By John Helmer, Moscow

It was a specialty of the Chicago Irish at the turn of the 20th century. A Mickey Finn was a drug that was slipped into your cocktail without your knowing, in order to incapacitate you. When you came to, the only thing you knew was that you were missing your valuables. The eponymous Mickey Finn was a pickpocket who built his capital into a thriving business as the proprietor of the Lone Star Saloon and Palm Garden on the corner of Dearborn and Harrison Streets. (It’s a Starbucks nowadays. The girls Mickey used as lures now drink skinny lattes.)

Maxie Finn, aka Maxim Finsky (left front), is eponymous too. He is a childhood friend of Mikhail Prokhorov (left back), and he has been employed by him to buy assets on the cheap; consolidate them into special purpose vehicles which the two of them then try to resell. They’ve had one signal success. That was when Prokhorov jointly controlled Norilsk Nickel, Russia’s largest mining company, with Vladimir Potanin. Finsky was employed to spend Norilsk Nickel’s money on buying goldmining assets at premium prices before they were spun off and separately listed as Polyus Gold. Finsky spent foolishly, or worse, read this. But no matter. The rise of the price of gold drove the share price of Polyus Gold ten times and more above the amount paid for its assets. For the ups and downs in that decade-long story, read here.

With a record like that, part of it documented on the London Stock Exchange, it’s not been easy for Prokhorov and Finsky to slip Canadian shareholders a powder. But they have tried, starting with the formula of reversing into already listed but insolvent junior mining companies. Here’s the story of White Tiger Gold (WTG), whose value destruction is almost solely Finsky’s doing, not Prokhorov’s. Before the company became virtually bankrupt at the start of this year, it was taken over by three other Russians – Sergey Yanchukov, Sergey Kashuba, and Evgeny Konstantinidi. They recently removed the odium by changing the company name to Mangazeya Mining Ltd. and changed its listing on the Toronto exchange to NEX, a lower-value, less regulated board. The company is still lossmaking; in default to VTB, and as of September 30, its accumulated liabilities are larger than its assets by $67 million. The share price of White Tiger aka Mangazeya has dropped 87% this year, and at one Canadian cent per share it is fractionally above worthlessness.

With their Intergeo vehicle Prokhorov and Finsky tried a direct listing with copper and nickel prospecting assets, not producing mines as had been the case with Polyus Gold. As a collection of assets spirited out of Norilsk Nickel by Finsky, when Prokhorov was fighting his former shareholding partner Potanin, its provenance wasn’t confidence-building. Its lack of production and positive cashflow didn’t help. The collapse of market prices for the minerals Intergeo claimed to have in plenty underground also discouraged sharebuyers. So Intergeo failed; actually, it failed twice. Here is that story.

Now on Prokhorov’s third bite of the cherry, he is buying 99% of 85% of Mercator Minerals Ltd.’s shares, more than enough to secure the required 66% shareholder approval for the deal. The terms were reported on December 12. That was one day before the deadline Mercator’s creditors had set for resolving indebtedness of almost $400 million.

Prokhorov has managed to halt bankruptcy action with a promise amounting to just one-quarter of Mercator’s debts, but with a cash outlay of just 3.5% of that sum. Even this has a sting in the tail for Mercator’s balance-sheet. Prokhorov is lending Mercator $14 million at 15% interest to forestall the creditors’ deadline of December 13; plus $36 million in insolvency rescue for Mercator’s Mineral Park Mine in Arizona; and promising $50 million more if the existing shareholders don’t get in his way. That bigger amount, though, isn’t exactly promised for Mercator’s active mining project in Arizona or its two mining prospects in Mexico. The small print in the deal announcement says the big money will be spent to “fund closing costs related to the Transaction, to advance the El Pilar [Mexico] and Ak-Sug projects and for general working capital.” Ak-Sug is the Russian copper project Intergeo has been unable to finance with Canadian shareholder money to date.

