By John Helmer, Moscow

@bears_with

The Belgians like to speak of themselves as the victims when the great powers of Europe go to war. They were when the Germans invaded in 1914 and 1940.

But since 2014 when the Belgian government has been repeating it is gung-ho for the war with Russia, there has been no Russian attack, no occupation. Instead, there has been the amicable Russia-Belgium diamond trade worth more than $30 billion in annual exports and imports, supplied by the Russian state diamond company Alrosa.

If Belgian officials cut that trade off by agreeing to the European Union (EU) sanctions banning Russian diamond imports, as proposed by other EU states, that would liquidate ten thousand diamond polishing and related jobs concentrated in Antwerp, and destroy the country’s fifth largest export business forever. Alrosa would move its diamonds to Dubai, killing Antwerp as a diamond trading and cutting centre, just as Amsterdam as a diamond centre was killed by the German occupation of 1940. Antwerp took advantage of Amsterdam’s misfortune in 1946. Dubai will now do the same.

This is what Belgian government and diamond industry officials mean when they say they favour the toughest possible sanctions on Russian gas exports to Europe – but no sanctions on Russian diamonds. This is what Prime Minister Alexander De Croo meant when he told an Antwerp conference of diamantaires on September 14: “Sanctions should focus more on the aggressor than ourselves.”

Earlier, reacting to an attack on the diamond trade with Russia by Ukrainian President Vladimir Zelensky in a speech to the Belgian parliament, the spokesman for the Antwerp World Diamond Centre (AWDC) said: “Not only are thousands of jobs in Antwerp at stake in the short term, but this decision will inevitably lead to a worldwide shift in the diamond trade in the long term. As long as international policy-makers worldwide do not adopt a unanimous position to sanction Russian diamonds in their entirety, Antwerp will be the only place that will bear the consequences of an EU sanction.”

By “worldwide shift” he meant Dubai.

De Croo has camouflaged Belgium’s resistance by repeating he will not veto a Russian diamond ban if there is “overwhelming support” for it in the EU. So a majority of the EU states have continued pressing; they are led by Poland. In March of this year, De Croo announced: “I would like to officially state that our country has never hindered any measures regarding diamonds. Our country did not interfere in this issue.” In private, however, De Croo has been casting Belgium’s veto.

The Poles have been attacking De Croo, pressing the case for an EU ban on Russian diamond imports as payback for De Croo’s insistence on imposing EU budget sanctions against the Warsaw government last year. De Croo is also refusing to accept Ukraine’s demand for accelerated membership of the EU and of NATO, and for fresh EU funding to pay Kiev’s war-fighting bills.

Instead, he has just announced €8 million in non-lethal aid to Kiev. “Ukraine can keep on counting on Belgium,” De Croo declared. “More than words, there are actions. Once again, Belgium is responding to concrete needs and will be providing essential equipment to Ukraine in the coming weeks.” The equipment is first-aid kits and pharmaceuticals produced by Belgian companies.

This week the secret Belgian veto campaign appears to have succeeded. The new draft of the eighth round of EU sanctions includes dental floss and deodorants; it leaves out diamonds. This omission is expected to be confirmed publicly on Friday of this week at the EU summit meeting in Prague.

“At the moment, diamonds are not included on the agenda for the next round of sanctions,” announced Tom Neys, the AWDC spokesman. “But things change quickly. [On] Friday [October 7] they will finalize discussions, and the EU [leaders decide] on October 6 and 7. The fact that sanctions also create other ethical problems, and that these sanctions will have no effect in Russia, are probably important elements in these debates. Now is the time to focus on international solutions.”

By “international solutions” the Belgians mean keeping Dubai from taking over Antwerp’s diamond business.

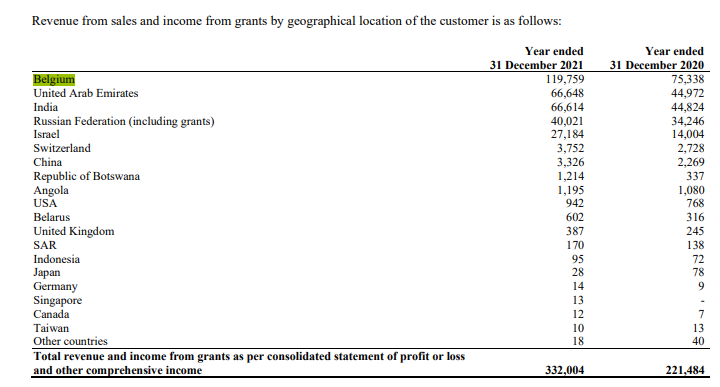

The Belgian diamond trade is worth about $37 billion annually in exports and imports. Diamonds polished in Antwerp and exported to the rest of the world are the country’s fifth largest export. These figures vary sharply from source to source, but according to Alrosa, the company’s exports to Antwerp last year amounted to 36% of its total sales revenues, far ahead of Dubai and India. The figure was up 60% on the year before.

