By John Helmer, Moscow

You don’t have to be Mr Plod to suspect that Noddy isn’t playing fair.

More than half the Canadians who hold shares in High River Gold (HRG:CN), and who have resisted Alexei Mordashov’s buyout offers in the past, think he’s low-balling them again. Having driven up the share price to C$1.43, three cents over Mordashov’s latest offer price for his takeover of HRG, the sentiment in the share market is against Mordashov. Or is it?

On July 18 Nordgold (NORD:LI), which already owns about 75% of HRG, announced that it wants to buy the rest. Nordgold is listed on the London Stock Exchange; HRG on the Toronto Exchange. The former has a market capitalization of US$1.71 billion after listing in Moscow and London between December 2011 and January 2012. Since then it has lost more than 60% of its value.

Share price trajectory for Nordgold, January-July 2012:

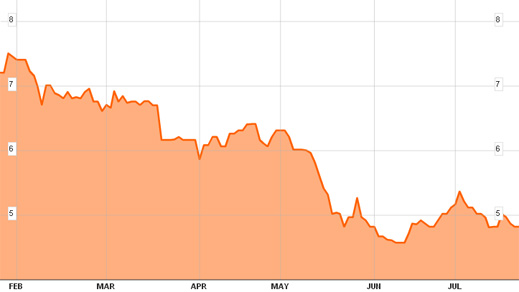

By contrast, over the same period of time HRG has preserved its value, starting at C$1.24 in January and ending at C$1.23 at the start of last week, before Mordashov made his move. The market cap of HRG on July 17 was C$1.03 billion (US$984 million).

Share price trajectory for High River Gold, January-July 2012:

The buyout offer is addressed to the “Minority Shareholders of High River Gold Mines Ltd… Nordgold currently owns 630,627,472 High River shares, constituting approximately 75 percent of High River. Under the terms of the proposed offer, eligible High River shareholders will have the right to elect to receive either: (i) 0.285 (the “Exchange Ratio”) Nordgold global depositary receipts (“GDRs”) for each High River share held by them (the “GDR Offer”); or (ii) C$1.40 in cash for each High River share held by them (the “Cash Alternative”, together with the GDR Offer the “Offer”).

The GDR Offer represents a 17.2 percent premium based on Nordgold’s and High River’s respective closing share prices on July 17, 2012, the last trading day before this announcement, a 20.2 percent premium based on Nordgold’s and High River’s respective one month average share prices for the period ended July 17, 2012, and a 30.6 percent premium based on Nordgold’s and High River’s respective three month average share prices for the period ended July 17, 2012.”

“At Nordgold’s closing share price on July 17, 2012, the GDR Offer values High River at approximately US$1.2 billion, or approximately 58 percent of the value of the fully consolidated Nordgold. Nordgold has executed lock-up agreements with a number of substantial High River minority shareholders, including three of the largest shareholders, as well as with former members of High River executive management, under which they have all agreed to tender their High River shares and accept the GDR Offer. The aggregate number of High River shares subject to the lock-ups is 58,050,206, which represents approximately 28 percent of the High River shares not already owned by Nordgold and its affiliates.”

A buyout offer from Mordashov has long been anticipated in the London and Toronto markets. Analysts who follow the two stocks believe that Nordgold has been the more under-valued of the two; among the reasons for this is the public case the HRG minorities have made that Mordashov is toxic for their company and for their valuation of HRG’s fair share price. The story of Mordashov’s fight with the HRG minorities over the past three years can be followed here.

The current position can be described arithmetically this way: there are a total of 840 million HRG shares on issue. Mordashov through Nordgold and other companies owns 631 million (75%). That leaves 209 million – and they are the target of the July 18 offer. Of this aggregate, the Nordgold announcement claims that 58 million have been pledged to Mordashov for conversion to shares of Nordgold.

If true, that would leave 151 million, or 18%. There are reports from the Canadian minority shareholders that they have lined up pledges for at least 110 million shares (13%) to be voted against the Mordashov offer. If that too is true, then the fate of the takeover now depends on what the holders of the remaining 51 million (6%) will decide. According to the Canadian stock exchange rules, once Mordashov can demonstrate he owns 90% or more of the share – that’s 756 million—he can proceed with a mandatory buyout, and the resistance is at an end.

The Nordgold announcement claims that the owners of the 58 million shares to be swapped for Nordgold shares include “three of the largest shareholders”. Asked to verify this by identifying who they are, the spokesman for Nordgold in Moscow, Sergei Loktionov, responded: “Unfortunately, we cannot identify the shareholders of HRG and their shares (of course, except those under the control of the company Nordgold). Also, we do not disclose exactly what shareholders have agreed to sign the Lock-up Agreement. So you’d better refer the matter to the shareholders.”

The bellwether of the resisting minorities has been Sprott Asset Management of Toronto, run by Eric Sprott. Moscow Investors in HRG believe he may hold as many as 50 million of the so-far uncommitted shares. Sprott isn’t announcing publicly where he stands towards Mordashov, except that according to sources in Moscow, he believes Mordashov’s earlier buyout offers were too low to be acceptable.

The bellwether of the resisting minorities has been Sprott Asset Management of Toronto, run by Eric Sprott. Moscow Investors in HRG believe he may hold as many as 50 million of the so-far uncommitted shares. Sprott isn’t announcing publicly where he stands towards Mordashov, except that according to sources in Moscow, he believes Mordashov’s earlier buyout offers were too low to be acceptable.

The Canadian minorities with smaller stakes continue to believe that Mordashov’s offer is still too low, and that if they succeed in barring him from crossing the 90% threshold, he is likely to do what he’s done before – extend the time for the offer acceptance, and sweeten the offer price by another 10 cents to 20 cents.

What makes the buyout terms different this time around, according to one Moscow investor in HRG, is that the current market price for Nordgold is so low, there appears to be more upside gain in betting the price will go up than there may be in betting on HRG’s upside. “Nordgold should be worth more – between $4 billion and $5billion”, the source calculates. “The discount is Mordashov. But the institutions holding HRG shares may be calculating now that this is the right time to swap and capitalize on the value gap between the two companies.”

Russian minority shareholders agree with the Canadian resisters that distrust of Mordashov remains now, as it has been for the past three years, the reason for the low share price. But can he buy himself out of the penalty box? At least one investment banker in Moscow thinks so. “This is the clearest case in Russian metals and mining,” he believes, “of an oligarch creating value for minority investors. Taking mismanaged crap and turning it around, lifting the operating metrics and free cash flows, developing reasonable investment strategy. And then buying out the minorities at a higher value – yes, in self-interest because he needs the cash pile at HRG and he needs to lift the free float of NORD.”

The Canadian resisters will launch their counter-attack on these points later this week. But according to the Moscow banker, “[the resisters] don’t understand the stock would be stuck back in the 20-30 percent range without [Mordashov]. Ungrateful bastards – I wish them the best of luck.”

The Nordgold announcement has called on HRG to commission an independent valuer to produce an opinion on the fairness of Mordashov’s offer. Once that is ready, it is to be included in the terms of offer to be mailed out to the minority shareholders. They will then have 35 days to say yea or nay.

Leave a Reply