By John Helmer, Moscow

The share price of United Company Rusal, the Russian state aluminium monopoly, has again dropped below the three-dollar (Hong Kong) level, and is heading towards oblivion – that’s the Citi Bank forecast of HK$1.80. In London and Moscow the market calculation is that, despite the company’s announced cuts to production of aluminium, Rusal’s second-quarter sales, revenues, costs, profit and loss to be released shortly, will reveal a worsening picture.

Just how much worse the share price can get Rusal insiders realize at Moscow headquarters. That’s because they say that a very large volume of metal Rusal has produced, reported as exported and sold, is stocked in a warehouse beside the Baltic Sea. Only this aluminium hasn’t really been sold – it has been hidden by Rusal and its chief trader, Glencore. A company source said the number is so secret that only chief executive Oleg Deripaska (image right), Glencore chief executive and Rusal board member Ivan Glasenberg (left), and a handful of others know it.

Last month at Rusal’s request, New York lawyers for Citi issued a copyright violation notice, trying to suppress circulation of Citi’s oblivion forecast. But in a subsequent interview the bank’s London-based aluminium analyst Jatinder Goel insists that “nothing has changed. This [$1.80] is still the TP [target price].” His analysis suggests the size of Rusal’s debt is now larger than the value of its equity, while its cashflow is drying up. If there were to be significant negative changes in the Citi estimates of aluminium price, Rusal sales, stocks, and the premium Rusal claims to be getting for direct metal deliveries to customers, the company risks insolvency. According to the New York lawyers, Georges Nahitchevansky and Kristin Garris, “Citigroup is one of the world’s leading financial institutions… Our client invested a significant amount of time and effort creating and developing its proprietary CR reports.” There can be no doubting the reliability of Citi’s forecast for Rusal’s future.

The company reported that in the first quarter it managed to cut its output of primary aluminium by 4% (42,000 tonnes) compared to the first quarter of 2012, or by 3% (31,000 tonnes) compared to the fourth quarter of 2012 . This, according to the Rusal operating report, “was mostly attributable to the decreased production at certain less efficient smelters located in European part of Russia and Urals.”

Moscow analysts to whom Rusal has confided preliminary production and sales data for the second quarter are divided between those who believe Rusal’s second-quarter results will show a flat line and those who expect a declining one on the key indicators. One analyst says that “volumes will remain about the same [level], that is, there will be no significant changes.” The downward shift in the aluminium spot price, he added, may have been offset by an increase in the premium which aluminium buyers pay to receive Rusal metal without warehouse delivery delays. Nonetheless, according to this source, Rusal’s earnings (Ebitda) may drop from $200 million to $100 million.

Other Moscow analysts are forecasting a flat line – no change in volume of production, sales tonnage, or reported sales revenues.

Rusal insiders warn that volume numbers for production and sales are misleading because they believe Rusal is shipping its metal to an Estonian warehouse complex where it is counted as sold; in fact, the sources allege, it is being withheld from the market in order to stop the trading price for the metal falling further.

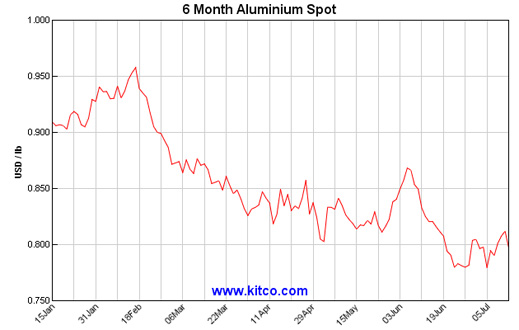

So far this year, the price of aluminium (3-month mean, month of June) is down 12% from January, according to the London Metals Exchange (LME) figures. The current LME cash spot price is $1,765 per tonne. The Kitco chart shows the downward trajectory expressed in US cents per pound for 6-month spot.

Source: http://www.kitconet.com

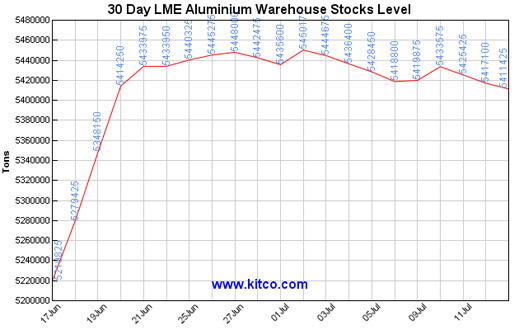

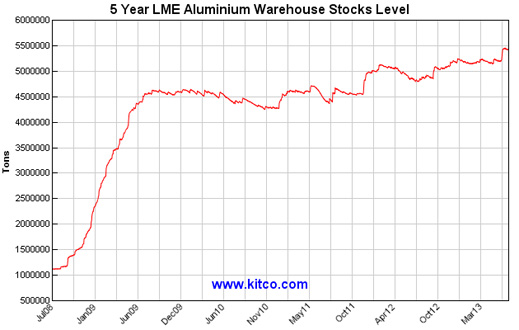

Threatening these prices, and thus Rusal’s future revenues, according to the official data of the LME, today’s unsold stockpile of metal is enormous — 5.41 million tonnes. Kitco illustrates in these two tables how the warehouse stock level of aluminium has been heading steadily upwards since the global trade collapse of 2008.

Source: http://www.kitcometals.com

However, the LME stock data refer only to aluminium in the LME’s approved and monitored warehouses, principally those in Rotterdam and Detroit. Take a close look at this list, and you will see that no warehouse has been authorized either in Russia or in Estonia. Rusal keeps unsold inventories on its balance-sheet in Russian warehouses, and reports them. As aluminium prices fall, Rusal must report a reduction in value for these stocks.