Figures are in millions of roubles. The exchange rate adopted in the Alrosa report was Rb74.3 to the US dollar. The revenue figure for Belgium equates to $1.6 billion. Other company and Belgian data indicate a value iof more than $4 billion. Source: http://old.alrosa.ru/, before the pandemic, the sales revenue figure for Belgium was $100.4 million; that amounted to 42% of Alrosa’s export value. See: http://old.alrosa.ru/ Dubai was worth much less then; Israel much more. As the war has escalated, the Jewish diamantaires of Israel have been losing business to the Arabs and Indians who dominate the diamond exchange in Dubai. If Antwerp is lost to its Jewish diamantaires, the Arab and Indian takeover will be complete.

In 2015 this is how the EU’s sanctions war against Russia started to threaten the Belgian diamond industry.

For the following seven years, as the war has intensified, the Belgian government under Charles Michel (2014-2019), then De Croo for the past two years, has combined fighting with feinting, enabling the trade to recover from the loss of demand and revenues during the pandemic years, and preserving the Russian diamond business after the start of the Special Military Operation in February. This is how the schemes of work-around and parallel trade have worked quite profitably for everyone involved.

Left: Prime Minister Alexander De Croo. Right: Charles Michel meeting President Vladimir Putin in Moscow on January 31, 2018. Michel was the Belgian Prime Minister at the time. “History has known good and not so good moments in relations between Europe and Russia,” he told Putin. “However, since we are neighbours, we will always work together. Michel became President of the European Council in 2019; since then he and Putin have held 12 telephone conversations, the most recent three calls since the beginning of the military operation; every one of them was initiated by Putin. Michel has kept significantly better relations with the Kremlin than the German, Ursula von der Leyen, the European Commission President, or Josep Borrell, the Spanish foreign representative of the Commission.

The archive on Alrosa can be followed here. It is a detailed and long one because since 1994 I was the Russia correspondent for the diamond media in the US, UK, Israel, Botswana, South Africa, and Canada.

The US Treasury commenced its sanctions against Alrosa by including it in the debt and equity restrictions of February 24 of this year. Washington then attacked the company directly on April 22, declaring “these sanctions will continue to apply pressure to key entities that enable and fund Russia’s unprovoked war against Ukraine…These actions, taken with the Department of State and in coordination with our allies and partners, reflect our continued effort to restrict the Kremlin’s access to assets, resources, and sectors of the economy that are essential to supplying and financing Putin’s brutality.” . The privatization of Alrosa has created a free float of 34% of its shares; 33% are held by the Russian government; 25% by the Sakha republic (Yakutia) where most of Russia’s diamonds are mined; and 8% divided between the districts of Sakha where the mines are located. At the time of the US attack, the company had already been sanctioned by Canada, the United Kingdom, New Zealand, and the Bahamas.

Sergei S. Ivanov, Alrosa chief executive since 2017, was personally sanctioned by the US on February 24; he is the surviving son of the senior Kremlin official and former defence minister, Sergei B. Ivanov.

Until that point – until the launch of the Special Military Operation — the company had been reporting optimistically on its prospects for profiting from the recovery of the global diamond market after the impact of the lockdown in China and loss of demand in the US jewellery market.

The market outlook for 2022 — the company reported on March 2 but composed weeks before the military operation began — was for strong demand chasing a decline in supply and causing diamond prices to jump. “In 2021 diamond jewelry hit a new all-time record level reaching $84 bn due to strong consumers activity in all key markets notably in USA and China. Retailers report strong sales in 2021, cite continued positive sentiment from consumers. Cutters and polishers enjoy strong demand for polished, healthy profitability, improved balance sheet. Though in 2022 availability of rough diamonds is their key concern. Miners exhausted diamonds stocks in 9M’21, starting from H2’21 supply comes from production only. Global diamonds production in 2022 to reach 110-120 m cts, a 15-20% drop vs 2021 total rough diamond demand… In 2021 ALROSA diamond prices grew +33% from Jan’21 through Dec’21. Diamond prices will be playing an important role in fixing rough diamond shortage amidst healthy diamond jewelry demand.”

