By John Helmer, Moscow

Are they real teeth in the tiger’s mouth, or are they falsies?

This is the question which shareholders of two Canadian-listed junior goldmining companies have been asking since the two companies, both apparently controlled by Russian mining entrepreneur Maxim Finsky (image), proposed an all-share merger on the basis of valuation of assets buried in the wilds of eastern Siberia.

On March 14, here is what White Tiger Gold (WTG:CN)) and Century Mining (CMM:CN), both Toronto Stock Exchange listed, said they have agreed to do: “Under the terms of the Business Combination, shareholders of Century will receive 0.40 of a White Tiger common share for each common share of Century held. The board of directors of each company has unanimously approved the Business Combination.” A break-fee penalty of C$13.5 million was accepted by Century if its board opts for a better deal; or if Deutsche Bank London refuses to accept the deal. Deutsche Bank is the principal financier of Century’s operations through a US$33 million advance to buy Century’s future gold production.

Press reports of the merger deal claimed its combined value was C$743 million, based on the share trading for the two stocks. At the time of the announcement, WTG’s 114 million shares had a total market capitalization of $371 million. The week before the deal announcement, WTG was at $485 million, before selling ahead of the merger cut $114 million off its value.

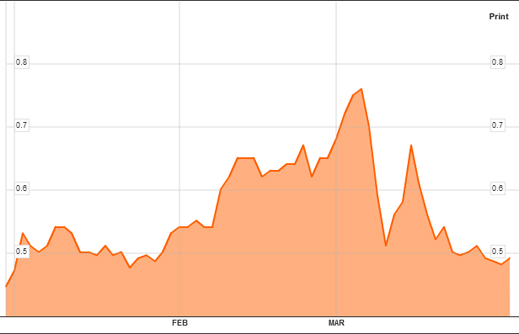

WTG’s THREE-MONTH SHARE PRICE TRAJECTORY

Century Mining has 408 million shares on issue; on March 14, the WTG offer fixed its value at C$273 million. Just a few days earlier, its share price was much higher, and its market cap $306 million. The combination took $33 million off CMM’s value, adding up to a combined loss of market value of $147 million.

CMM’S THREE-MONTH SHARE PRICE TRAJECTORY

The market apparently doubted that WTG was the bigger of the two miners, so the collapse of both share prices ended up bringing the two closer together. Still, WTG remained with the higher value. Asked who provided the expertise to calculate this during the merger negotiations, Cowley of WTG said “[the valuation ratio] was agreed by independent committees of both companies. [They] are a group of people not in the public domain.” He added that the committees were advised by Moelis & Company of New York and Blair Franklin of Toronto. Moelis reports that last year it won The Banker Magazine’s award for “most innovative boutique”. Blair Franklin reports its motto as “At all times our primary interest is: What is in our client’s best interest?”

At Blair Franklin, Ben Mandell has been identified as the advisor to Century Mining for the merger deal. He has yet to respond to the question of how he calculated the valuation ratio for the share swap.

The facts on the ground look a little different from the announced valuations According to the only documented valuation WTG has so far presented publicly, a technical report by the Micon consultancy known in Canadian parlance as NI43-101, WTG’s only operational mine, Savkino in the Trans-Baikal region, started this year with 125,471 oz of gold reserves. By the year 2017, when mine life will be over, Micon reports it will be capable of producing a cumulative total 103,266 oz, at an average cash cost of $678 per oz, generate free cashflow of $9.1 million. Net income over the entire project, according to Micon, would be just $6.9 million.

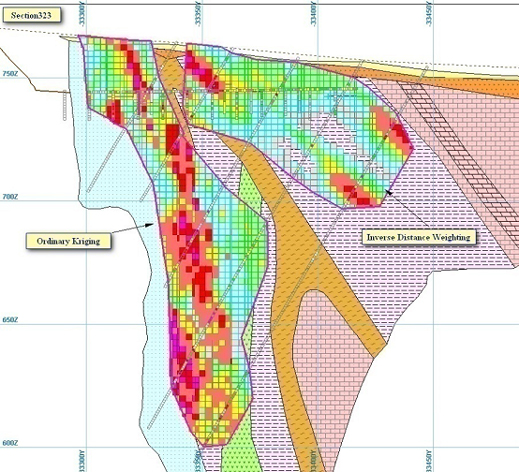

Micon’s calculations are based on projective modelling of data from this survey map of the Savkino deposit:

Cross-Section of the Savkino mine, Ildikangold Block Model, NI-43-101 page 61

The Micon analysis, dated November 22 and posted on the Canadian market repository website SEDAR on December 29, says this mine produced 7,507 oz in 2009; 24,434 oz in 2010. It is possible Micon’s estimate for production in 2010 was not realized, because WTG chief executive Geoffrey Cowley said this week he estimates his company’s production last year at “between 13,000 and 14,000 ounces.” This, he confirmed, was entirely from the Savkino mine.

In the same period, Century has reported producing 19,224 ozs at its San Juan, Peru, goldmine, and 14,419 ozs at its Lamaque, Quebec, making a total of 33,643 ozs, or at least 38% more than WTG; possibly two and a half times more. In 2012, Century claims to be targeting annual gold production of 130,000 oz for Lamaque and San Juan combined. By contrast, WTG’s best hope, according to Micon’s analysis, is for output of 22,184 oz, one-sixth the volume of Century.

In their reserves count, Century’s Lamaque claims proven and probable reserves of 1.14 million oz, grading at 4.56 grams per tonne, with a mine life of at least 11 years. Century’s San Juan mine claims 186,316 proven and probable reserves, grading 8.87 g/t, with a mine life of 7 years. Savkino can do no better than a reserves count at present of 125,471 oz, grading 1.29 g/t, and a mine life of 7 years. On these indicators, WTG is about ten times smaller than Century.

The financial reports of Century, issued quarterly, indicate that in the nine months to September 30 last, gold sale revenues came to $16.2 million; costs of production were $10.8 million, and there was an operating profit of $5.4 million, before the bottom-line, after depreciation, tax, and other charges, turned into a net loss of $4 million.

WTG’s predecessor company, SL Resources, also listed in Toronto, reported that as of September 30 last, it held cash of $27,370 and had liabilities of $49,032. Financially, it was dwarfed by Century Mining, and was not a mine-operating company at all.

WTG did not come into existence in its present form until last December. More of how that happened shortly. No financial report from WTG was available at the time of the takeover bid for Century, but the first report was released on March 31. This indicates sales revenue (almost entirely earned from gold sales) of C$20 million; cost of sales, $12.6 million; operating profit, $7.4 million; and a bottom-line loss for the year of $665,000. Comparing these results item for item with Century Mining’s 9-month report, WTG cannot claim to be the bigger of the two mining companies.

WTG reversed into SL Resources in December within days of a Russian company called LLC UK Dalsvetmet (DZM — never mind the name, it is registered in Russia) agreeing to move SL Resources from Canadian registration to the British Virgin Islands, changing its name to WTG, and merging by reverse takeover with Dalsvetmet. On December 16, from an office in Tortola, WTG announced it had obtained conditional approval to sell shares in Toronto. From the negligible assets which SL Resources held, WTG now claimed the underlying value of “four wholly-owned subsidiaries of DZM and DZM’s entire 80% interest in a fifth subsidiary.”

These subsidiaries are licence holders for the Savkino mine and gold prospecting licences elsewhere in the Russian Fareast. A search of the Russian press and internet archives for these subsidiaries and their licence areas indicates rich promises, poor results. In 2008, at the time the first gold was poured at Savkino, the company claimed it would be producing 850 kgs (27,328 oz) of gold in 2009. The actual result, according to Micon, was less than half. The company also claimed reserves amounting to 190,000 oz. When Micon reviewed the data, it could not find one in five of those ounces.

In October of 2009, Dalsvetmet said it would produce almost 13,000 oz that year; according to Micon, it fell short and produced just 12,255 oz. In 2010, the company forecast production of more than 32,000 oz – the actual outcome was less than half as much. The gold reserve claim, counting Savkino and other exploration prospects, added up to 870,000 oz, according to the published claims.

