By John Helmer, Moscow

Ziyavudin Magomedov’s hold on the ports of Novorossiysk and Primorsk, and the oil which flows into and out of them, deteriorated suddenly and publicly this week. This has triggered new concern in The Netherlands that Magomedov’s Summa Group will be unable to find the money to break ground, as scheduled next month, at their new oil terminal project at Rotterdam. There is also concern among Rotterdam traders that if Magomedov cannot get the Russian crude oil he needs to fill his new tanks, he may substitute it with a flood of ship (bunker) fuel that will push down on the price of Rotterdam bunkers. Magomedov’s troubles in Moscow are thus causing a negative domino impact on his Dutch business allies.

The story of how Magomedov won a Rotterdam competition in 2010 for Tank Terminal Europort West (TEW), with a promise to deliver 600,000 barrels a day of Russian crude, can be read here. Last week, the state crude oil pipeline company Transneft went public in a direct attack on Magomedov and his Summa group, hinting that there will no Russian crude oil for the Rotterdam project, at least not from Primorsk port, whose pipelines Transneft controls, but whose management Magomedov runs through the Novorossiysk Commercial Seaport Company (NCSP). Recent disclosures from oil companies working with Magomedov’s oil trading subsidiaries, such as Souz Petrolium (not a spelling mistake), suggest that Magomedov is switching to trade of large volumes of Bunker C, the ship fuel with the highest sulphur content.

Sulphur pollution of the air – from vessel funnel fumes, and from transfer in and out of storage tanks – is a high-priority concern at North Sea ports, especially Rotterdam. Magomedov has already run into a challenge by the Russian regulator RPN of his air emission compliance at Primorsk.

Not since Oleg Deripaska’s Rusal opened his hostile takeover attempt against Vladimir Potanin and Vladimir Strzhalkovsky at Norilsk Nickel have two rival stakeholders of a major Russian company aired their differences in public. But until this week, Summa had not responded directly to the criticisms of Transneft, or its proposal to replace Magomedov’s trusties at NCSP with Transneft men.

On Monday Magomedov’s fight with Tokarev went into the Big Top, as the NCSP chief executive loyal to Magomedov, Rado Antolovic (right), held a press conference in Novorossiysk, and Transneft’s first vice president, Maxim Grishanin (left), a member of the NCSP board of directors, called a press conference of his own in Moscow.

On Monday Magomedov’s fight with Tokarev went into the Big Top, as the NCSP chief executive loyal to Magomedov, Rado Antolovic (right), held a press conference in Novorossiysk, and Transneft’s first vice president, Maxim Grishanin (left), a member of the NCSP board of directors, called a press conference of his own in Moscow.

Two months ahead of the scheduled release of NCSP’s audited financial report for 2012, Grishanin announced some of the interim figures, casting doubt on the current management’s ability to trade its way out of revenue weakness and cover NCSP’s ballooning debt. Grishanin reported that NCSP’s 2012 revenues had declined to Rb32 billion ($1.03 billion), down 2% on 2010. Earnings, however, were reportedly up 6% to Rb18.3 billion ($589 million). According to Grishanin, “if you look at the preliminary results of the NCSP in 2012, you will see growth indicators: EBITDA, revenue and turnover increased by 1.2%, but the average for Russia, it increased by 5.6%,”

A warning to clients by Uralsib Bank maritime analyst Denis Vorchik calculates that these year-end figures also mean that in the fourth quarter NCSP’s revenues fell by 9%, while earnings plunged by 19%.

NCSP retaliated, issuing a warning on the company website that “investors should not rely on this information. The FY 2012 financial information previously disclosed and disclosed here is preliminary and based on internal management accounts, has not been converted to IFRS or audited and may be significantly adjusted during the course of the preparation of the Group’s audited IFRS financial statements.”

At CEO Antolovic’s counter press conference, he claimed there had been a board meeting last week to consider the year-end results, and that Grishanin hadn’t spoken up with objections at the time. “It’s not a matter of correct or incorrect,” Antolovic said. “It is simply wrong to disclose figures that have not been audited. I was very surprised when I read that. My team and I will be successful, not by 90 percent but by 100 percent, and the results speak for themselves,”

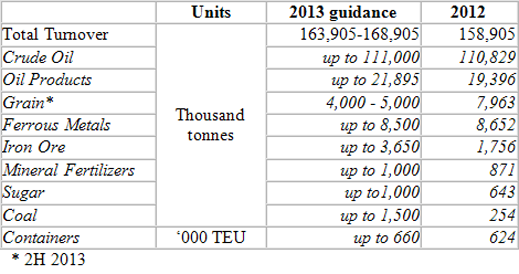

Antolovich also attempted to neutralize Grishanin’s bad-news pitch with an optimistic forecast for the port company’s turnover this year, predicting up to 6% growth in cargo volume to 169 million tonnes, led by a fivefold growth in coal shipments; 33% growth for grain; double the volume of iron-ore exports; and 6% growth for containers.

Since the optimism for each of the cargo predictions depends on uncontrollable factors – weather for the grain harvest, for example, and rising demand at foreign steelmills for growth of iron-ore exports – Vorchik reported skepticism to Uralsib Bank clients. “[NCSP’s] bullish outlook for 2012 turnover did not materialize as turnover grew only 1.2% YoY and thus lagged the Russian seaport market last year.” At his press conference Grishanin claimed “real companies are going to other ports,” and NCSP has been failing to invest as much as it should in new port facilities.

NCSP managers have countered with the claim that Transneft had long ago agreed to revisions of the investment spending plan, and that during the past year NCSP had gained extra cargo volume, compared to rival Russian ports, in mineral fertilizers, iron ore, coal and cars.

“The results speak for themselves,” claimed Alexander Vinokurov, Magomedov’s deputy at Summa, in his first public statement after refusing to respond to questions for several weeks.

“The results speak for themselves,” claimed Alexander Vinokurov, Magomedov’s deputy at Summa, in his first public statement after refusing to respond to questions for several weeks.

“An increase in traffic, revenue growth, diversification of cargo base, the timely implementation of the investment programs, etc. With the team led by Antolovic we have no doubt that the long-term development strategy, voted for all shareholders, including representatives of Transneft, will be carried out.”

NCSP’s share price has been picking up steadily since mid-January, but as details of the conflict with Transneft have spilled out, the share started to retreat this week. “Uncertainty on ownership structure remains,” warns Vorchik for Uralsib Bank. The fight may end in a partition of the assets, warns Infranews.Ru editor, Alexei Bezborodov, perhaps even a restoration of the status quo ante, before Novorossiysk and Primorsk were merged.

Leave a Reply