Alrosa said it was not expecting US or EU sanctions against the diamond trade. “No further diamonds supply upside risks are expected.” In a postscript attached to the company’s audited financial report for 2021 it said: “A number of sanctions have been announced to restrict Russian entities from having access to the Euro and US$ financial markets including removing access to the international SWIFT system and in such a situation this could further complicate the Group’s ability to transfer or receive funds. Though it is not possible for management to predict with any degree of certainty the impact of all this uncertainty on the future operations of the Group, the Group continues to run business as usual, and service its obligations.”

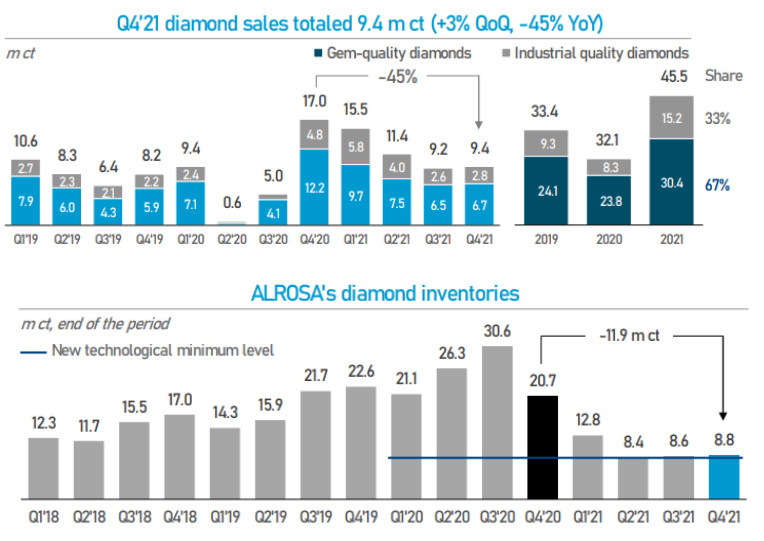

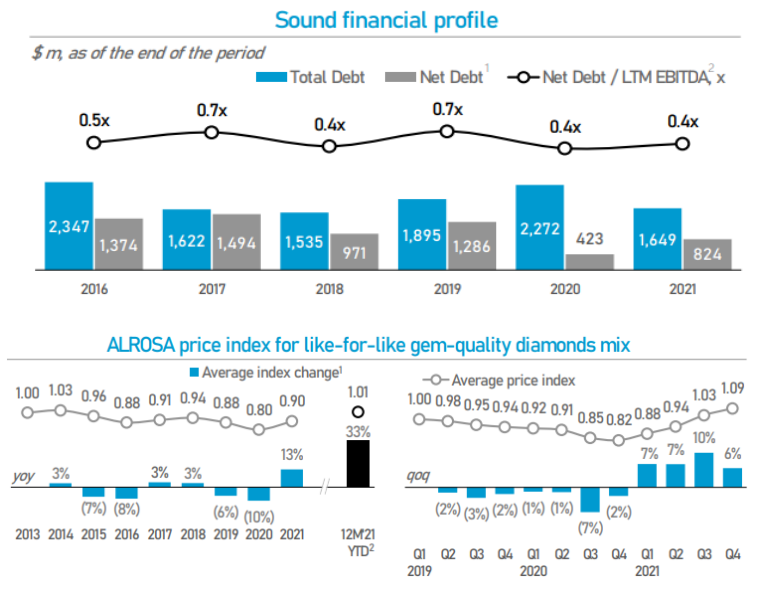

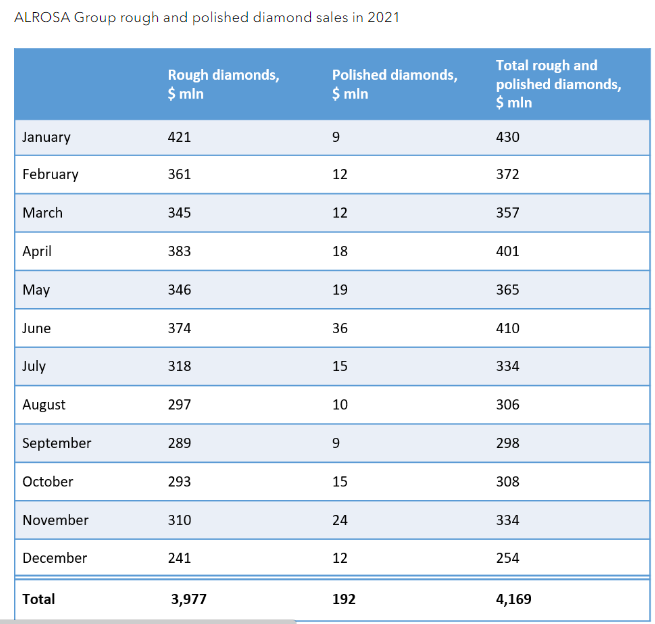

These tables from Alrosa’s March 2022 presentation illustrate the recovery of sales in 2021, not only compared to the pandemic year of 2020, but to the sales result in 2019. Diamond stocks fell sharply as demand in the biggest of the diamond-consuming markets, China and the US, pushed Alrosa’s exports upward. Earnings (Ebitda) grew, and the company debt declined. Before the US acted to sanction Alrosa, the company was already gaining in profit from higher diamond sale prices due to burgeoning consumer demand and shrinking stocks. Between 2020 and 2021, recorded profit tripled in value.

Source: https://alrosa.ru/

Source: https://alrosa.ru/

By comparison, De Beers, the main international rival for Alrosa, has reported diamond sales of $4.04 billion in 2019, $2.8 billion in 2020; $4.8 billion in 2021.

The immediate effect of the US sanctions, and the Polish effort to strike with EU sanctions, has been to further restrict supplies to the market, and push prices up higher and faster. The company has announced that it is converting its sales and repayment of bond coupons to roubles or rupees. It has also halted public disclosure of its production and sales results, and inventory levels. The war has returned Alrosa into the secrecy in which it operated in 1994.

Rapnet, the diamond industry price setter in New York and Israel, is reporting: “While the sanctions on Russian goods have not yet caused notable polished scarcities, shortages are likely in the coming months. Rough supply has dropped since Alrosa canceled its March and April sales. Prices at rough auctions have increased — particularly in the small-diamond category, which Alrosa dominates. De Beers raised prices of small rough at its latest sight from June 6 to 10.”

