By John Helmer in Moscow

Oleg Deripaska is preparing a series of presentations to institutional investors next week in Boston and New York, chaperoned by one of his largest creditor banks, BNP Paribas. Rarely has so unconvincing a lamb been led to market by so well-known a wolf; or such an odd couple asked to be believed for the sincerity of their hand-holding.

The prospectus released by United Company Rusal to the Hong Kong Stock Exchange on December 31 reveals that BNP Paribas’s affiliated banks are owed more than $415 million by Rusal; no other international bank appears to be owed a larger sum by Rusal than that.

In addition, there is more than $80 million which BNP Paris claims from another of Deripaska’s companies, but about which there has been a “dispute” and a “repayment shortfall” in connection with Deripaska’s abortive effort to take a stake in the North American auto parts firm, Magna. Less vaguely expressed, Deripaska appears to be in default to BNP Paribas on that one.

Then there are all the ways in which BNP Paribas has arranged to make fees out of managing Rusal’s billion-dollar debts to the syndicate of international lenders which BNP chairs and coordinates. BNP is listed as the bank in charge of enforcing the security of Rusal’s loan agreements with the syndicate. It is one of the principals in the “cornerstone placing agreements”, according to which the first listing of Rusal shares on January 27 was guaranteed. BNP’s motive is clear – it not only has Rusal debts to collect for itself, and for the larger syndicate, but it also holds additional fee warrants, claims and rights to Rusal shares whose price it wants badly to boost.

The purpose of BNP’s exercise in the US is to convince US investment fund managers and analysts of institutions holding Norilsk Nickel shares that they should vote in favour of Deripaska’s hostile takeover attempt against Norilsk Nickel. On October 21, at a planned extraordinary shareholder meeting called by Rusal, they are being asked to reverse their near-unanimous vote against this scheme when the annual general shareholders meeting of Norilsk Nickel was held on June 29.

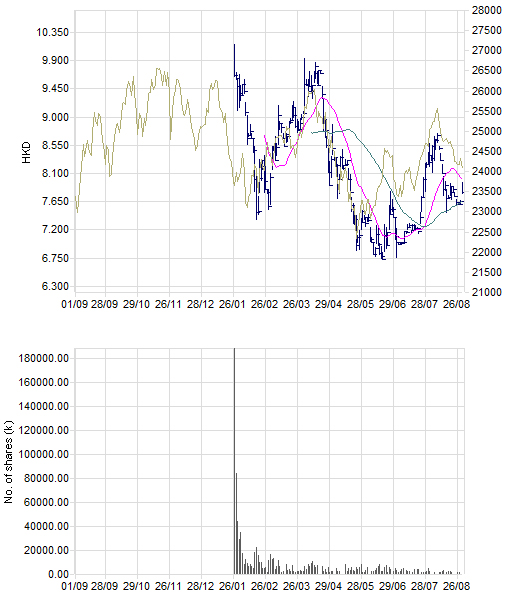

Additional presentations for the same purpose are planned by Rusal, BNP and another of its creditor banks and promoters, Credit Suisse, in London. The proposition that the Norilsk Nickel minority shareholders should embrace Deripaska’s hostile takeover effort has already been rejected in the open marketplace, and by none other than Rusal shareholders, since the company first started selling its shares in Hong Kong seven months ago. The vote of no-confidence is reflected in this share price chart:

What interviews with the fund managers in London, Hong Kong, and the US reveal is the churn rate, which isn’t disclosed in this highly volatile price line – that is the amount of short-term share buying and selling which is driven by wagers on the movement of the price of commodity aluminium. The unusually high churn rate for Rusal reported by these market experts means that few, if any, of the original January and February shareholders remain committed to the company and its chief executive, apart from those who have no choice – the Russian government banks VEB and Sberbank, which is securing the state monopoly of aluminium from bankruptcy; Nathaniel Rothschild and his father Jacob; and the other cornerstone investors – Robert Kuok, John Paulson, Li Ka-shing, and the Libyan Investment Authority.

So what has Deripaska to say now that might convince a market that has been deeply skeptical of Deripaska risk on its own, let alone adding it to Norilsk Nickel’s future?

Before anyone dares to answer that question outside the Boston and New York meeting-rooms, Rusal has engaged its old standby, the London libel law firm of Schillings, to threaten independent institutional analysts from publishing anything Deripaska considers unfavourable. Schillings has even begun applying its English strong-arm tactics against American institutions.

One of these recently received a warning letter after it had published a report on the Rusal takeover attempt. The report had speculated that Rusal might be told by the Kremlin to abandon the attempt against Norilsk Nickel, and sell out its 25% stake in the company. When the institution’s report cited investment community sentiment and institutional shareholders and their analysts as believing this might be a welcome development, and that Rusal’s exit from Norilsk Nickel would be positive for the latter’s share price, Schillings cried false, misleading and inaccurate reporting. Schillings then opened its Savile Row waistcoat to reveal a little English dagger, terming its right to sue Americans in the English courts “expressly reserved”.

That this Schillings threat isn’t taken seriously across the Atlantic reflects the rather bigger blade which threatens Deripaska — this week it was put on open display by the two most powerful decision-makers in Russia, Prime Minister Vladimir Putin and Deputy Prime Minister in charge of resource concessions, Igor Sechin. The occasion was their state visit to the plant, town, workers, and management of Norilsk Nickel.

When Deripaska’s aircraft had trouble getting airport clearance to land for this meeting, he decried his rival Norilsk Nickel shareholder, Vladimir Potanin, for a dirty trick. But land Deripaska eventually did – with this advance signal for all to see that it is the Kremlin which is running Norilsk Nickel, and that even local air-controllers aren’t afraid that Deripaska may become their boss.

