By John Helmer, Moscow

As famous hoaxers go, Igor Sechin (lead image, centre), the chief executive of Rosneft, Russia’s largest oil company, is at least as clever as Clever Hans (right), a German horse of the late 19th century.

Hans was apparently good at arithmetic. If his owner asked him to multiply three by four, he would tap his hoof twelve times. He could tell the square root of sixteen by tapping four times. He was also able to give answers to questions he hadn’t heard before. So he was a very famous horse in Germany. That was until a sceptical psychologist realized Hans would only get the answers right if his owner also knew the answers, and if the horse could see him when the questions were asked. If the owner or another questioner was invisible to the horse’s eye, Hans would fail. He even bit the psychologist after a string of tests produced wrong answers. The psychologist’s conclusion was that the horse was gifted, but not at arithmetic. Hans could detect the visual cues his questioner would give out when the horse was reaching the correct number of hoof taps, and he would stop. The owner wasn’t attempting a fraud, and Hans was exceptionally intelligent. But his calculations were a hoax.

In last week’s Rosneft share sale — the deal President Vladimir Putin has called the biggest privatization in Russia, and also the biggest oil sector sell-off in the world this year — clever Igor, like clever Hans, has proved his indubitable intelligence. But the arithmetic which the president has announced — €10.5 billion paid into the Russian state budget – is a hoax. That’s because a curtain has been drawn across all questions of where the money has come from.

In fact, Kremlin and Russian banking sources acknowledge, the money originated from the Central Bank of Russia, recycled through the Russian state banks to Rosneft and back, and finally concealed inside secret fiduciary agreements with a consortium of Glencore, the Swiss trading company, and the Qatar Investment Authority (QIA), an Arabian Gulf state agency. The agreements appear to make Glencore and QIA the owners of a 19.5% shareholding in Rosneft – when they are fiduciary shareholders – and that’s not the same thing as owners.

“The transaction has been financed by money creation by the Central Bank”, said a source close to the dealmakers. “The Central Bank can’t simply print money and give it to the federal budget. So this deal was engineered for Glencore and the Qataris to appear to be buying shares when the terms of the agreement reward them for acting as fiduciaries, but ensure they cannot vote the shares without instruction from the Russian state; that’s Mr Sechin. This means the privatization of the shares isn’t genuine. Also, three-quarters of the money going into the state budget is coming from the Central Bank.”

A Russian banker in London comments: “There’s a golden rule in Russian banking. If you fiddle around, never involve foreigners because in the end they will expose you. The announced terms of the Rosneft deal cannot stand the light of day. Inevitably, the truth will come out.” According to Swiss sources, the truth has already been demanded by the US Government of the Swiss Government, which will obtain the contracts from Glencore.

Until the start of this month, the Russian government held 69.5% of Rosneft through a wholly owned state enterprise called Rosneftegaz. British Petroleum (BP) owned 19.75%, and the National Settlement Depository, 10.36%.

When Putin met Sechin on December 7 to announce the privatization sale of a 19.5% shareholding in Rosneft, it was pats on the back all round.

Source: Kremlin, December 7, http://en.kremlin.ru/events/president/news/53431

“[PUTIN]. Mr Sechin, I would like to congratulate you on the conclusion of a privatisation deal to sell a large stake in our leading oil and gas company Rosneft: 19.5 percent. The deal was made on an upward trend in the price of oil and it therefore reflects on the value of the company itself. In this respect, the timing is very good and the overall value of the deal is significant: 10.5 billion euros…I very much hope that new investors – a consortium of the Qatar state fund and Glencore, a major international trading company – I hope that their participation in managing bodies will improve corporate procedure and the company’s transparency and will ultimately increase its capitalisation. Meanwhile, the company’s controlling stake will remain in the hands of the Russian state: over 50 percent. Overall, this is a very good result. I would like to congratulate all of you, your colleagues who have worked on it. And naturally, the question arises: when will the money come to the Russian budget?”

“[SECHIN]. This amounts to over 1 trillion rubles, which will come to the budget, including 10.5 billion euros for Rosneft’s 19.5 percent stake. The consortium that will become Rosneft’s shareholder was established by the Qatar Sovereign Wealth Fund and Glencore trading company, which is our long-standing partner. The consortium participants hold equal stakes: 50 percent each. Payment to the state budget will be made both with our own resources and with a loan organised by one of Europe’s largest banks…Overall, the privatisation of 49 percent of Rosneft in a series of transactions has earned us $30 billion, no, nearly $34 billion, which is four times more than returns from all other privatisation transactions in Russia’s oil and gas sector.”

