By John Helmer

An out of court settlement has been reached between Oleg Deripaska and his Russian Aluminium (Rusal) group, and Avaz Nazarov and a group of firms associated with the Tajikistan Aluminium Plant (TadAZ).

The confidential deal was announced on Friday in London by law firm Clyde & Co, which has represented Nazarov and his group. The lawyers’ statement said: “Rusal and Ansol have reached a comprehensive settlement of all of their outstanding claims against one another without any admission of liability by either side. Both parties are content with the terms of the settlement and pleased that their disputes have now been resolved.”

Nazarov and his associates at Ansol are unavailable, and their law firm says there will be no comment. There has been no statement from Rusal. Rusal spokesman, Vera Kurochkina, refuses to answer questions.

The settlement announcement came one day after wire services reported Oleg Deripaska as saying in Vienna on Thursday that the planned initial public offering (IPO) of Rusal would come “in the nearest future.” “We have a partnership agreement and it states that we will turn Rusal to an IPO as quickly as possible,” Deripaska is quoted as saying. “It will happen in the nearest future as far as I am concerned.”

Deripaska owned almost all the shares of Rusal, which last month merged with Russian rival SUAL, and also includes alumina refinery assets from Glencore. Deripaska now holds 66% in the new Rusal; Victor Vekselberg, SUAL’s owner, 23%; and Glencore 12%. The company is now the world’s largest producer of primary aluminium, and one of the largest global miners of bauxite and refiners of alumina. It claims to hold 12.5% of the global aluminium market, and 16% of the global alumina market.

The Nazarov group — which controlled TadAZ, Tajikistan’s most valuable enterprise, until December 2004 — has been highly effective in two parallel High Court claims in London. One charges Rusal with data theft, unlawful computer hacking and spying in the Nazarov group’s computers. The judge in that case has ordered Rusal to open up its Russian computer system to an independent inspector.

The civil case, first initiated in Chancery two years ago, was officially captioned against TadAZ; Deripaska; Rusal; Rusal’s chief executive Alexander Bulygin; two shell companies registered in the British Virgin Islands; Orienbank of Tajikistan; and an influential Tajik official. The claim alleged breach of contract, unlawful interference in trade, breach of trust, and corrupt conspiracy. As Mineweb has already reported in detail, this was a counterclaim to allegations from TadAZ against Nazarov, plus several of his associates and companies.

The initial claim by TadAZ was the boomerang that has returned to strike Deripaska, expensively.

In the court proceedings, Nazarov’s lawyers contended that every reference to Rusal meant those who control the company — Deripaska, Bulygin, and Gulzhan Moldazhanova, the former finance director of Rusal, and now a director of Deripaska’s Moscow holding, Basic Element. The High Court has accepted jurisdiction over Rusal, and lawyers have been preparing for trial later this year.

In a statement to Mineweb, after the tide in court first turned against Rusal, the company said: “RUSAL was drawn into this case by TadAZ’s opponents purely in an attempt to create a smokescreen to draw attention away from allegations of fraud against Ansol [Nazarov company].”

It can be expected that all proceedings will now be wound up.

No details are available of the settlement. But if Deripaska’s settlements in previous contract and other legal claims are a guide, it is likely he has paid the Nazarov group more than $100 million.

On November 2005, a London arbitration proceeding awarded Norsk Hydro $145 million, payable by TadAZ for breach of contract in delivering aluminium. The text of the initial and appellate rulings in that case have been kept secret by applications from Rusal’s lawyers. Hydro confirms the payoff deal.

The claim form originally filed by Nazarov’s group in July 2005 declared only that their claim exceeded GBP15,000. Legal costs for Nazarov over more than two years are estimated to be between $5 million and $10 million. Testimony in court to date indicates that compensation has been calculated on the basis of profits Rusal made after ousting Nazarov from the plant, and profits Nazarov and his companies would have made, if Rusal had not ousted them. A claim of about $220 million, plus costs, interest, and exemplary damages, is estimated to have been the basis for the settlement negotiation. The unprecedented success Nazarov’s lawyers have had in the UK High Court — the first international court to oblige Rusal to face trial for its business practices — limited the discount Deripaska would have been able to achieve.

In its press releases to date, Rusal claims to be innocent of all the charges alleged against it of contract breach, asset theft, racketeering, and corruption. Rusal also claims to have succeeded in having the charges thrown out of the US courts on jurisdictional grounds. Innocence has its price, and Deripaska has paid substantial out of court settlements.

The terms are all sealed, and the beneficiaries don’t talk. Lawyers, public records, and sources close to Deripaska and inside Rusal confirm, however, that the Zhivilo brothers were paid about $65 million; they had controlled the Novokuznetsk smelter before Deripaska, but then failed to win jurisdiction in a US court for their claim. Anatoly Bykov, controlling shareholder of the Krasnoyarsk smelter before his ouster, was paid about $105 million, a sum ordered by an arbitration tribunal and appeals court in Zurich, which Swiss court records corroborate.

