By John Helmer, Moscow

Diamonds are a bit like champagne: even in the worst of times, demand can grow among consumers, and for producers, sales revenues and profits too.

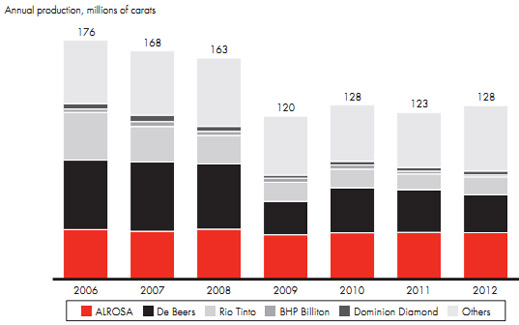

Good news isn’t usually the honey which attracts this particular bear; and Alrosa has been producing plenty of it. Released early this month, the company’s financial report for 2013 and operational report for the first quarter of 2014 show that production of rough stones is up, with higher grades for each tonne of ore and higher volumes of ore out of the company’s newest mines. Rough diamond prices are rising, so sales revenues grew at 11% last year, and are forecast to accelerate to 16% this year. Compared to its major global rivals, Alrosa has been able to maintain its output at the minehead, while the others – De Beers, Rio Tinto — have retreated, and BHP Billiton has left the business altogether.

With a 27% share (2012 data) of global production, Alrosa is the dominant diamond miner in the world. It is also catching up on De Beers’s share of the diamond sales market. According to the Bain consultancy study of 2013, Alrosa is also the most profitable diamond producer, with the largest operating-income margins per carat. The earnings margin, according to a report of Otkritie Capital issued on April 16, is forecast to rise from 41% last year to 43.2% in 2016. From an investment point of view, Alrosa is one of the best bets in the global diamond universe; it is also the best bet among Russia’s mining companies.

Source: http://www.bain.com/

Last month a whisper in Washington that Alrosa might become the target of US sanctions has been gagged by the rapid reaction of the New York, Antwerp, and Tel Aviv diamond traders. Their businesses would suffer if Alrosa’s annual output were to be consigned to a direct trade with India and China, or to the black market. As an Israeli dealer in Antwerp recently pointed out, “even if the Antwerp diamond centre avoids the fallout, Alrosa may seek to divert some of its supply to other destinations such as Mumbai, India. There are already signs that Alrosa is preparing itself for such an eventuality that must be halted by demonstrating strength and confidence in the vitality of Antwerp’s diamond sector!” “Antwerp’s loss could be Surat’s gain” is the way the Times of India reported the situation last week.

THE GLOBAL DIAMOND TRADING HUBS

Source: http://www.bain.com/

Click on chart to enlarge

There is still vulnerability to sanctions for Alrosa. But it is indirect, because the company is obliged during this year to pay off short-term debt totaling Rb56.3 billion as of December 31, 2013. At that point, free cash was Rb9.3 billion. The ratio of debt to cash was a high 6x; the company is forecasting this will shrink to 1.7x by the end of this year. Refinancing in the interval may be affected if there is a US attack on Russian state banks or Russian state companies.

Otkritie analyst Denis Gabrielik reported a fortnight ago that Alrosa management had told him refinancing negotiations to convert short to long-term debt are “expected to be completed this month [April]… At the beginning of May 90% of Alrosa’s debt should be long-term.” If that turns out to be the case, the exposure to US attack will be minimal. Gabrielik is assuming so, and is projecting a 50% increase in Alrosa’s target share price to Rb56.20. That would represent a market capitalization equivalent to $11.6 billion. Two years ago, in the run-up to a public share offering, Alrosa management was promoting a target valuation of $13 billion.

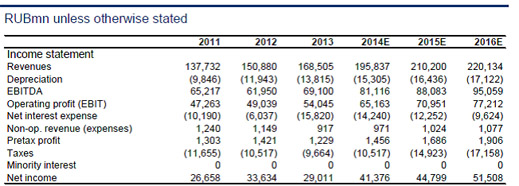

The good news from Alrosa, along with even sweeter projections, have been tabulated by Otkritie as follows:

Last October Alrosa made a secondary public offering (SPO) in Moscow, with share-buying and price support from the state’s Russian Direct Investment Fund to hold the low listing price of Rb35 per share. That created a market capitalization of Rb258 billion (at the time $8.12 billion). The price then drifted down, and in mid-January of this year it hit a low of Rb32.20. Since then it has reached highs above Rb38 three times; it is currently pretty much where it started at the SPO. According to chief executive Fyodor Andreyev, “ALROSA’s successful SPO on MICEX in 2013 proved a high level of confidence in the Company from long-term investors and showed capitalization growth prospects”. Well, not exactly.