“I am sure that the high standards of our investors and Rosneft’s transition to a new dividend payment system, which the Government has approved at 35 percent, will definitely improve the company’s capitalisation, including the state-owned stake. We estimate the state-owned stake after the transaction at approximately 80 billion rubles…Also, I would like to say that we received the necessary amount of assistance from the Government while preparing the deal.”

“[PUTIN]. The budget must receive the full sum in the ruble equivalent, in rubles.”

The London market, where Rosneft is listed, was not persuaded by the valuation of the 19.5% shareholding. By conversion of €10.5 billion into US dollars on the deal day, December 7 — $11.13 billion – the transaction figure turns out to be $300 million less than the market capitalization of Rosneft the day before at $11.43 billion. Glencore and QIA got themselves a 3% bargain.

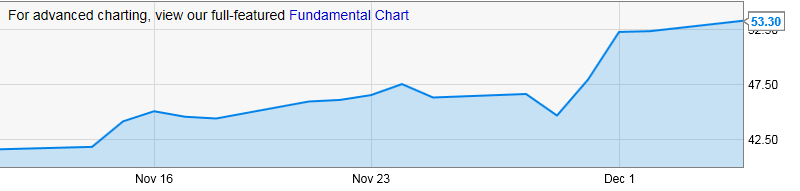

ONE-YEAR TRAJECTORY FOR ROSNEFT SHARE PRICE

Source: https://www.bloomberg.com/quote/ROSN:LI The market capitalization of Rosneft on December 7 was $58.6 billion.

The pickup in the Rosneft share price since has followed the rise of the crude oil price. That has helped enhance the subsequent gain in the value of the foreign consortium’s side of the deal. The market value of Glencore’s and QIA’s 9.75% stakes on December 7 was $5.7 billion apiece. With the rise in Rosneft’s share price by December 13, their stakes are now worth $6.8 billion. That’s a profit of $1.1 billion to Glencore and the same to QIA. That is, if and when the terms of their agreements with Rosneft allow them to cash out on market terms.

ONE-MONTH TRAJECTORY OF THE BRENT OIL PRICE

Source: https://ycharts.com/indicators/brent_crude_oil_spot_price

Rosneft’s announcement of the terms of the transaction express the value of the 19.5% stake sale to the state budget as Rb710.8 billion. At the Russian Central Bank rate of the day, this was equivalent to $11.12 billion; €10.4 billion.

Rosneft also claimed: “The acquisition of the Rosneft stake will be financed with investors’ own funds and will also involve debt financing. Investors’ equity in the acquiring vehicle will amount to EUR2.8 bn. The bulk of debt financing will be provided by Banca Intesa Sanpaolo that will arrange financing to the acquiring vehicle on non-recourse basis with a pledge of the acquired shares. Additionally, Glencore’s equity exposure on its investment in Rosneft shares will be reduced to EUR300 mn with full indemnity to Glencore’s balance sheet on other potential liabilities to the acquisition vehicle as through structured risk reduction instruments.”

The reference to Banca Intesa Sanpaolo has not been verified by the Italian bank, whose headquarters are in Turin (right). On December 2 the bank announced it was about to start a “transparency exercise” under supervision by the European Banking Authority. On December 12 the bank said it had agreed to grant credit lines of €750 million to the Yamal liquefied natural gas project of Novatek, to enable it to build a liquefaction plant with Italian-supplied equipment. In between these releases the bank said nothing at all about lending money to Rosneft.

whose headquarters are in Turin (right). On December 2 the bank announced it was about to start a “transparency exercise” under supervision by the European Banking Authority. On December 12 the bank said it had agreed to grant credit lines of €750 million to the Yamal liquefied natural gas project of Novatek, to enable it to build a liquefaction plant with Italian-supplied equipment. In between these releases the bank said nothing at all about lending money to Rosneft.

An international bank source said the Italian bank cannot finance Rosneft under the current US and European Union sanction rules, and it isn’t lending money to the shareholding deal as announced. “They don’t violate the sanctions,” the source said. “They don’t finance Rosneft.” A similar statement was issued by the bank a year ago.

If Rosneft meant the Italian bank is arranging for other banks to lend to Glencore and QIA, that isn’t what Glencore’s account of the transaction says. Click to read the Glencore version. According to Glencore, it and QIA “will commit €2.5 billion in equity to the Consortium with the balance [€7.7 billion, 76% of total] of the consideration for the acquisition of the Shares to be provided by non-recourse bank financing, principally [sic] by Intesa Sanpaolo S.pA., with Russian banks also providing financing and credit support [sic].”

