, a Rusal executive, told Reuters at the time: “Indonesia ticks all the boxes and is the best platform for the next cycle of growth… Our plan is to close all the high-cost smelters, keep our low cost base and look for the new opportunities to expand that low cost base. Indonesia is that new opportunity.” In Moscow Sokov doesn’t dare say that Rusal has closed its smelters in Russia with a plan to invest in Indonesia. “We’ll conduct feasibility studies by the end of this year and after that, we can start the project,” he claimed.

Rusal insiders said this week they don’t know what has happened to the feasibility study; Rusal’s spokesman refuses to say. The Borneo project hasn’t rated a mention in Rusal’s annual reports or in the company’s Hong Kong Exchange notices.

By joining Rothschild Melnichenko is pitting himself against the Indonesians, not with them as Deripaska has done. The outcome is likely to be the same, according to an investment banker familiar with all sides in the deal. “The proposed deal is a black hole, and it will fall apart. The reason for it is that Melnichenko has gotten government approval to make a move which looks like sailing under the flag of combatting sanctions.”

Melnichenko’s spokesman in Moscow Alexei Naumenko (right) was asked to clarify what proportion of the outlays and what proportion of the shares to be acquired by the joint bidding vehicle would be the property of NRH and of SUEK. He was also asked to say what undertakings SUEK has given NRH that it has received the permission of the Russian Government and Russian state bank lenders to SUEK for such an offshore transaction to proceed? Naumenko refuses to reply.

Melnichenko’s spokesman in Moscow Alexei Naumenko (right) was asked to clarify what proportion of the outlays and what proportion of the shares to be acquired by the joint bidding vehicle would be the property of NRH and of SUEK. He was also asked to say what undertakings SUEK has given NRH that it has received the permission of the Russian Government and Russian state bank lenders to SUEK for such an offshore transaction to proceed? Naumenko refuses to reply.

At Rothschild headquarters there was surprise that Melnichenko might not be the free agent, let alone the white knight he has presented himself to be. To the same questions Rothschild said through a spokesman that “NRH/SUEK have announced a possible offer. At this stage it is conditional and depends on a number of factors. NRH and SUEK need to make additional disclosure and when they publish the details I will send you a copy.”

Leave a Reply