ALROSA SHARE PRICE TRAJECTORY, 6-MONTH CHART

Source: http://www.bloomberg.com/

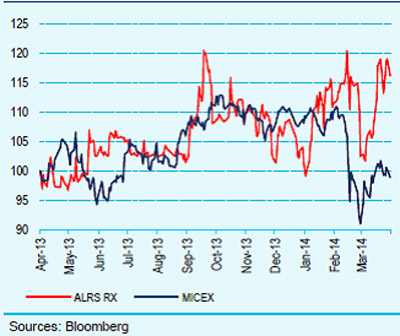

The short-term effect of the good news has been that since March, Alrosa’s share price has disconnected from the Moscow stock market trend. On the upswings of the index, the gap widens to the considerable advantage of the Alrosa share price.

ALROSA SHARE PRICE TRAJECTORY COMPARED TO THE MICEX INDEX

Why then would Yury Trutnev want to upset the apple-cart and propose to replace Andreyev as chief executive? And this, weeks after the government shareholders had already approved the renewal of Andreyev’s contract for another five years, starting in July?

Trutnev has had a pedestrian career as the political representative of commercial interests, starting in his home town of Perm; then the Perm region. For nine years he was the minister in charge of the Russian mining and resource sector under deputy prime minister Igor Sechin (left, right). Replaced as minister in September 2013, Trutnev was given the rank of deputy prime minister and the job of presidential emissary for the fareast, replacing Victor Ishaev, who lasted only a year. Ishaev’s much longer tenure as the self-serving governor of Khabarovsk krai was reported here.

Trutnev has had a pedestrian career as the political representative of commercial interests, starting in his home town of Perm; then the Perm region. For nine years he was the minister in charge of the Russian mining and resource sector under deputy prime minister Igor Sechin (left, right). Replaced as minister in September 2013, Trutnev was given the rank of deputy prime minister and the job of presidential emissary for the fareast, replacing Victor Ishaev, who lasted only a year. Ishaev’s much longer tenure as the self-serving governor of Khabarovsk krai was reported here.

According to the Moscow newspaper Kommersant last week, Trutnev turned his thumb down on Andreyev during what had been expected to be a routine cycle of ministerial sign-offs, before the appointment was finalized by first deputy prime minister in charge of Alrosa, Igor Shuvalov. The newspaper reported that Trutnev lacks veto power, and that out-ranking Trutnev by a degree, “nothing prevents Igor Shuvalov to sign the directive”.

Shuvalov has much the same record for self-interested governance as Trutnev and Ishaev; and despite his higher rank he has not proved to be notably more successful. In mid-2012 Shuvalov attempted to arrange the privatization of Alrosa shares for a state-financed takeover of the diamond miner by Suleiman Kerimov. At the time Kerimov also controlled the potash miner, Uralkali, and the goldminer, Polyus Gold.

Shuvalov (below) has as much trouble buttoning up deals as he has his shirt.

He failed to get government agreement for Kerimov to acquire Alrosa, just as he has failed at steering the privatization of the state shipping company Sovcomflot. That he has not yet agreed to sign Andreyev’s appointment may mean he is siding with Trutnev; that Trutnev may be acting on his instructions; and that they both represent a commercial interest that is still hidden.

Trutnev has also proposed adding an additional member to the Alrosa board, officially representing the Ministry of the Development of the Fareast, but in effect representing Trutnev. Between Trutnev and Shuvalov the weight of federal government influence on the 16-seat Alrosa board is being shifted from the Finance Ministry, which inherited the diamond sector from the Soviet arrangements and preserved it under Alexei Kudrin until he lost the ministry in 2011. According to Kommersant’s sources, Trutnev is pitching to take Kudrin’s place at Alrosa in league with Shuvalov. On the present Alrosa board, the Finance Ministry holds one seat and the vice-chairmanship, as well as influencing two other board members – Denis Morozov and Sergei Dubinin.

In March Trutnev also made a pitch for the support of the government of the Sakha republic (Yakutia) – the fareastern region where all but one of Alrosa’s mines are located. Sakha controls 33% of the Alrosa shares and six seats on the board. It has the direct right to stock and sell a share of rough diamonds produced at the Nyurba mine. The federal government controls 49.9% of the Alrosa shares; the free float adds up to 23.1%.

An Alrosa debt note prospectus issued in 2010 by UBS, JP Morgan and VTB, described the special powers of the Sakha government. These include a priority purchase right for the Sakha diamond stockpile; call on the company’s revenues for local needs; and regulatory powers which may conflict with federal regulations and company policy.

Last month Trutnev said at a conference on the future of the Russian diamond industry in Yakutia that he favours the resurrection of diamond cutting and polishing in the region. This is despite almost twenty years of efforts to operate such plants. The largest of them, Tuymaada, in which at one time Alrosa held a 12.7% stake, has been in and out of insolvency, and is no longer the recipient of a supply of rough diamonds from Alrosa.

According to Sergei Goryainov, a leading analyst at Rough & Polished, the Russian diamond industry bible, Tuymaada and a number of other regional operators were designed, not to cut and polish, but to act as conduits for discount-priced rough diamonds to move into the hands of exporters and offshore buyers. Trutnev’s new idea, says Goryainov, is “flawed because it’s been tried many times before, and it has always ended up in the same way. The local cutters were getting preferences from Alrosa. They acted as intermediaries in the market of raw materials, and as a result, instead of cutting the diamonds they were engaged in dumping, and eventually finished up in bankruptcy. Ultimately, dozens of cutting factories went bankrupt in Yakutia leaving the budgets of the Russian Federation, Sakha and Alrosa with multi-million dollar costs.”

