By John Helmer, Moscow

In Kiev on Sunday, Ukrainian President Petro Poroshenko complained that he isn’t getting cash from the International Monetary Fund (IMF) fast enough. Christine Lagarde, the IMF’s managing director, told him to stick to the Fund conditions, but she also promised to go soft on whether the IMF will stop the money if Ukraine decides not to repay the $3 billion bond owed for repayment to Russia in December.

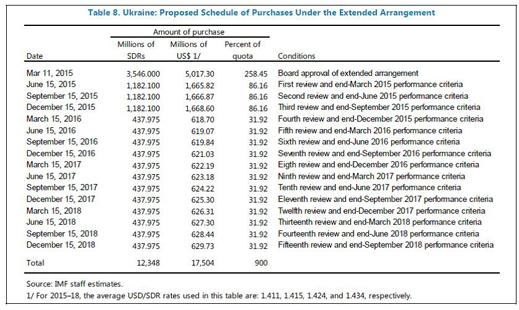

“So far, we have received only 38 percent of the total funds earmarked [for Ukraine] under the Fund’s program,” Poroshenko claimed at a press conference following the round of meetings with the IMF delegation. “We have agreed on a strict schedule,” he added, referring to the first two payments the IMF has transferred to Kiev, totalling $6.7 billion so far, in what is being called the Extended Fund Facility (EFF); this replaced last year’s aborted Stand-By Agreement (SBA). The Ukrainian president implied he wants to go faster than the IMF schedule, published in August, allows.

Source: http://www.imf.org/external/pubs/ft/scr/2015/cr15218.pdf -- page 41

The Fund schedule provides for the next payment to Kiev of $1.7 billion on September 15, after the IMF staff complete their assessment of the Ukrainian government’s compliance with the “performance criteria” as of end-June.

In fact, according to Poroshenko, the timing has slipped; there will be no Fund payment this month; and he doesn’t like it. “The IMF mission is due to arrive in September and will work here until October 2, and we have agreed that after its work is done it may present its offers at a meeting of the IMF board of directors as early as in October.” That is an admission that there won’t be fresh cash this month, and maybe not until October, or November.

The assembled reporters from the Financial Times, Wall Street Journal and Bloomberg failed to detect the slippage, so noone asked why.

Lagarde, accompanied by her spokesman Gerry Rice, released a statement congratulating the officials she had met – Poroshenko, Prime Minister Arseny Yatseniuk, National Bank of Ukraine (NBU) Governor Valeria Gontareva, Finance Minister Natalie Jaresko, and Economic Development Minister Aivaras Abromavičius. Lagarde paid “a tribute to the courageous work of the Ukrainian authorities. Policies are on the right track and have started to yield results. The fiscal position is getting stronger, the foreign exchange market has stabilized, and the banking sector is being repaired so that banks are sounder and can start to provide credit again. The recent debt restructuring agreement is a vital complement to economic reforms, and an essential step toward creating fiscal space, external sustainability, and improved confidence.”

Prime Minister Yatseniuk held a solo session on Sunday with Lagarde

Lagarde added: “an independent and capable anti-corruption agency with broad powers has been launched.”

At the press conference noone asked what that line meant for the Ukrainian court proceedings now under way in which at least $1.8 billion in IMF “emergency liquidity assistance” (ELA) to the National Bank of Ukraine has disappeared through Privatbank and related-party accounts offshore. Ukrainian investigators and reporters claim local prosecutors and the anti-corruption agency refuse to open a formal case against the bank or its control shareholder, Igor Kolomoisky. For that story, read this.

Poroshenko and Lagarde were asked what they mean by the “recent debt restructuring agreement”. In that deal, announced on August 27 between Jaresko and commercial holders of Ukraine government bonds, the creditors insisted on, and got, significantly more for their paper than the IMF had advised Kiev to concede. The terms provide a 20% “haircut” or reduction for Ukrainian government repayment of $8.9 billion in commercially held sovereign bonds. That’s just $1.8 billion – far less than the western media have been reporting from the script issued by the Ukrainian Finance Ministry.

The face value of the commercial bonds comes to less than half the $19.3 billion aggregate which the IMF calculates Ukraine must repay in sovereign obligations. The short-term “haircut”, which has been announced, and the extension of time to repay have been offset in the longer term by an increase in the coupon interest rate, plus a bonus (that’s to say, a wager) tied to a Ukrainian economic growth target.

The IMF has been calculating that about $15 billion in debt repayment cuts are required to meet the capacity to repay conditions of the EFF How the small commercial bond deal will impact on the IMF calculations of Kiev’s capacity to repay the bigger number has not been explained in the IMF staff documents released so far.