In November of 2009, Finsky identified himself as the owner of Dalsvetmet and told Vedomosti, a Moscow business newspaper, that he intended to sell shares of his company in a Hong Kong or Shanghai Stock Exchange listing. He said “offers from Chinese investors to purchase shares are received continuously”, totaling, he claimed, $150 million. He also claimed that his partners were two Canadians, Fran Scola and Margaret Kent. Scola appears as a member of the Century Mining board which voted for the WTG merger. Kent was chief executive of Century Mining until she was replaced in July of 2010 by Daniel Major.

Richard Meschke, vice president for legal and corporate development at Century, said today that Finsky is the controlling shareholder of the company with a stake of about 30%, which he started accumulating in 2009. Finsky himself claimed in his November 2009 newspaper interview that he owned 40% of the company, with Scola and Kent owning the rest. The China stock sale never materialized.

Instead of raising the interest of Chinese investors, Finsky has raised the ire of minority shareholders of Century Mining. They charge that he used his power at Century to encourage the market to cut the share price ahead of the mid-March merger deal, and thereby favour WTG in the share swap, while retaining control of the expanded company. Cowley was asked to comment. “I am not prepared to respond to criticism by Century Mining shareholders. They will have their shareholders’meeting on May 12. Presumably, they will have an opportunity to discuss [these questions].”

But what is WTG worth? In Russian practice, mining companies are obliged to submit their reserves and resources counts to the State Reserves Committee and Rosnedra, the state mine licensing agency. Cowley was asked whether WTG had done this, and if so, what are the officially authorized reserve counts for Savkino and the prospecting areas, if any. Cowley said he wasn’t sure. “I have to check. I’m sure we do.” Asked what the proven and probable reserves are for Savkino, he said: “I don’t have [them] in front of me.” He claimed the full data were issued in the Micon report of December 29 posted on SEDAR. The report does not refer to official Russian state reserve estimates.

The State Reserves Committee declines to answer press questions. Rosnedra was asked to say whether Savkino had applied for and been granted an official reserve figure. The agency did not reply.

Cowley explained that when WTG’s shares were offered for sale in their debut listing on December 31 on the Toronto exchange, “a very small amount of retail shares” were sold. There was no prospectus for the sale, he added, “because it was a private placement”. What he means is that between converting SL Resources and Dalsvetmet into WTG, and the share sale of December 31, Finsky arranged for WTG to sell 24.8 million shares for a total of $24.8 million to what a company release called “various international investors”.

Wth this sale of 22% of the total issue, a share price was fixed of $1. Since the company has reported that Finsky owned 85 million of the shares (74%), that appears to have left just 4 million for sale on the stock exchange – just 4%. Who ran up the share price to buy these shares, Cowley was asked . He said he doesn’t know; the company has announced it knows of no material circumstances warranting the share price movement. Cowley acknowledged only that Finsky is the controlling shareholder, and that the investors in the private placement “are locked in until April 30.”

Finsky has a controversial reputation in the Russian mining industry. Reportedly a friend since childhood of Mikhail Prokhorov, he worked for him at Norilsk Nickel and was employed to buy gold assets which were later spun off into a separate mining concern, Polyus Gold. An executive at another Russian mining group says Finsky over-paid for the assets; in at least one case, Lenzoloto, more than $100 million of initial outlay was written off the Polyus Gold books a year after the acquisition.

During Prokhorov’s fight to oust former partner Vladimir Potanin from Polyus Gold in 2008, Finsky headed a further spinoff company called Intergeo. Potanin’s group charged this was improperly spiriting assets out of Polyus Gold.

From an initial price of US$26 cents per share at the merger of Dalsvetmet with SL Resources on November 11, just before the combination took the name of WTG, Finsky saw the price jump to $1 in the private placement of mid-December, and then to $6.67 in the first week of January, 2011. Cowley admitted that very few shares were actually traded. “We had no control and we had no significant idea of why the price shot up.” One analyst has reported that “given that Mr. Finsky owns on the order of 74% of White Tiger Gold shares, I would argue that a fair market price for White Tiger Gold does not exist.”

Finsky, who maintains a Moscow office as chief executive of Intergeo and a seat on the Polyus Gold board of directors, did not respond to a request for his comment.

Leave a Reply