“The market is splitting into two segments: Russian and non-Russian goods. Some big cutters are finding ways to buy Alrosa rough in order to serve centers that remain open to buying Russian-origin polished. These diamonds will likely sell at a discount to non-sanctioned ones. US and European jewelers and brands may have difficulty filling their sourcing requirements in the coming months without Russian supply. This will lend further support to diamond prices.”

“For manufacturers, the biggest factor in the downturn was a sharp drop in demand in China, which still maintains restrictions related to Covid-19. Given the quarantine requirements for arriving foreigners, suppliers do not want to visit the country, and Chinese buyers do not travel abroad. The same applies to Hong Kong, although the precautions there are not so strict and are gradually being relaxed. China’s retail sector has also slowed. A recent update provided by the two largest jewelry companies in the region, Chow Tai Fook and Luk Fook, showed that their sales at comparable stores in mainland China for the quarter ended June 30 [2022] fell by 19% and 28%, respectively. As a result, these large buyers have significantly reduced their orders.”

“Indian suppliers, of course, are closely watching the United States, the largest market for them, amid all the talk about recession and inflation. But even though they report a general drop in orders, the US remains a stable market, even if trade in this country does not match last year’s level. U.S. retail trade weakened as Signet Jewelers, the country’s largest specialty jewelry company, lowered its annual forecast. According to Rapaport reports, the company expects revenue of $1.75 billion in the second quarter of the fiscal year ended July 31, which is 2.1% less than last year.”

“In July, we saw a decline in sales as our customers were increasingly impacted by rapidly rising inflation, so we are revising our targets to match these trends,” CEO Gina Drosos said in early August. Major diamond producers are concerned about a drop in orders from the United States in the current quarter. But the US continues to support the market, and there is some hope that it will stabilize by the holiday season.”