For those fund managers who are about to receive visits from BNP and Rusal, it is no novelty to understand that in the management of Russia’s natural resource, mining and metal companies, the oligarchs with shareholding control are temporary concessionaires, with limited operating, earnings, tax and capital gains rights; and that it is the state which dictates terms and the sharing-out of rewards. Exactly how the sharing of these concession rewards has been arranged, including the debt bailouts Rusal and Norilsk Nickel received during the 2008 crisis, is widely understood in oligarch circles, but unprintable in a family newspaper. The operative rule, however, is that those officials who supervise the concessionaires swear to have no purpose but the welfare of the market, the workforce, and the Russian commonwealth – and no desire to intervene when the concessionaires fight each other. That is why Sechin, seated to Putin’s right during their meeting with shareholders and management, said: “The main shareholders will reconcile their positions. We don’t interfere in corporate processes. That’s the shareholders’ business.”

Understanding why the no-intervention disclaimers must be made, it follows that the methods of Kremlinology are required to decipher the real meaning of the intervention which Putin and Sechin have decided towards Deripaska and Potanin. Accordingly, Tuesday’s display indicates that timing and circumstance are not going as well for Deripaska as he will claim next week in North America.

| At his session with Norilsk Nickel workers, Putin was peppered with concerns about the Pikalevo analogy. This refers to June last year, when residents of the Leningrad region town of Pikalevo protested at the collapse of their livelihoods at the hands of the Deripaska group, which dominates the town’s alumina refinery. The trouble was settled by Putin appearing on national television to give Deripaska his marching orders. Since then Deripaska has clawed back much larger financial favours from the prime ministry, and dismissed the affair as a show for television. |  |

This time round Putin has been at pains to distinguish Deripaska’s conduct and the problems at Pikalevo from the takeover conflict at Norilsk Nickel. But the insistence of the questioning on the Pikalevo point was a round-1 win for the state official running Norilsk Nickel, Vladimir Strzhalkovsky, who has been publicly attacking Deripaska’s competence and ethics for months now. According to the transcript published by the prime ministry, the question for Putin was that since shareholders like Deripaska (explicitly named) have as their main purpose “to fill their own pockets, many people in Norilsk are worried about the current conflict between the main shareholders of Norilsk Nickel. I would like to ask you: Do you think how our employees are protected from the possible adverse effects of this conflict? And I hope that it will not be a Pikalevo scenario – I hope, and am confident in this. But can we count on the support of the Government of the country?”

Putin’s reply started with an explanation of how the conflict at Pikalevo was not comparable to the shareholder fight at Norilsk. But he implied that he agreed with the charge against Deripaska of filling his own pocket. “With regard to the [shareholder] conflict – yes, we see that it’s there. I tell you frankly: today it has not even been discussed. And in accordance with the law, we would not be there to intervene. But I’m on to something that has drawn attention.” At this point Putin referred to the proportion of profit which Norilsk Nickel and its international peers have distributed as dividends to shareholders. “Kazakhmys”, he said, “distributed 6.6%, Rio Tinto in my opinion, 18%; BHP, 38% plus something. The shareholders of Norilsk Nickel distributed as dividends 50% of the profits – the largest allocation [in the peer group]. I think that’s enough. You see, an order of magnitude greater than all the rest!” Implicit in this remark was condemnation by the prime minister of the attempt by Deripaska to get Norilsk Nickel to pay out in dividends more than it had earned last year – about 115%. That had been blocked by the unanimous opposition of the minority shareholders, Potanin, the management, and the board elected in June.

In short, Putin told the workers he expects to see reinvestment of profits for social purposes, and will not allow Rusal to extract cash from Norilsk Nickel if that would work to “the detriment of the company”. He also assured the workers that he had made his will plain to the shareholders. “Today we talked to them and about the resettlement program, and about environmental issues, and so on. I must give credit to shareholders, they are not greedy, not mean, not argumentative — all at once they agreed.”

Remarks by Putin during the management and shareholder session also suggested a win on points for Strzhalkovsky against Deripaska. Discussing the proposals from government ministries to raise more tax from Norilsk Nickel through a duty on nickel and copper exports, greater spending on environmental protection measures, and higher social benefits, Putin implied that the state wants to curb its payouts to the oligarchs’ profit line, and to increase budget revenues at their expense. Some Moscow brokerage analysts reacted that this might be negative for the share price. Others noted that the proposed tax would amount to less than 6% of prospective earnings — insignificant for the company’s financial performance.

But Putin’s emphasis on fiscal probity also implies his reluctance to endorse the large state bank loans which Deripaska would require, if he is make good on his takeover bid for Norilsk Nickel; or the cash stripping from Norilsk Nickel to pay down Rusal’s debts if Deripaska were to be allowed to take control. A Troika Dialog analyst, who has actively championed Rusal in recent reports, expressed his disappointment that “nothing groundbreaking was said during the meetings”; by that he meant “that UC RUSAL would lose more than others should the current status quo be maintained.”

The London news in the run-up to the October 21 shareholder vote at Norilsk Nickel isn’t going to Deripaska’s benefit either. The UK High Court will resume for the Michaelmas term on October 1, and a few days later, a hearing has been scheduled to decide when Deripaska goes on trial to defend the shareholding that currently gives him control of Rusal. The accumulation of new evidence files in court, and the judge’s ruling on the trial schedule, mark the progress Mikhail Chernoy (Michael Cherney), Deripaska’s former patron and shareholding partner, is making to adjudicate the suit for his share of Rusal, and of the dividends and profits Deripaska has taken for himself since the two men signed their trustee and shareholding agreement in March of 2001. The sum of Chernoy’s claim is more than $4 billion. That’s more than half the value of Deripaska’s stake in the company.

Leave a Reply