The deal also wards off another bidder, Nevada Copper Company, which currently owns 14.59% of Mercator’s shares, and was until now the largest single shareholder. Mercator went to court a year ago to prevent Nevada building up enough of a shareholding to effect a takeover.

Mercator’s chief executive, Bruce McLeod, a copper and molybdenum mining veteran, will be able to walk away with a lump-sum severance payment of two and half times his annual compensation. McLeod earned just over $1 million in 2011; $647,318 in 2012, according to company documents. McLeod took over management in April 2011 after Mercator merged with Creston Moly Corporation, which owned the El Creston molybdenum prospect in Mexico. The share and cash exchange was valued at the time at C$195 million (US$205 million). Less than three years later, the asset value of that transaction has been written down by Mercator by $152.5 million.

At the time Prokhorov and Finsky moved in Vancouver last week, Mercator’s accountants were acknowledging that without a substantial financial injection from somewhere, it was flat broke. “The Company recorded a net loss of $141.3 million for the nine months ended September 30, 2013 (September 30, 2012 – net loss of $13.5 million), and as at September 30, 2013, had an accumulated deficit of $391.2 million (December 31, 2012- $251.6 million) and a working capital deficiency of $94.4 million (December 31, 2012 – working capital of $2.0 million). The loss for the period includes impairment charges totaling $167.8 million in respect of the Mineral Park Mine and El Creston [that was McLeod’s company]. The working capital deficiency at September 30, 2013 includes $99.8 million of the Company’s debt arrangements (note 6). The Company did not make the required September 30, 2013 scheduled principal payment of $4.8 million which constitutes a Payment Event of Default under the Company’s Credit Facility and related amendments. The default under the credit facility resulted in cross-covenant violations under the Company’s Equipment Loans. When preparing the condensed consolidated interim financial statements for the third quarter 2013, the Company also determined that it may have breached one of the covenants under the Project Financing as of September 30, 2013. Therefore, the non-current portions of all these debt arrangements have been classified within current liabilities as at September 30, 2013.”

Mercator will now be buried, and the new company will be called Intergeo Mining Limited, a name the Toronto stock market wouldn’t subscribe to a year ago.

Canada’s Financial Post, which operates giveaway advertising schemes, describes the Prokhorov-Finsky takeover of Mercator Minerals as “a win-win: Mercator’s balance sheet problems get resolved, and Intergeo gets copper projects that could make it a significant industry player in a relatively short time. Mercator shareholders get diluted but will continue to have an interest in the future company’s success. Mercator’s Mineral Park mine in Arizona is already in production, but it is struggling and needs a number of upgrades. The cash infusion from Mr. Prokhorov’s ONEXIM Group will allow Intergeo to fix it up. The next step is to develop Mercator’s El Pilar mine in Mexico, which is expected to produce roughly one billion pounds of copper over 13 years.The cash flow from those two mines will help Intergeo develop its own Ak-Sug project in Southern Siberia, a larger and more challenging project that has a longer timeframe.”

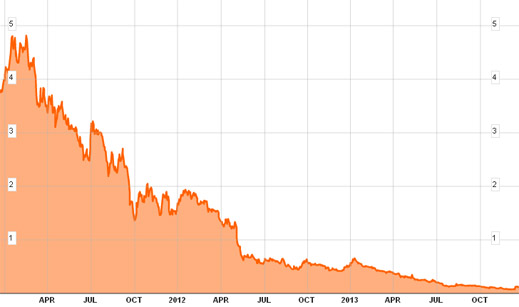

Prokhorov has not invested before in a payback scheme lasting thirteen years, let alone “a longer time frame”. He is reported this week in the Moscow business newspaper Vedomosti as claiming that in 2011 Mercator was worth $1.2 billion. “We have bought a unique asset for an insanely low price. I think that when combined with the assets of Intergeo, when the cycle comes back, the company will be worth several billion.” As can be seen from the following chart, Mercator’s billion-dollar valuation lasted for just a few days: by the end of 2011 it had crashed from a high of C$4.56 to C$1.46 (C$461 million; US$484 million).