The Reuben brothers of London, who ran several trading schemes for the Russian smelters Deripaska operated, claimed $300 million; they received a sum reported to be over $100 million, after an application to a British Virgin Islands court. Details of their June 27, 2005, settlement spilled out when one of Deripaska’s companies – called Bluzwed Metals — went into the High Court in London, arguing that Trans World Metals, the Reubens’ vehicle, had violated Clause 11.4 of the secret deal with Deripaska. Deripaska then sought High Court enforcement of the Reubens deal. He got his summary judgement on January 26, 2006, in a ruling by Justice Sir Andrew Morritt. One secret also spilled in the Bluzwed case was the identity of a Lebanese arranger called Joseph Karam – “K” in the court text – whose payoff and indemnity from further claims Bluzwed accused the Reubens of threatening..

Counting the latest Nazarov settlement, Deripaska has been obliged to fork out about half a billion dollars to those claimants with cases strong enough to take to foreign courts and tribunals.

If he manages to list Rusal in a London IPO at a market capitalization of $30 billion, Deripaska’s 66% stake would be worth $19.8 billion. Cashing out claims that constitute a serious legal barrier to the IPO saves money, and makes business sense.

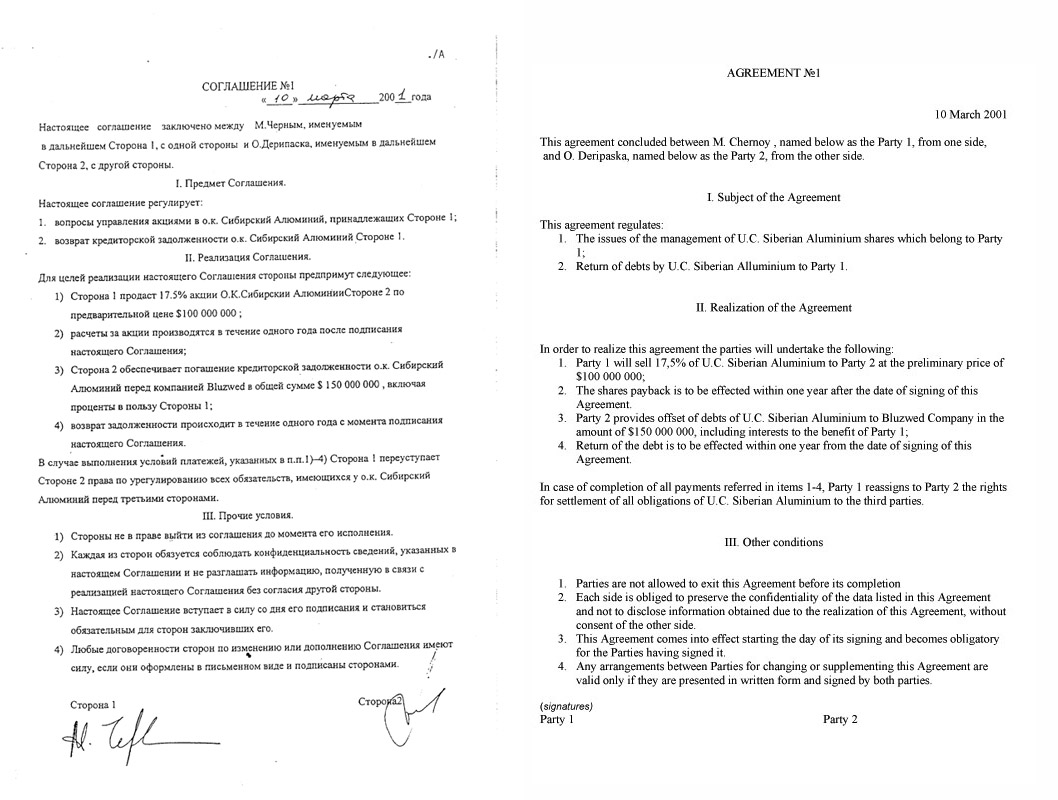

Just one UK High Court case remains — that of Mikhail Chernoy (Michael Cherney). This was filed in the Commercial Court of Queens Bench on November 24, 2006. The sole defendant is Oleg Deripaska, who is accused of breach of trust. Mineweb has reported the details before. There has been no court hearing yet.

The evidence in Chernoy’s case, according to the claim form, and interviews he has given the Russian press, is an agreement Deripaska and he signed, under UK legal jurisdiction, on or about March 10, 2001. This claims Chernoy’s entitlement to 20% of Deripaska’s equity in the original Rusal, and a like proportion of the dividends earned on the capital since 2001.