On September 17, Bloomberg reported that the parallel diamond trade was “fracturing the global trade that stretches from cutting factories in Mumbai to luxury stores on New York’s Fifth Avenue…Many in the industry refuse to deal in Russian gems following the invasion of Ukraine and after mining giant Alrosa PJSC was hit with US sanctions. But there’s a handful of Indian and Belgian buyers who are snapping up large volumes at lucrative terms, getting to pick and choose the diamonds they need while others stay away. The deals are happening quietly, even for the famously secretive diamond world. And while they’re not breaching sanctions, there are other risks to consider — heavyweights like Tiffany & Co. and Signet Jewelers Ltd. don’t want Russian diamonds that were mined since the war began, and suppliers say they are worried about losing crucial contracts by dealing in Alrosa gems.”

Vladimir Malakhov, editor of the Russian diamond industry bible, Rough-Polished.com, was asked how much had sanctions affected the export of Russian diamonds; what gain in market share De Beers had made at Alrosa’s expense; and how the parallel trade schemes were operating to compensate. “Unfortunately,” he replied, “I do not comment on what is happening in the industry.” Read more in the publication. No Russian analyst covering the diamond industry, Alrosa and De Beers will talk at the moment, on or off the record.

“There seem to be quite a few errors in the Bloomberg article about Russia, India and the diamond market generally,” responded a leading international diamantaire. Israeli and American diamond industry sources acknowledge that they have been anticipating that Alrosa would continue selling through Dubai and resist the price discounting pressure from India. The problem is, however, that the banks financing the trade in India, the United Arab Emirates, and Hong Kong, as well as in Antwerp, have come under US pressure to stop or risk losing much more of their business than their diamond financing.

In Vienna, a source acknowledges that “a major Austrian bank of dubious repute, which used to handle a lot of Russian diamond transfers, stopped completely a few months ago.” A Chinese source adds: “No one wants to bank through Hong Kong any more for obvious reasons. Only Indian banks manage to arrange some payments, and India direct seems to be the only outlet for Russian rough.”

In the short term this means that in what was already a market in which demand was weakening, rough prices falling for three months in a row, the sanctions war has put a floor under prices to prevent them falling further; that was expected if more Russian diamonds had been arriving on Alrosa’s plan before April. “Obviously,” comments a South African source, “De Beers is taking advantage of the situation and filling the gaps where they can, and where the market allows.”

In Moscow open source reports indicate that in the month of July diamond imports to India increased by 25% by value, compared to the same month of 2021; for the April-July period, the Indian imports were up 4.5% on 2021. In August Indian imports of rough were up by 12.5% year on year.

Russian diamond export data are now a black hole, and will remain that way. There have been reports from Indian diamantaires that there is a continuing flow of Russian rough into Surat, the Indian diamond cutting centre, though the volume is lower than before February; the price is not discounted. In comments to the press at the Eastern Economic Forum in Vladivostok last month, Alrosa CEO Ivanov (right) said there has been no decision to cut this year’s mine production target of 34 to 35 million

carats nor next year’s production target; no discounting of Alrosa’s export sale prices; and no decision to stockpile unsold diamonds at the state stockpile agency Gokhran in Moscow.

Left, Sergei Ivanov of Alrosa; right, Ahmed bin Sulayem of the Dubai Multi Commodities Centre.

While the Belgians keep trying to talk out of both sides of their mouths, the last word has been said by Ahmed bin Sulayem, the chief executive of the Dubai Multi Commodities Centre. Rejecting Zelensky’s attack on Antwerp, and also “cheap comment” by Belgian diamond industry officials on Dubai, he told Rough & Polished in Moscow: “Twenty years of diamond transparency in Belgium includes a long list of challenges and systemic failures ranging from the Monstrey Case, to the conviction of felon, Agim De Bruycker, a former commissioner of the Antwerp Federal Judicial Police and head of its Diamond Squad. It should also be obvious that if any action is ultimately enforced by the European Commission, it has not and will not be because Dubai lobbied for it to be so.”

“In the same way that sanctions may not have the intended consequences on Russia, neither do ill-informed comments or false media narratives help to protect industries or jobs. Ultimately, healthy competition is fundamental to any industry as a driver for innovation, lower prices as well as higher quality goods and services, however, greater benefits can be found in ’coopetition’, where industry-specific economies work together to create higher standards that benefit the entire supply chain, while remaining resource efficient. While I may not agree with all of Mr. Neys [Antwerp diamond industry spokesman] comments, I agree that sanctions on Belgium’s diamond industry would be ‘a mistake of historic proportions’ and it is my wish for Antwerp to return to full strength and join in not only providing a competitive market, but working with Dubai to drive positive change for the industry’s wider benefit.”

Leave a Reply