CHART OF MERCATOR MINERALS SHARE PRICE, 2011-2013

Source: Bloomberg

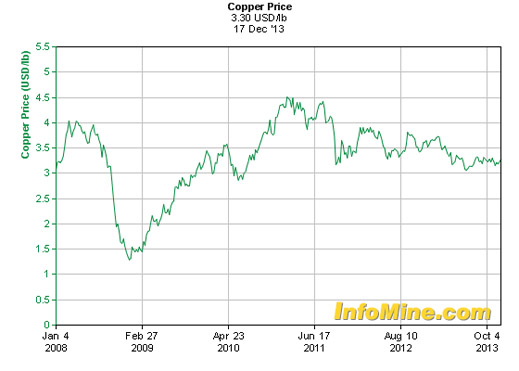

It hasn’t stopped falling. Part of the reason can be seen from the price track for copper, which tumbled sharply in 2011, and is currently pushing at the 2011 lows.

Prokhorov and Finsky were asked to clarify what management role Finsky will play at Mercator Minerals. Prokhorov’s spokesman at his Onexim holding in Moscow deflected all questions about the Mercator transaction to Intergeo because “it’s not a direct purchase of Onexim, so it’s better to ask Intergeo or Mercator.” At Intergeo’s Moscow office Finsky’s spokesman responded that he will be become Chairman of the Board of Directors in the new company.

Finsky was also asked this question: Now that Intergeo has been able to list itself on the Toronto Exchange, what confidence does Intergeo have that it will not repeat the shareholding value destruction which occurred at White Tiger Gold? Finsky’s spokesman replied that she had forwarded the question to Finsky, and promised that if there will be anything in reply from him, she will say. There isn’t; she hasn’t.

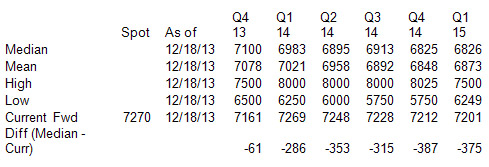

Many global copper miners, including Norilsk Nickel, Russia’s leading producer and exporter of copper, share Prokhorov’s hope that there will be a recovery in the copper price soon. But noone in the industry is betting this timing will be soon. In the two to three-year term, in which Prokhorov has placed his bets in the past, the Bloomberg consensus is that the negative distance between today’s spot price and the future forecast gets bigger.

In the short term, the consensus of copper analysts monitored by Bloomberg is that copper’s current spot price (today it is $7,228 per tonne) will continue to fall through the first quarter of 2015.

THE FUTURE PRICE OF COPPER – CONSENSUS OF ANALYSTS POLLED BY BLOOMERG

Source: Bloomberg

According to Morgan Stanley’s report of December 3, not even the evidence of revival in demand for copper in China, the consumption of surplus metal inventories and stocks, and tightening in the global supply-demand balance for the metal fail to shake the forecast of a continuing decline in the copper price. Notwithstanding the optimism, Morgan Stanley is predicting that five years out, the copper price in 2018 will average $7,165 per tonne. That is still $63 below today’s price.

With a future like that, and a record like Finsky’s, what are the chances for Prokhorov to realize his multi-billion dollar gain? So far Canadian shareholder comment on the takeover of Mercator remains unpersuaded by the Intergeo magic. According to one Canadian expert, “it appears they finally managed a TSX listing by way of a reverse takeover. Their past transactions look to be quite a mess of smoke and mirrors. I suspect this was [Mercator’s] last option before bankruptcy. It could be that they actually try and build value in this new combined entity. Still, I suspect there will be many games going forward to the benefit of management and majority shareholder. Although we know how weak the Canadian regulators are, Intergeo will still have to play by the rules generally.”

Leave a Reply