Russian Finance Ministry statements have consistently repeated the position that repayment of the $3 billion bond issued to the Ukrainian government for two years from December 2013 is an official, or government-to-government obligation, not a commercial one; and it is not negotiable with the private, mostly American bondholders – Franklin Templeton, TCW and T. Rowe Price. For more, read this. Finance Minister Anton Siluanov (below, left) responded to the August 27 announcement of the commercial bondholder agreement by saying: “We won’t agree to a restructuring. We will insist the funds are returned in full in December.”

Russian tactics for dealing with the IMF loans to Ukraine, as they have been discussed at the inter-government level on the IMF board, is that there will be no Russian objection to the EFF, nor even to the conversion of IMF loan money to spending on the war in eastern Ukraine. In return, the extra flow of Fund cash must also be spent, among other things, on repaying the Russian bond in December, as well as Ukrainian debts for gas deliveries by Gazprom.

“If this is the Russian government calculation, it’s foolhardy”, comments an international banker who was directly involved in restructuring talks following the Argentine and other government defaults. “What must happen before the Kremlin puts the Finance Ministry on a war-footing? It’s folly not to realize that the old rules of international debt workout between governments will not be applied to Russia.”

On Sunday Poroshenko told the IMF he means not to repay the $3 billion owed on the Russian bond. That is a commercial debt, not a government debt, he is claiming.“Under no circumstances Ukraine will provide any benefits to the Russian loan. The Russian side had all the facilities needed to join the negotiations, we were open to express our positions. The talks [on debt restructuring with the creditors’ committee] have been held, there is no and will be no default. Russia should decide before the end of the year…whether it goes with commercial creditors or it holds a separate position…when it decides, Ukraine will also define its position.”

The IMF has said its lending rules and the EFF loan conditions for Ukraine allow the Fund to keep supplying Kiev with cash even if the commercial bond reduction falls far short of the “performance criteria”. The rules don’t allow IMF lending to continue if Ukraine defaults on a government obligation. That’s the rub for the Russian bond.

Lagarde ought to have corrected Poroshenko when he made the Russian obligation look like a commercial one. Instead, she ducked, saying the decision is for the country directors and control shareholders of the Fund to make on how to designate the Russian bond, and whether the rulebook can be rewritten. “It is up to the [IMF] board to determine the characterisation of one bond or the other and I think it will be for the board to decide.” Personally, she implied, she is going along with Poroshenko. “It is really up to all creditors to take advantage of [this] debt restructuring … We believe it is a very good arrangement … We doubt very much that anything better could have been obtained.” By all creditors, Lagarde meant Russia — not the IMF, the World Bank, the US, or the European Union.

As for Poroshenko’s request to hurry up with the cash, Lagarde was more cautious: “What’s critically important is to restore confidence…and to deliver on the promises that have been made, to stay within the parameters of what has been agreed.”

Lagarde’s remark on junking the Russian bond was impromptu – it wasn’t in the draft press release Jerome Vacher was carrying in a briefcase, as he trailed behind the managing director and the president. Vacher is the IMF’s resident representative in Kiev.

Source: https://www.youtube.com/watch?v=LzBSxVci6sc

According to Lagarde’s official statement to the press, “the recent debt restructuring agreement is…an essential step toward creating fiscal space, external sustainability, and improved confidence.”

Vacher was out of sight when Lagarde met Poroshenko. Later, he and spokesman Rice were seated on Lagarde’s left when Poroshenko was joined by other Ukrainian officials.

Source: https://www.youtube.com/watch?v=LzBSxVci6sc

Covering up for political and financial favouritism for individual Ukrainian oligarchs and their banks has been charged against Vacher and Rice. They refuse to respond to the evidence. For more on their violations of the IMF Code of Conduct for Staff, click here. Following publication of this report, the IMF’s chief of media relations, Simonetta Nardin, removed photographs of her political partisanship from the internet.

A response has followed from the US Department of Justice (DOJ), after a spokesman for the Department confirmed an investigation of the IMF money trail through the Ukraine banking system and offshore. Anna Iemelianova, a Foreign Service National Legal Specialist, according to DOJ records, said she had been misidentified in photographs of her and Mary Butler attending official meetings in Ukraine. She requested a correction. According to an intramural awards announcement from DOJ’s Criminal Division last December, Iemelianova has received a Certificate of Appreciation for the significant contributions she has made in her work on Ukraine.

Leave a Reply