The implication is that Intesa has agreed to lend Glencore and QIA more than half (“principally”) of the €7.7 billion ($8.2 billion) required by Rosneft. In its corporate and investment banking loan book which the bank reported on September 30 at €97.6 billion, such a loan would amount to between 4% and 8% of the bank’s entire book. With shareholder equity in the bank reported at the same time to be €48.9 billion, the purported Rosneft loan may amount to 10% or more of equity. European bankers say they don’t believe it.

Instead, Russian banking sources are convinced by the evidence they have seen that Russian state banks, backed by the Central Bank (right), are the principal financiers of the Rosneft share sale. According to one source, “Rosneft issued bonds. Those bonds were purchased by Russian banks on credit lines from the Central Bank. Rosneft then transferred its bond sale proceeds to the same banks, and they gave this money to the so- called investment fund of Qatar and Glencore to buy shares of Rosneft. Very nice combination.”

that Russian state banks, backed by the Central Bank (right), are the principal financiers of the Rosneft share sale. According to one source, “Rosneft issued bonds. Those bonds were purchased by Russian banks on credit lines from the Central Bank. Rosneft then transferred its bond sale proceeds to the same banks, and they gave this money to the so- called investment fund of Qatar and Glencore to buy shares of Rosneft. Very nice combination.”

The source is referring to the late-November bond transaction, reported by Reuters from a Rosneft briefing this way. “Nov 24. Russia’s largest oil producer Rosneft is to return to the country’s domestic bond market after a two-year absence with a programme worth 1.071 trillion roubles ($16.6 billion), the company said on Thursday. Rosneft, which is preparing to buy 19.5 percent of its own shares from the state in a share buyback deal worth around 700 billion roubles, said that the money raised from the bonds might be used for overseas projects, new upstream business and planned refinancing. A Rosneft source said the company has no plans to use bond proceeds to finance the potential share purchase from its parent company, the state energy holding Rosneftegaz. Rosneftegaz holds a 69.5 percent stake in Rosneft. ‘There is no intention, no goal to use funds any other way (than for overseas projects, new upstream business and planned refinancing),’ the source said. A Rosneft spokesman declined to comment.”

Mikhail Leontyev (lead image, left), Rosneft’s chief spokesman, doesn’t answer sensitive questions, and the company source quoted in the Reuters report was either mistaken or misleading. A Rosneft insider says the terms of the sale to Glencore and QIA have been kept secret from many senior company officials. According to Leontyev, “I have nothing to add… We have not given commitments to comment on the [transaction details] online, we’re not exhibitionists.” Is the transaction an intermediate one, allowing Rosneft to buy the shares back again? “That’s kind of absurd,” Leontyev claimed this morning. “That’s another achievement of morbid fantasies, which are generally subject already, in my opinion, to some kind of clinical diagnosis. Political or medical.”

In the outcome, however, Russian and international bankers believe the bond proceeds are the principal source of the privatization deal. A source close to the dealmakers explains: “Putin told Sechin to get more money out of Rosneft and into the budget to reduce the deficit. So the idea was to sell shares. But noone in the market wanted to buy something too small to represent even a blocking stake. The Russian oligarchs all refused because they don’t have the money. If Sechin came back to Putin with state bank financing, then the deal would obviously look fake, and simply move cash from one state pocket to another. Rosneft’s oil traders like Trafigura were asked for the cash as pre-financing for oil, but they said no. So in the end the Central Bank created the money through the bond financing, and then guaranteed the state banks’ role in the privatization. That has been camouflaged by the appearance of Glencore and QIA. Putin and Sechin wanted to prove the money came from the outside, so Glencore and QIA were persuaded with hefty rewards to act as fronts. Anything you can’t make transparent, though, is a mistake. And Sechin has compounded the mistake by making such a victory celebration of something that isn’t what it seems.”

“Such a scheme would achieve that desired purpose,” a Moscow banker comments. “It might make sense, but this is guessing. It is indeed a non-transparent deal, and what has been disclosed is not its entire financial mechanism. There may be good reasons for that. No doubt the US authorities will go after the identified deal parties one by one, and harass them. But there is the strong smell that funds of Russian origin can be involved.” The source adds the Central Bank doesn’t disclose its counter-parties in loan transactions, and will not report anything to substantiate its role last week.

A US business publication claims it was told by a Russian government source “the bond issue was a safety net in case the negotiations with the outside investors fell through.”

The Qataris needed reassurance for a case of the jitters which came on after the US Government reacted with private hostility. On December 13, Putin telephoned the Emir of Qatar, Sheikh Tamim bin Hamad Al Thani, to discuss “bilateral relations. Specifically, they emphasised the importance of the recent agreement by the Qatar Investment Authority to buy a 19.5 percent stake in Rosneft together with Swiss oil trader Glencore.”