In the first quarter this year, Rusal claims that “as a result of weaker aluminium demand and a growth in warehouse stocks, the regional duty-unpaid premium for primary aluminium ingots declined in February and March from USD210-233 per tonne to USD200-215 per tonne.” Also, the shrinking value of unsold stocks is a known quantity. In its annual report for 2012, Rusal reports its inventory position at Note 21.

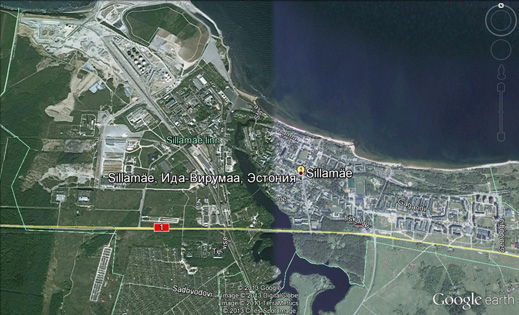

But a Rusal source, together with an Estonian source close to Glencore, have revealed there is a large, unreported Rusal stockpile of unsold aluminium at a complex at the Estonian seaside town of Sillamae.

Another source who declined to be identified confirms that the complex is owned and operated by a company called Silmet. Ostensibly engaged in the mining and trade of rare metals, with a 90-year history of Swedish, German, and Soviet occupation, Silmet acknowledges that its high-security warehouses are being used to stock aluminium. The capacity there is several hundred thousand tonnes; that’s at least 10% of the official LME count. If Rusal’s hidden stockpile in Estonia were to be added to the global stockpile, the number would be stratospheric. A Silmet source says the company’s aluminium stocking capacity is a commercial secret.

Here’s a bird’s-eye view of Rusal’s latest secret to surface.

This is not the first time that Rusal schemes have been discovered for making production, exports and sales revenues appear to be more closely matched than they really are. In 2004 an investigation by a trade consultancy in London discovered anomalies in the volumes of primary aluminium traded by Rual, a trader associated with the group, and Wainfleet Consultadores, a company reported to be doing business in Madeira, Portugal. Further investigation by the Moscow-based Aluminy Consultancy in 2007 and by the European Commission cast doubt on the reliability of the match between production volumes and sales tonnage and revenues.

Also problematic for Rusal is the proposed change in the international warehousing rules for aluminium. For the rule change, planned to take effect early in 2014, threatens to cut the premium in the price Rusal claims to receive for its shipments. According to Rusal’s first-quarter 2013 report, “the decrease in average LME aluminium prices was slightly offset by a 60.0% growth in premiums above the LME price in the different geographical segments (to an average of USD264 per tonne from USD165 per tonne for the three months ended 31 March 2013 and 2012, respectively).”

A report this month by the Financial Times credits the takeover of the LME by the Hong Kong Stock Exchange company, six weeks ago, with forcing a reduction in warehouse delays in shipping out aluminium once sold. “ ‘Premiums have to come down,’ says one senior trader. ‘We’ve essentially taken out a bid from the market.’ The immediate effect would be to put pressure on aluminium producers such as Rusal, Chalco, Rio Tinto and Alcoa, already struggling with low aluminium prices… The second order effects of the change in rules are less easy to predict. The prospect of falling premiums may make banks and traders less willing to buy aluminium for so-called ‘financing deals’ – potentially putting additional downward pressure on prices.”

A report by Andrea Hotter of Dow Jones explains that warehousing schemes benefit aluminium producers who play the warehouses against the metal consumers in order to jack up the delivery premium. “ Traders, merchants and banks are using the warehouse system as a financing mechanism for various storage deals, cancelling tonnages and putting them into bonded warehouses when financially viable. Consumers are getting the worst deal because they can’t use the system for physical delivery… Consumers such as U.S. aluminum sheet maker Novelis and U.S. canmaker Coca-Cola Co (KO) have both complained to the LME, directly or indirectly. Coca-Cola told Dow Jones Newswires that it takes two weeks to get metal into warehouses and six months to get it out, and that the situation has been ‘organized artificially to drive premiums up.’ An even larger portion of those complaining are banks, merchants and traders who have warrants in warehouses that they can’t immediately get to. Producers don’t really care, because they are able to command higher premiums for their metal, although they continue to say that they sell to consumers and only supply parcels to the spot market as and when they have aluminum available.”

In practice, by concealing unsold aluminium in warehouses Rusal is trying to ensure that the LME warehouse system keeps the spot price from falling in line with demand, and supports the delivery premium for buyers who want on-time delivery. So the more metal which can be concealed in Estonia, or other places off the LME-approved map, the better for Rusal’s balance-sheet.

What will happen when the premium dwindles, though? One Moscow analyst is sanguine. “The new warehouse rules are being considered for introduction sometime in April 2014,” he says, “and they will be applicable only to the warehouses with a queue longer than 100 days. No doubt that premiums will fall from the current level; but since the realized price for the Western producers is LME plus premium, if the premium goes lower, we may either get more capacity reductions or the LME going slightly higher to offset some of the premium lost. My guess is that the effective realized price if and when new warehouse rules get introduced will not fall much.”

In Russia, for capacity reductions read job layoffs and social protests. As a Russian monopoly in which state shareholders exercise virtual control over the company’s revenues, as well as personal control over Deripaska, this is unacceptable. What will happen when the LME warehousing rules change and the premiums are cut, claim Rusal insiders, is that even larger volumes of production will be shipped into hiding in Estonia.

{kind=link}

Leave a Reply