Here is how the liability arithmetic adds up. Deripaska’s 66% stake in the new Rusal, at IPO target valuation, would be $19.8 billion. A 20% share of that would come to $3.96 billion. Rusal’s net profit from 2001 to the end of Q1 2007, when the merger took effect, is estimated at about $10 billion, but because Rusal is a closed private concern, it isn’t known how much of that was paid out in dividends. Supposing all of it, that would include Chernoy’s entitlement to $2 billion. If and when Chernoy and Deripaska sit down together, the opening demand on the table is likely to be $6 billion.

To play a card as pricey as that, Chernoy must get before a UK judge, and like Nazarov, start presenting the evidence in his case, and win initial rulings. Unless or until he does, the investment banks and law firms responsible for the Rusal IPO will be able to press on, blackening Chernoy’s credibiility as plaintiff, and dismissing his claim as extortion. Unseen by the judge, the Chernoy-Deripaska agreement would become a dead letter.

If Deripaska wants to make sure of that, he could try negotiating a hefty discount with his old godfather, payable in part from the proceeds he expects to draw from the IPO. Chernoy, who has been waiting for his cash for six years, is going to insist on money up front. Will he accept a discount, and a wait?

Deripaska’s stake may be worth $19.8 billion after the IPO, but that’s paper money. Assuming that a 15% shareholding in Rusal is sold at the target price for the IPO, then that would raise $4.5 billion in cash. But only $2.97 billion of this — less placement fees and costs — would be available to Deripaska. There are also bound to be other calls on this cash from Moscow, before he can meet Chernoy’s demand.

Pleading that he isn’t cash-rich at all, will Deripaska offer Chernoy $2 billion to tear up the March 10, 2001, agreement, and go away? Will Chernoy accept it? Chernoy isn’t saying.

Deripaska must play for time, but the clock is ticking against him, so long as the Chernoy agreement of 2001 is an albatross hanging unluckily around his neck. But if the two could agree on staging payments over time, with the bulk to come from Deripaska’s dividends from future Rusal earnings, this may constitute a prima facie violation of Deripaska’s undertakings to the European Bank for Reconstruction and Development (EBRD), when he swore he had fully bought out Chernoy years ago. An ERBD loan to Rusal, and a matching credit from the World Bank’s International Finance Corporation, depend legally on the truthfulness of Deripaska’s covenants.

And there is another potential liability for the owner of the world’s most important bauxite, alumina and aluminium combine. Would an ongoing financial obligation between Deripaska and Chernoy complicate Deripaska’s relations with the US authorities?

If it can be authenticated, the Chernoy document is serious evidence in the Federal Bureau of Investigation’s dossier on Deripaska. Now that the Nazarov case is gone, the pressure is on Deripaska to settle with Chernoy on terms that also resolve his problems with the FBI.

According to evidence already reported by Mineweb, and publications by a US newspaper this month, the US State Department has revoked Deripaska’s visa to enter the US, first issued in 2005. According to the newspaper, this happened last year “after concerns were raised about the accuracy of statements he made in a meeting with the Federal Bureau of Investigation, according to U.S. officials and others familiar with the matter.”

On April 17, Deripaska’s spokesman at the London PR agent Finsbury, Simon Moyse, was reported as saying that Deripaska is in current possession of a multiple-entry US visa. Further checks by US reporters led to reconfirmation that Deripaska’s visa had been revoked. The gap between the Finsbury claim and the US reports is easily explained by the circumstances in which Deripaska learned that his permission to enter the US had been withdrawn.

Deripaska had been about to board his jet in Toronto last year, when the US immigration system flashed a warning, and the US agent told Deripaska his entry visa had been revoked. Thus, Deripaska knew he held a visa in his passport — the Finsbury announcement — but he also knew that there was no permission to enter the country.

Lawyers, other sources close to the US government review of the Deripaska visa, UK and Australian officials have all confirmed that Deripaska’s problem stems from concerns relating to his business practices. Deripaska has strenuously denied any involvement in organized crime, and calls the reported charges against him extortion.

Because a US visa ban is also enforced by the UK and Australian governments, Deripaska has applied for waivers in order to enter the UK and Australia. On one occasion, confirmed by UK sources, British government investigators detained Deripaska after his private aircraft landed near London, and combed the aircraft, and computers and files carried by its passengers, before he and they were released. The Australian Ambassador in Moscow has confirmed that Deripaska has received waivers to enter Australia, where Rusal bought a minority stake in a Queensland alumina refinery.

In the latest US newspaper reports, it is disclosed that Deripaska paid $560,000 to the law firm of former Republican Senator Bob Dole to resolve the FBI’s ban, and get Deripaska his 2005 visa. Washington sources report that other prominent US law firms, and at least one other prominent Republican Party official, have been retained by Deripaska over the years to surmount the visa ban, and retrieve the black ball. At one point, the source claims, he was offering a sizeable bounty for success. The sources also say there has been a long-running and spirited argument between the White House, the State Department, and the investigation agencies over this issue.

The prominent publication in the US and corroboration of these troubles complicates participation in the Rusal IPO for US banks and US lawyers.

Leave a Reply