Putin with Al Thani at the Kremlin, January 18, 2016

In Washington outgoing US Government officials have been biting their tongues. Amos Hochstein, the State Department’s envoy for international energy affairs, told Bloomberg: “Clearly this is not what we were hoping for when we implemented sanctions.” The departing White House spokesman, Josh Earnest, said: “ The experts at the Department of Treasury that are responsible for constructing and enforcing the sanctions regime will carefully look at a transaction like this. They’ll look at the terms of the deal and evaluate what impact sanctions would have on it.”

“There’s been too much of a victory celebration”, a New York bank source said of the Rosneft leaks to the Russian press, and of the Russian propaganda organs in English. “Another blow to Western sanctions and a vote of confidence in Russia’s economy,” claimed The Duran. “Russia has pulled off another coup.”

Swiss sources concede that US Government officials are concerned at the appearance that “under their noses the sanctions-busting specialist Glencore pulled off an €11 billion deal”, and that unless they act, the deal will encourage others. “The point is”, according to a Geneva source, “when the Swiss give Washington the Glencore contracts, as they are certain to do, the Americans will see this is a Russian bank financing for Rosneft and the state budget, not a foreign one.”

Russian sources say they suspect Sechin of making concessions to Glencore which will end up in five years costing the Russian budget more money than Sechin told Putin he is paying in now. Russian press reporting has identified tax relief for some of Rosneft’s oilfields to be likely to cost up to $1 billion in annual budget revenues foregone. By proposing to pay out 35% of its profit as dividends, instead of 25%, Rosneft is promising Glencore and QIA a takeaway that may be more than $1 billion richer by the year than would otherwise have remained in state coffers.

Glencore’s deal announcement also reveals that Sechin has given Ivan Glasenberg (right),  Glencore’s chief executive, a “new 5 year offtake agreement with Rosneft representing a sizeable additional 220,000 bbls/day for the Glencore Marketing business.” While Russian bank analysts of the oil trade have estimated that the trade commission has been $1 per barrel, trade sources claim Glencore will now take $3 per barrel. “An insider from Rusal, the state aluminium company, acknowledges that in return for financing Rusal through its near-collapse into bankruptcy in 2008-2009, Glencore took a substantially higher commission than Rusal had ever wanted to concede before. The Glencore terms were also a violation of the company charter, as a successful legal challenge by Victor Vekselberg proved. For details, read this.

Glencore’s chief executive, a “new 5 year offtake agreement with Rosneft representing a sizeable additional 220,000 bbls/day for the Glencore Marketing business.” While Russian bank analysts of the oil trade have estimated that the trade commission has been $1 per barrel, trade sources claim Glencore will now take $3 per barrel. “An insider from Rusal, the state aluminium company, acknowledges that in return for financing Rusal through its near-collapse into bankruptcy in 2008-2009, Glencore took a substantially higher commission than Rusal had ever wanted to concede before. The Glencore terms were also a violation of the company charter, as a successful legal challenge by Victor Vekselberg proved. For details, read this.

A calculation of the value of the new Sechin-Glasenberg oil trading concession looks like this: 220,000 bbls/day x $3 per barrel x 365 days x 5 years = $1.205 billion. Glencore does not respond to questions about its trading commissions, and the calculation may err on the low side. If the normal Rosneft trading commission had been $1 per barrel, this would earn $401.5 million over five years. The difference between $1 and $3 would be $1.05 billion minus $401.5million; that is, $648.5 million.

According to Glencore’s deal announcement, “Glencore and QIA have concluded various agreements which provide for the establishment of a 50:50 consortium.” These agreements, several European sources believe, include a fiduciary scheme which keeps ownership of the 19.5% shareholding under Sechin’s control, but allows Glencore and QIA to act as shareholders with tight restrictions. “They appear as the holders of the shares but vote as instructed by Sechin in the fiduciary agreement,” one of the sources believes. “In five years, these shares may come back to him. They may be entitled to keep the dividends over this period, or they may be required to return part or all of them.”

Sechin is currently suing in a Moscow court the RBC media group for reporting last April that he intended to impose such restrictions on Rosneft share sales, in order to prevent BP, with 19.75%, combining with a foreign shareholder to form a blocking stake.

“The foreigners play a superficial role [in the deal]”, said a knowledgeable source who concedes he is speculating now, but will know for certain shortly. “Putin would not know what the structures are. He would just be told the budget is getting €10.5 billion. He would not be told what the outgoings will be.” Sources who know Sechin and other senior Rosneft executives say the Glencore oil trade concession “sounds like a provident fund. For an outlay of €300 million Glencore is going to make much more in annual dividends so long as the oil price stays stable above $50; and much more again from its trading commissions.”

Leave a Reply