A detailed report on these problems in the Sakha diamond manufacturing industry can be read here. The study dates from 2005. The lessons haven’t diminished with time.

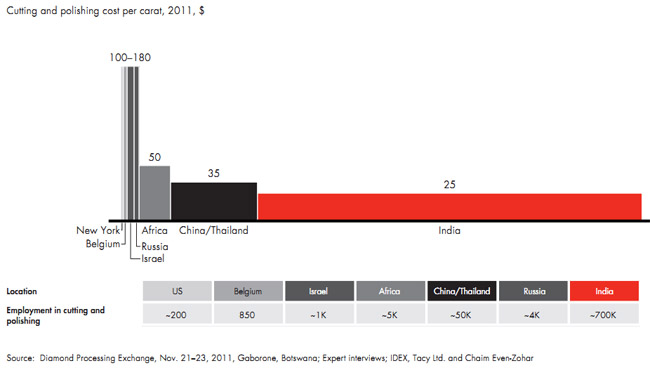

Goryainov has also calculated that the economics of Trutnev’s scheme, even with state budget and Alrosa preferences, remain unprofitable. The cost of cutting and polishing diamonds in Yakutia cannot be less than $180 per carat, Goryainov suggests. In Moscow it is $150 per carat, and in Smolensk, where Russia’s dominant diamond manufacturing plant operates, the cost is down to about $80 per carat.

The Bain report illustrates how these costs compare with cutting plants across the diamond world:

Click on chart to enlarge

Once the commercial impossibility of the scheme is understood, Goryainov concludes that the Trutnev proposal is in fact a scheme to revive diamond supply preferences for others to benefit, using Sakha diamond manufactories as fronts. Because the profit margins of diamond cutters and polishers are much smaller than diamond miners or retailers of diamond jewellery, the manufacturers have to be ingenious at preserving their margins, especially in times when the price of rough has been contracting. This necessity is the mother of many inventions, almost all of them against Russia’s law on competition, not to mention the criminal code on tax and customs offences, and fraud.

There is nothing unique about the situation in Sakha. Preferential terms of supply, including preferential assortment (aka cherry picking from the run of mine), is a chronic problem for diamond miners everywhere. Russian diamantaires acknowledge it has taken Alrosa longer than most of the global diamond miners to restrict or eliminate these preferences. For that, chief executive Andreyev is acknowledged to have been signally more successful than his predecessors.

Goryainov said he suspects Trutnev’s attack on Andreyev’s reappointment is an attempt to replace with him with someone more amenable to preferences, or to pressure him into granting preferences in exchange for Shuvalov’s signature. A well-known international diamantaire says: “I was in Moscow recently, and you certainly hear that Alrosa’s selling policies are more rigorous, with an element of objectivity being introduced (at last). I did not hear anything about [Lev] Leviev being involved in [the Trutnev scheme]. I would have thought Andreyev’s position was fairly secure.”

Goryainov says: “there are a number of sources. They argue that Mr. Trutnev was, and perhaps now is the lobbyist for the interests of Lev Leviev. He was in close contact with Trutnev in the period when Trutnev was the governor of the Perm region. At this time Leviev bought there a [mining] company called Uralalmaz and organized a cutting company, Kama-Kristall. Then when Trutnev left Perm region, Oleg Chirkunov, his successor, a former business partner of Trutnev, has headed Perm region and also worked closely with Leviev. If this is true — let me emphasize the hypothetical, if this is true – then the interest of Trutnev in Alrosa and the negative attitudes expressed towards Andreyev can be attributed to some extent, perhaps, to these contacts. So far as I know, Leviev’s Moscow company Ruis Diamonds lost the preferences it enjoyed in the mid-2000s through Alrosa subsidiaries, Almazy Anabara and Nizhne-Lenskoye. All this was under the previous leadership of Alrosa. But this practice was discontinued. In comparison with those times, the Leviev enterprises are in a much worse position now than they were then.”

Valeriy Morozov, the chief executive of Ruis Diamonds and Leviev’s representative in Moscow, said: “Trutnev is certainly familiar with Leviev, but not so close. And even more, we cannot speak about any lobbying. As for Andreyev, on the contrary, our group has with him very constructive relationships in all areas. He is a very competent manager, the best of all the presidents of Alrosa in recent times. Indeed, today he is the most suitable candidate, and there is no alternative candidate for this position. Our view on this issue is well-known, including [our view] on Trutnev. But it is obvious he has his own view on Alrosa.”

“Trutnev’s viewpoint on the leadership of Alrosa”, adds Goryainov, “is not objective. It expresses lobbying interests, and perhaps personal antagonism. Maybe both.”

Trutnev was asked to explain the reasons for his opposition to Andreyev’s reappointment. Shuvalov was asked to say whether he supports Trutnev or Andreyev. Neither official has responded.

Leave a Reply